There was plenty of tropical wood furniture to be found at the first two big European furniture exhibitions of 2018 – the IMM interiors fair in Cologne, Germany (IMM-Cologne), and the January Furniture Show at the NEC in Birmingham, UK (JFS-Birmingham).

Judging by the stand listings, tropical timber products were also set to have a strong presence at the biggest international show of them all, the Milan Furniture Fair from April 17-22.

Among the 2,000 exhibitors at the latter (including 650 from outside Italy), companies were listed from Brazil, India, Indonesia, Vietnam and, leading the way with a total of 12 stands, Thailand. In addition, said organising federation Federlegno Arredo, judging by previous Milan shows there were set to be more tropical products on European importers’, distributors’, designers’ and manufacturers’ stands.

At the German and UK shows, plantation teak and mahogany furniture made a particularly strong showing, while other prominent tropical species included acacia, mango, munggur and suar.

At both events, there seemed to be a fashion too for recycled tropical timber products, with tables and storage units made from a range of species recovered from old doors, flooring, decking and even boats. Indian companies seemed to be particularly favoured, with their style currently in fashion, said exhibitors.

“Originally these recycled pieces looked recycled, with a deliberately rustic finish,” said one UK designer-importer. “But now, manufacturers, under our guidance, are working the wood more and going for more sophisticated, polished styles.”

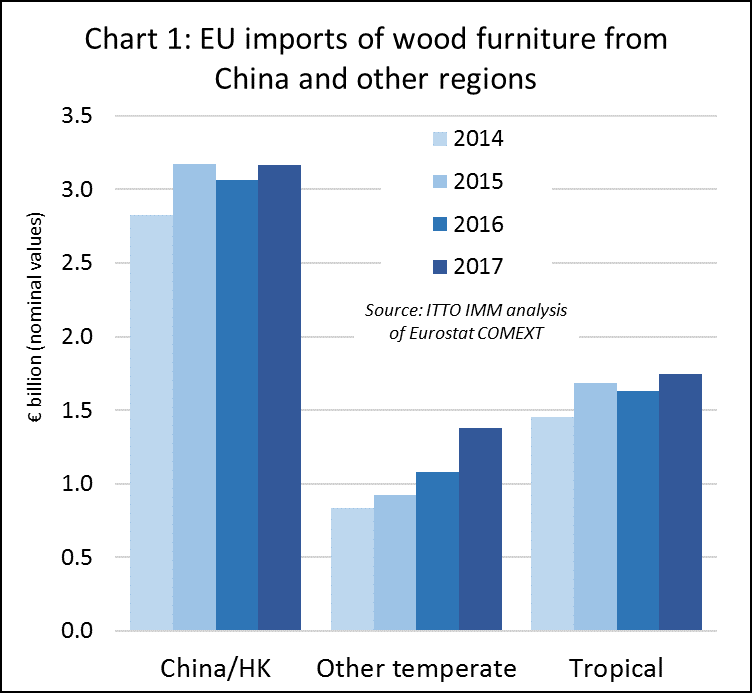

In fact, furniture from tropical countries has been performing reasonably well in the European market for the last four years. There was a slight dip in EU imports in 2016, which some attributed to the impact on wider consumer confidence caused by the UK’s vote to leave the EU, although others said it was small enough (under 3%), to have been ‘normal trade fluctuation’. But business picked up again last year as EU imports rebounded 7% to €1.75 billion. (Chart 1).

Increasing furniture market competition

However, looking more closely at the figures and wider sales trends, the news for tropical wood furniture in the EU is not quite as good as it might at first seem. Given the increasingly vigorous post-recession growth of the EU furniture market, said exhibitors and trade association representatives at the UK and German shows, you might have expected tropical products to have done better and have more of a profile at trade fairs.

The fact is – and the statistics support the anecdotal feedback from the trade – tropical suppliers have not been keeping pace with the competition in the EU, either from other EU import sources, or more significantly the EU’s own robust and dynamic furniture manufacturing base. So, while they may have grown overall sales in recent years, they have lost market share to rival producers.

According to latest figures, EU imports from temperate timber furniture suppliers in the last four years rose 66%, from €830 million in 2014 to €1.38 billion last year.

Amongst the largest increases in wood furniture imports from temperate countries last year came from the Ukraine, up a further 67.7% to €133 million, Bosnia, up 14.9% to €218 million, and Serbia, up 13.7% to €127 million.

