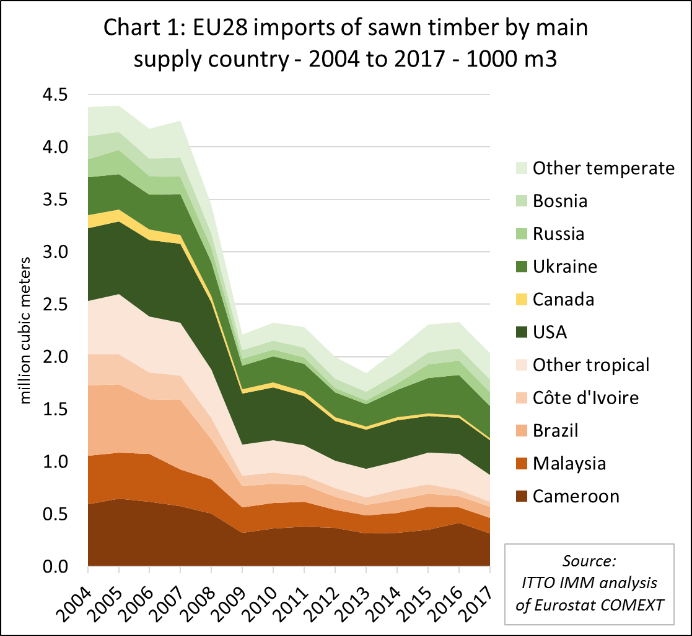

The EU imported 2.04 million m3 of sawn hardwood from outside the region in 2017, 13% less than the previous year. (Chart 1).

EU imports of tropical sawn hardwood were 875,000 m3 in 2017, 18% less than the previous year. Imports of tropical sawn hardwood last year were the lowest ever recorded by the EU, below the previous low of 930,000 m3 in 2013 during the euro-zone crises, and only around a third of the level prevailing before the global financial crises.

The value of EU imports of tropical sawn timber decreased by 16% to €653 million in 2017. The average unit value of tropical sawn hardwood imports into the EU in 2017 was €746 per cubic meter, up from €728 per cubic meter the previous year.

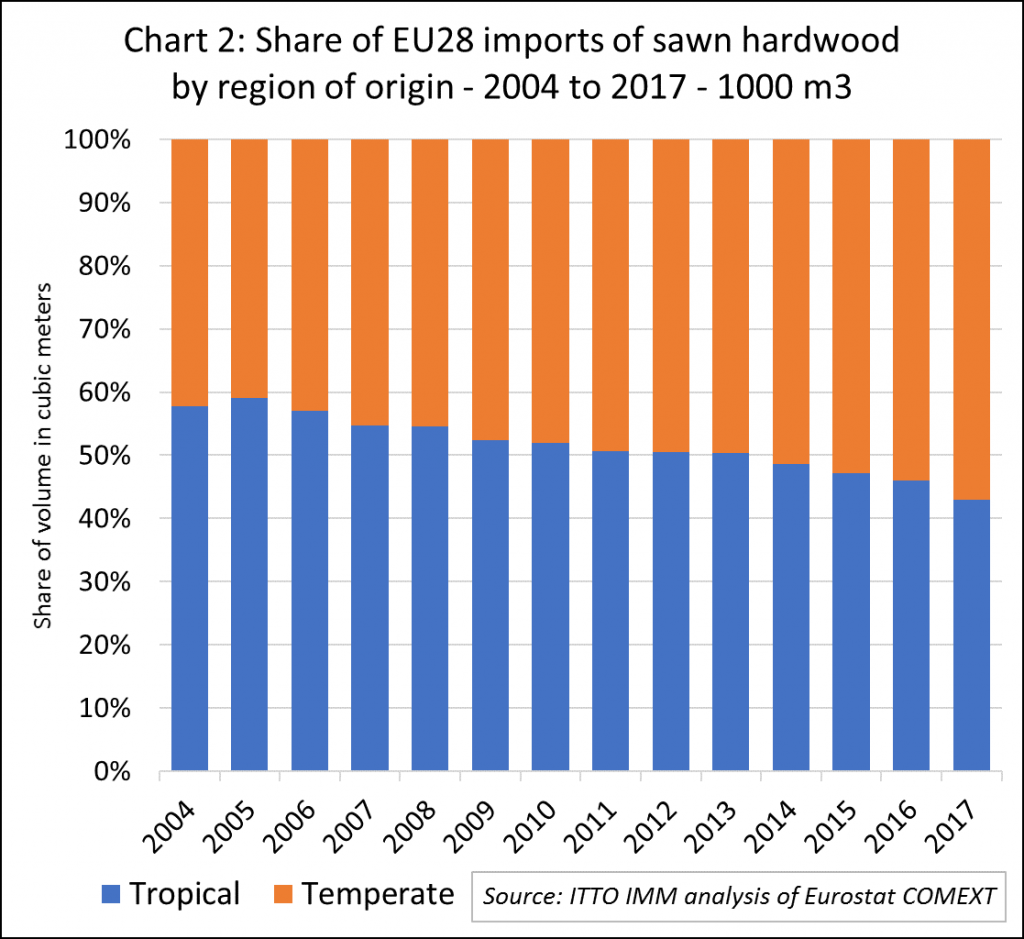

In 2017, EU imports of temperate sawn hardwood fell by 8% to 1.16 million m3. The more rapid pace of decline in imports from the tropics meant that the share of tropical in total EU sawn hardwood imports fell from 46% in 2016 to 43% in 2017, an acceleration in the long term downward trend (Chart 2).