A further major hike in 2016, from €62 million to €150 million, is also shown in EU imports from the US, all destined for the UK. However, this figure needs closer examination as it could be the result of large distributors changing sourcing policy, or a change in reporting of products against furniture customs code. Other big rises came from ‘other temperate’ producers, up 35.5% last year, notably from Turkey and Switzerland.

EU furniture sector recovery and growth

The biggest shift in the EU furniture sector in recent years has come in the degree of market self-sufficiency, with European manufacturers taking more of their domestic national and intra-EU trade. Further underlining their growth and increasing competitiveness, they are also exporting more.

According to the European Furniture Industries Confederation, the sector was hard hit in the international downturn from 2007, seeing turnover fall from €136 billion to €90 billion and shedding 280,000 jobs. Since then, however, it has seen sales recover to €96 billion and its workforce to rise to over 1 million again.

In 2010, EU furniture suppliers achieved intra-EU trade turnover of €15.3 billion from, while exports were valued at €6.4 billion and imports at €5.9 billion, delivering a €500,0000 trade surplus. By the end of 2017 the intra-EU trade figure had jumped 26% to €19.2 billion, while exports hit €8.8 billion. With total imports having grown only to €6.3 billion, this pushed the trade surplus to €2.5 billion in 2017, five times the level of 2010.

Several reasons are given for the success and development of the EU furniture industry. One is the maturing of investment from Western Europe into manufacturing in former Soviet bloc Eastern European countries, led by big brands such as IKEA. From being principally production satellites for companies like the latter, the plants are reported increasingly to have developed their own identity and market momentum.

An illustration of this is the latest market development project from the American Hardwood Export Council (AHEC). As part of its strategy to grow European sales of US red oak, it has linked with leading Polish furniture designer Tomek Rygalik. He has worked with leading international labels, including IKEA, and is now design director for major Polish producers Paged and Comforty.

In the AHEC project, Tomek Rygalik is creating a US red oak furniture collection, which the Americans hope will not only sell well and help promote the species in Poland itself, but also in the latter’s Western European furniture export markets. The goal is also to fire the interest of other Polish designers.

Technological impacts in EU furniture sector

Increasingly advanced computer-controlled and automated manufacturing has also benefited European producers, boosting their productivity, cutting overheads and reducing the relative labour cost advantages of competitors, such as those in the Far East.

“The increasing migration of European furniture sales online additionally favours a local manufacturing base,” said a German designer/producer. “It is better placed to meet the short lead times demanded by today’s EU internet retailers and consumers.”

Whether it also benefits domestic EU producers that the most in-fashion timber furniture species in the EU market remains oak is more debatable. There’s no doubting oak’s overwhelming dominance of the sector – in the latest development underlining this, it is reported that one of the Europe’s biggest retailer/producer brands is currently looking to sign up a supplier of up to 140,000 m3 this year.

But while European manufacturers may be close to sources of European oak supply, there are few limitations on its export outside the EU. This is despite efforts by manufacturers in France, in particular, to lobby their government to curb log exports, notably to China.

It’s also notable that EU furniture producers import large quantities of US white oak and that Asian producers have ready access to this material. In fact, a number of companies at the IMM-Cologne and JFS-Birmingham exhibitions were showcasing EU-designed ranges manufactured in US white oak by joint venture or subcontractor partners in South East Asia, notably Vietnam.

“Source locally” is a key theme of EU manufacturers

There does however, also seem to be a growing preference in the EU market to ‘source local’, particularly in the design and specifier sectors. This is mainly to support homegrown forest and timber-using industries – although EU furniture manufacturers and retailers like to take credit for the reduced transport miles and carbon footprint implied. This is despite several recent LCA studies of wood furniture undertaken by AHEC showing that environmental impacts incurred during the transport phase are significantly less than those incurred during the processing and manufacturing phases.

In practice the carbon footprint of wood furniture is often more dependent on the quantity and mix of energy used to convert and dry the wood, and the energy efficiency of the manufacturing operation, than on shipping even when materials need to be transported over large distances.

Nevertheless, the “source local” theme will feature at the Carrefour International du Bois show scheduled for 30th May to 1st June this year in Nantes, France. The four-year-old ‘Le Bois Français’ campaign will once more have a prominent presence and there will be significant regional French timber industry representation. In the UK, the Grown in Britain initiative, which is supported by such leading furniture retail brands as Heal’s and Marks & Spencer, is now in its fifth year and said to be still increasing its impetus.

Underlining just how competitive the EU furniture market is, even China has recently struggled to increase sales. EU imports of wood furniture from China rose 12% to €3.17 billion in 2015, but since then have plateaued around that level.

Leading tropical suppliers of wood furniture to the EU

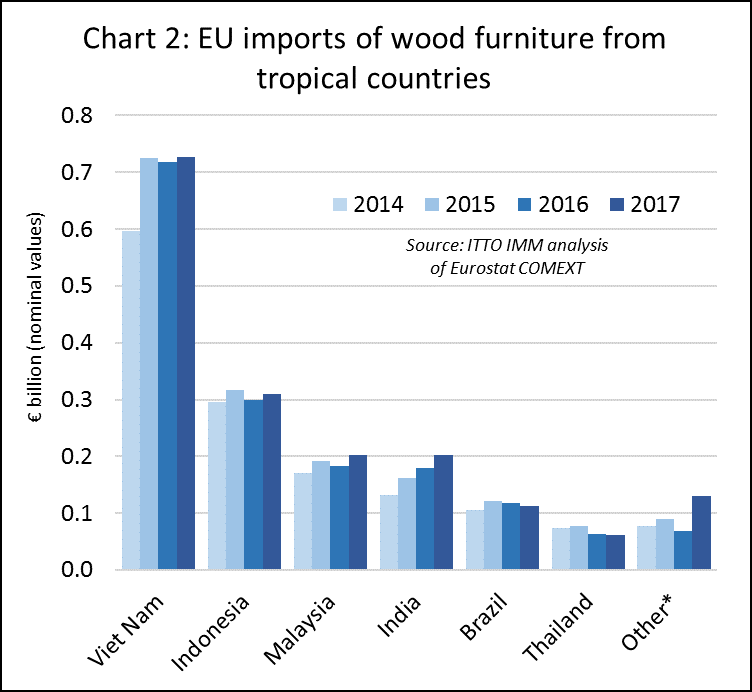

In terms of the leading tropical furniture suppliers to the EU, imports from Vietnam and Indonesia have followed a similar trend; rising relatively strongly in 2014 but slowing since. EU imports from Vietnam increased just 1.3% to €730 million last year, while imports from Indonesia increased 3.7% to €310 million. (Chart 2).

There was better news for Malaysia. After dipping 5% in 2016 to €184 million, EU imports from Malaysia recovered 10.3% to reach €203 million last year. EU imports from India have experienced more consistent year on year growth since 2015, with trade rising an additional 12.3% to €202 million in 2017.

After relatively static performance for four years, EU imports from Brazil and Thailand both saw decreases in 2017, down 5.3% and 3.4% to €112 million and €61 million respectively.

The biggest increase last year, albeit from a modest base of €69 million, came in EU imports from ‘other tropical countries’, up 87.8% to €130 million. Contributions to this rise came from Singapore, which is channelling furniture to the EU from elsewhere in South East Asia, and from the UAE and Qatar. EU imports of wood furniture from the two Middle Eastern countries jumped from under €1 million in 2016 to a combined total of nearly €36 million last year. This increase all went to the UK and is either an error in the customs statistics or could indicate a switch in sourcing by major retailers or distributors.