Sharp fall in EU imports of African sawn wood

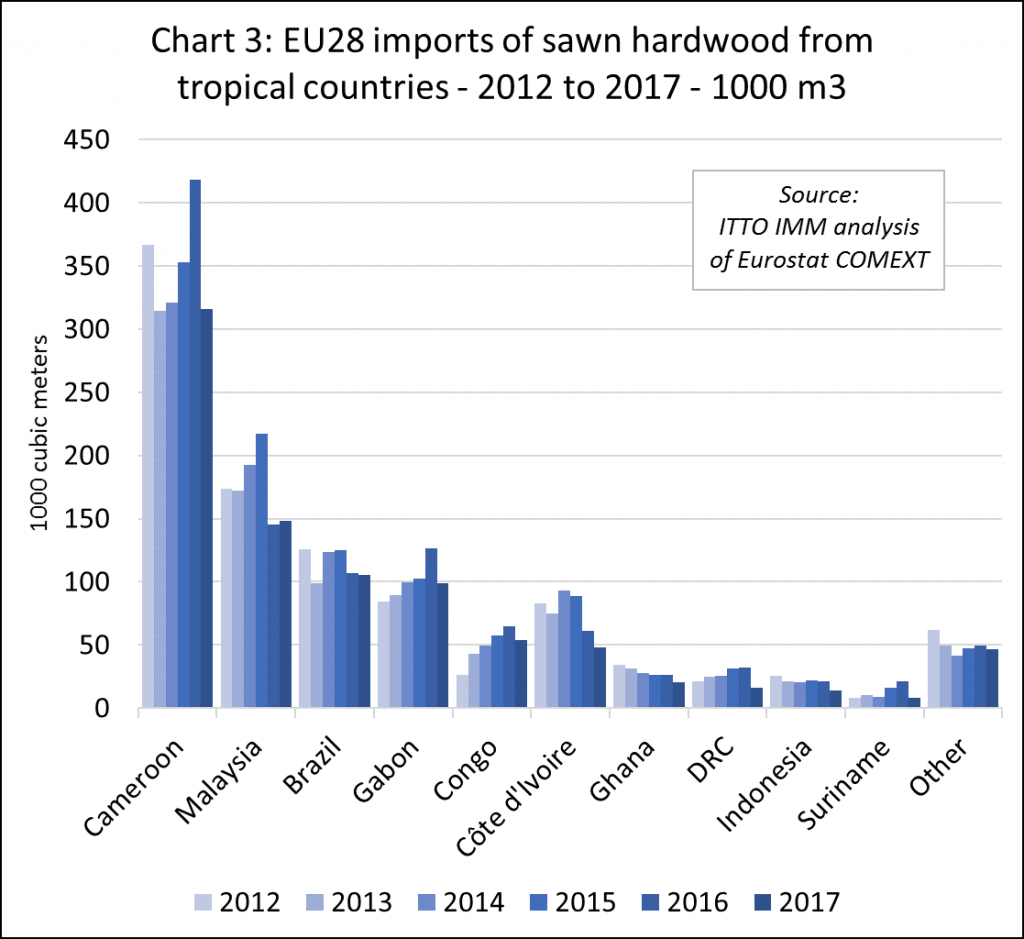

The most notable trend in the supply of sawn hardwood to the EU in 2017 was the sharp fall in imports from Africa, particularly from Cameroon, but also Gabon, Congo, Cote d’Ivoire, Ghana and DRC. Imports from Malaysia and Brazil were more stable (Chart 3).

Following a surge in 2016, EU imports from countries in the Congo region declined sharply in 2017. Imports decreased by 24% from Cameroon to 316,000 m3, by 22% from Gabon to 99,000 m3, by 17% from Congo to 54,000 m3, and by 51% from DRC to 16,000 m3.

Last year, there was also a continuation of the long-term decline in EU imports of sawn hardwood from West Africa. Imports fell by 21% to 48,000 m3 from Côte d’Ivoire, and by 23% to 20,000 m3 from Ghana.

EU imports from Brazil and Malaysia were more stable in 2017, although only a shadow of earlier levels having already declined significantly in previous years. Last year the EU imported 148,000 m3 of sawn hardwood imports from Malaysia, 2% more than the previous year, and 105,000 m3 from Brazil, 1% less than in 2016.

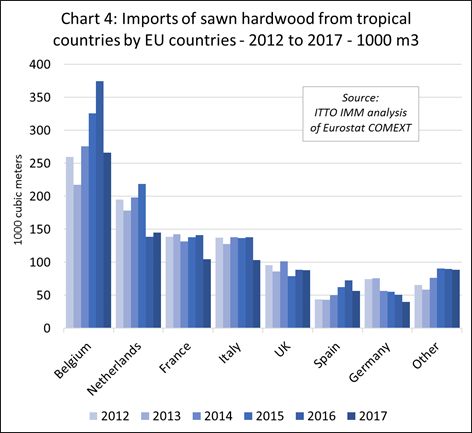

The decline in imports of tropical sawn hardwood during 2017 was particularly notable in Belgium (down 29% to 266,000 m3), France (down 26% to 105,000 m3), Italy (down 25% to 103,000 m3), Spain (down 22% to 56,000 m3) and Germany (down 21% to 40,000 m3). Imports increased 5% to 145,000 m3 in the Netherlands, after a sharp decline the previous year. Imports in the UK declined only 1% to 88,000 m3. (Chart 4).

Increasing concentration of trade in the hands of a small number of large companies close to EU ports, and their role to distribute tropical sawn timber throughout the EU, mean it is becoming more difficult to relate import trends with changes in consumption at national level in the EU.

Fall in EU imports driven mainly by supply-side issues

In practice, the recent decline in tropical imports into the EU is better seen as a region-wide phenomenon driven mainly by supply side trends. In 2017, a range of factors conspired to result in extremely low tropical sawn hardwood imports across the EU. These include:

- On-going serious problems and delays with shipping out of Douala port in Cameroon.

- Overstocking in the EU at the end of 2016 following arrival all at once of a large volume of delayed shipments from Africa.

- Diminishing commercial availability of tropical hardwood species of interest to European buyers.

- The problem of delayed payment of VAT refunds by African governments, partly linked to low oil prices, which is creating additional financial challenges for operators in the region.

- Good demand and willingness to pay higher prices for tropical hardwood in other regions including Asia, the Middle East, and North America.

- Reduced focus on supply of sawn timber to the EU by many tropical suppliers, particularly encouraged in Africa by strong demand for logs from China, and in South East Asia by on-going efforts to move into higher value products such as furniture.

- Continued substitution of tropical hardwoods for a range of modified temperate wood species and alternative non-wood products.

- Fashion changes, particularly the strong trend towards the oak look in EU and the fact that there is now very little demand for redwood finishes in the EU interiors sector.

- The on-going trend towards prefabrication in construction which is increasingly favouring tightly specified engineered wood products which are more readily accessible from domestic manufacturers than from the tropics.

- Intensifying enforcement of EUTR across the EU and the challenges and expense of legality due diligence in some tropical countries.

Loss of share for tropical veneer in EU market during 2017

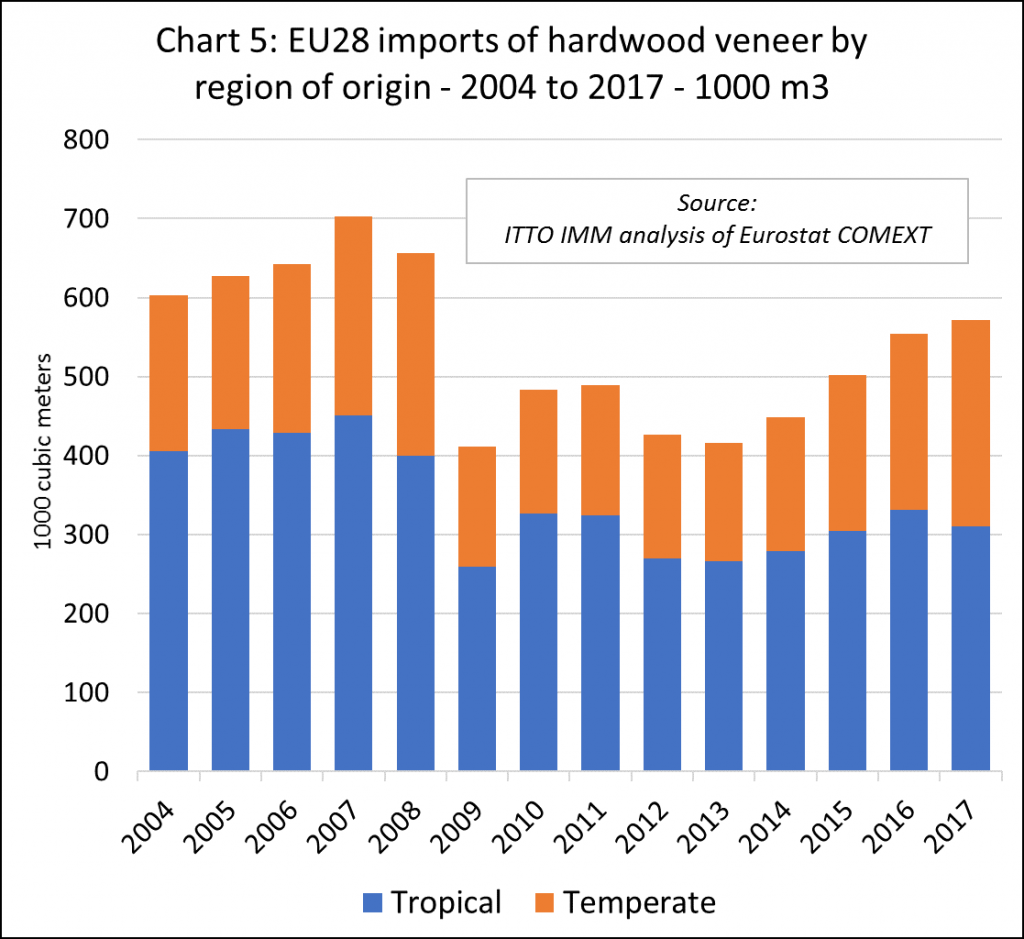

Many of the same factors contributing to the downturn in EU imports of tropical sawn timber are also now impacting trade in tropical veneer. Following three years of recovery, EU imports of hardwood veneer from the tropics declined 6% to 310,000 m3 in 2017.