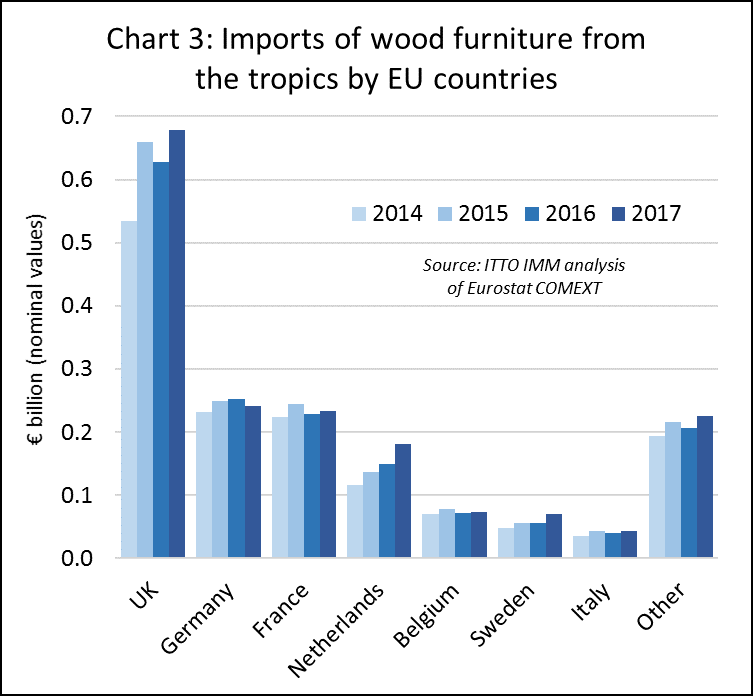

In terms of EU importers of furniture from tropical countries, the leading buyers have stayed in the same order by sales value since 2014. The UK remains the largest buyer, with imports up 8% last year at €680 million, having dipped 4.5% in 2016. Germany is in second place, despite a 4.2% downturn in imports last year to €240 million. Next is France, with imports up 2.4% at €230 million, the Netherlands, up 20.5% at €180 million (another anomalous requiring further scrutiny), Belgium up 2.4% at €70 million, Sweden up 23.7% at €70 million, and Italy, up 10.4% at €40 million. Other EU importers increased their combined total 9.1% to €230 million in 2017. (Chart 3).

Tropical timber market promotion in the EU

In the face of falling market share, proactive steps are being taken to consolidate and grow tropical timber product sales in the European market.

The European Sustainable Tropical Timber Coalition (STTC), comprising timber importers, traders, end-users and retailers, plus public and private sector specifiers and procurement personnel, continues its market education and promotion efforts. A key aim is to ensure that sustainably sourced tropical timber products receive due and fair consideration in business and public sector procurement policy. The core message is that ensuring a healthy, viable market for the timber will drive the spread of sustainable forest management in tropical countries.

The STTC has recently been reviewing its activities, working with various partners in the industry. Aims include becoming more effective and efficient in delivering key market data and also focusing more on monitoring trade flows of sustainably sourced tropical timber into Europe.

ATIBT, the International Tropical Timber Technical Association, also continues to roll out its Fair & Precious marketing/branding initiative. This too aims to educate the market on the wider social, environmental and economic benefits of increasing demand for sustainably sourced tropical timber and wood products.

All businesses along the supply chain can use the Fair & Precious brand on their products, provided they pledge to source third party-accredited legal and sustainable goods and material and ‘commit to respecting social, environmental and economic concerns in their activities, subject to audit by third-parties approved by the Fair & Precious ethics committee’.

Whether the EU FLEGT VPA initiative and FLEGT licensing has the potential to underpin the tropical timber market is still a matter of debate. Indonesia, the first country to issue FLEGT licences, did see its timber furniture sales to the EU rise marginally last year to €310 million. However, they have been around that figure for the last four years, so, say importers, offer no real clue on the market impact or perceptions of licensing.

A key conclusion of discussions at IMM-Cologne and JFS-Birmingham, and of the EU FLEGT Independent Market Monitor (IMM) trade consultation held in London during March, is that there is still a need for more market education and communication about the wider FLEGT initiative. Several exhibitors at the UK and German shows and participants at the trade consultation acknowledged they knew little about it. They seemed particularly surprised by the scope of licensing systems and the extent of the forest reforms implemented as part of the FLEGT process.

At the IMM London trade consultation, Kate Towler, Assistant Manager Sustainability and Responsible Sourcing at retail giant John Lewis, said that companies like hers needed to know more ‘human stories’ behind FLEGT which they could relay to their personnel and consumers. But she did conclude that the consultation had provided ‘knowledge of the further capabilities of the [EU FLEGT VPA initiative and FLEGT licensing] beyond just legality assurance’. “This is something I will be looking into further with the possibility of positioning FLEGT within our internal timber sourcing policy,” she said.

At the same IMM event Andy Duffin, Operations Director of one of the UK’s leading timber importers and distributors James Latham, cautioned that the emphasis in promoting FLEGT should not be on selling a licensed product, but on selling the product first, licence second.

“I believe that the real issue behind tropical timber’s loss of EU volume market share is lack of promotion of products before schemes,” he said. “No one buys or sells FLEGT. We need to sell balau products, for instance, that are also FLEGT-licensed. Environmental issues are key, but they are side-lined if no-one wants the product.”

PDF of this article:

Copyright ITTO 2020 – All rights reserved