The decline in EU imports of tropical veneer contrasts with a significant rise in imports of veneer from temperate countries which increased 17% to 262,000 m3 last year. Imports from Ukraine, the EU’s largest external supplier of temperate hardwood veneer, increased 9% to 89,000 m3 in 2017, while imports from Russia, the second largest supplier, increased 35% to 57,000 m3.

These increases in veneer imports from Eastern European countries during 2017 were driven partly by very weak exchange rates in the region, which has increased export competitiveness, and partly by policy measures to limit log exports and increase wood processing capacity in these countries.

In total, the EU imported 572,000 m3 of hardwood veneer in 2017, 3% more than in 2016. The share of tropical veneer in total EU veneer import volume fell from 60% in 2016 to 54% last year. (Chart 5).

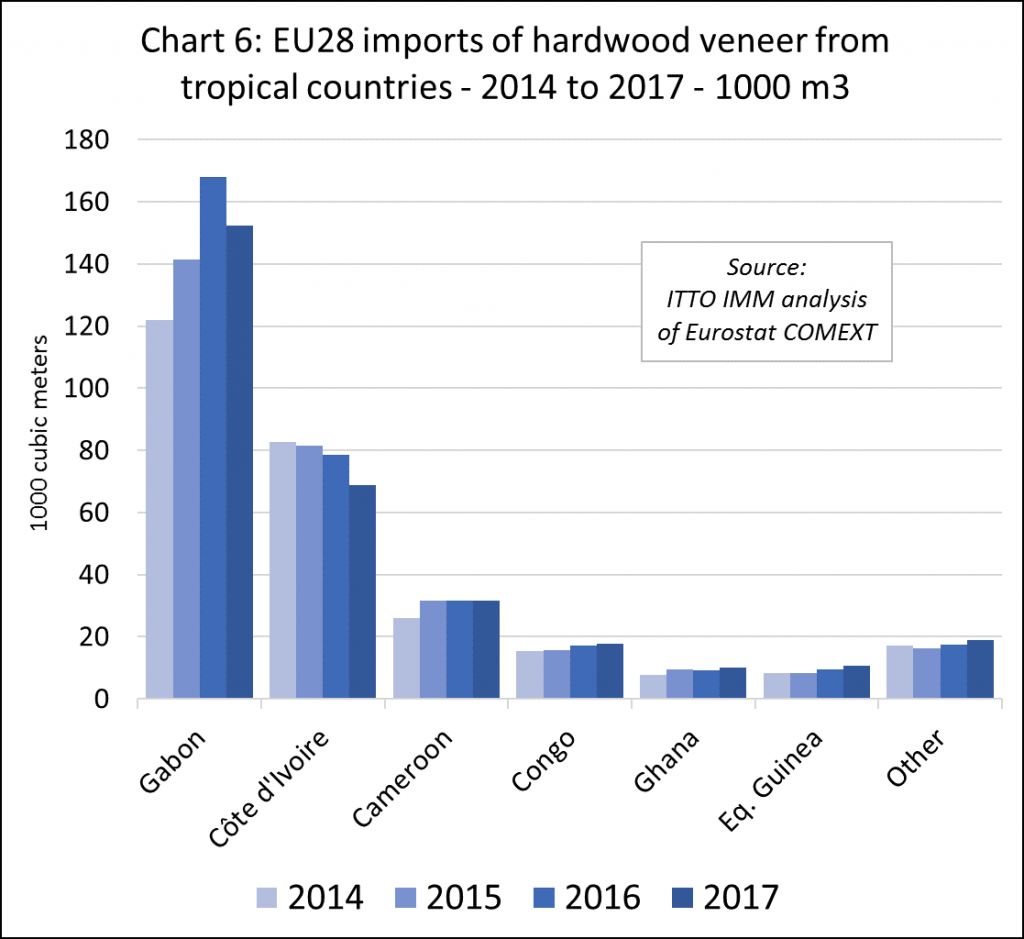

EU imports of hardwood veneer from Gabon, the leading tropical supplier, ended the year 9% down compared to 2016 at 152,000 m3. EU veneer imports also declined from Côte d’Ivoire in 2017, by 12% to 69,000 m3. Imports from Cameroon were stable at 32,000 m3 in 2017, but increased 3% to 18,000 m3 from Congo, 9% to 10,000 m3 from Ghana, and 11% to 11,000 m3 from Equatorial Guinea (Chart 6).

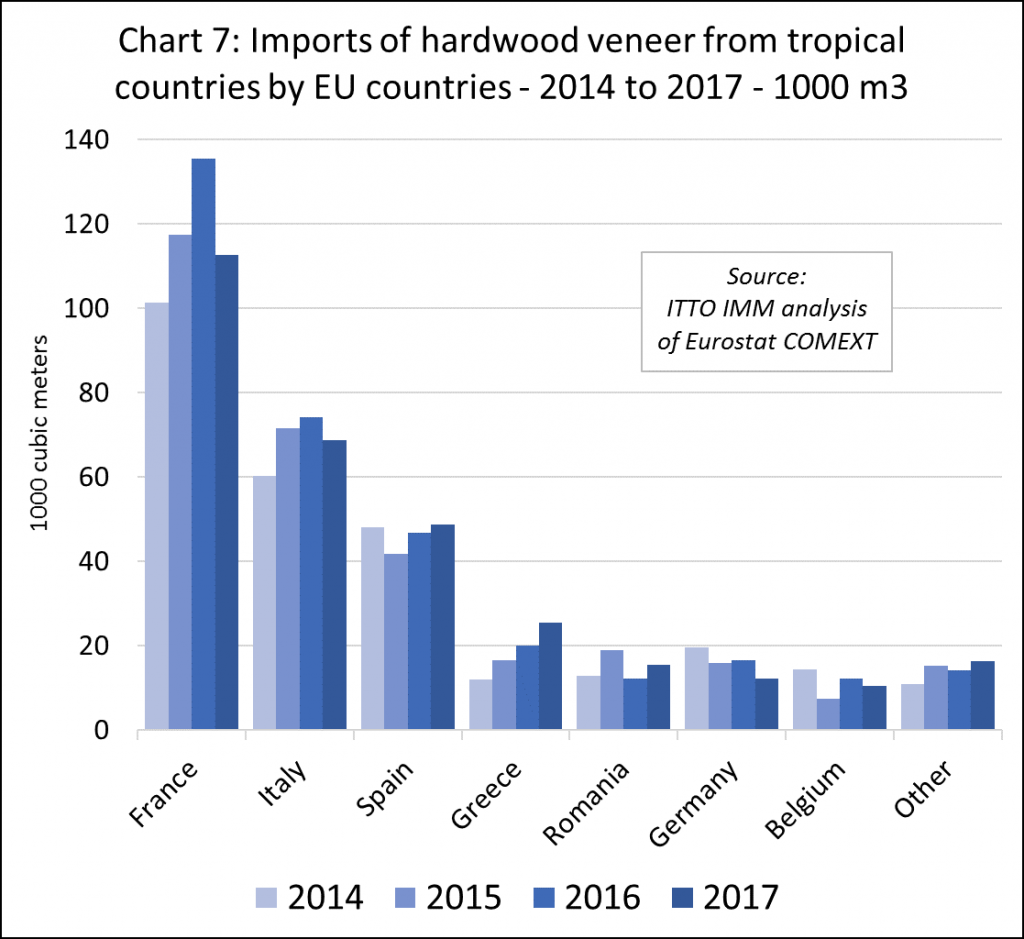

The downturn in EU imports of tropical veneer during 2017 was concentrated in France, Italy and Germany. Imports fell 17% to 113,000 m3 in France, 7% to 69,000 m3 in Italy, and 26% to 12,000 m3 in Germany. These falls were partially offset by rising imports in Spain (+4% to 49,000 m3), Greece (+27% to 25,000 m3), and Romania (+28% to 16,000 m3).

PDF of this article:

Copyright ITTO 2020 – All rights reserved