The latest Eurostat trade data to end October 2014 shows that tropical hardwood imports into the EU last year were only marginally better than the historically low levels recorded in the previous two years. Various factors account for this lack of import growth including lacklustre performance of the construction and joinery sectors in much of Europe during 2014, supply constraints and logistical problems (particularly for shipments out of Douala port in Cameroon), and the EU Timber Regulation which has encouraged buyers to focus on a more limited range of tropical suppliers to meet legality due diligence requirements.

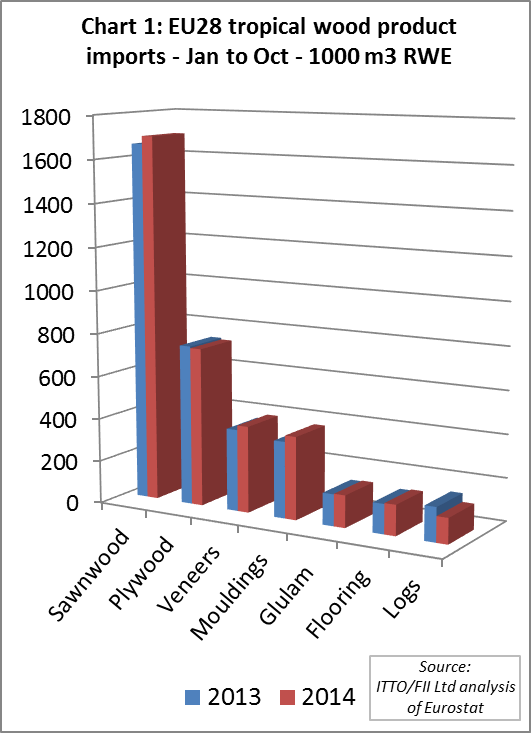

Total EU28 imports of all the main timber products from tropical countries were 3.63 million m3 in roundwood equivalent (RWE) terms in the first 10 months of 2014, 1.3% greater than the same period in 2013. In value terms, EU tropical timber imports in the first ten months of 2014 were €1.18 billion, only 0.7% greater than the same period the previous year. The volume of EU imports of tropical sawn wood, veneers, mouldings, glulam and flooring all increased slightly in the first 10 months of 2014. However there was a decline in EU imports of tropical plywood and logs (Chart 1).

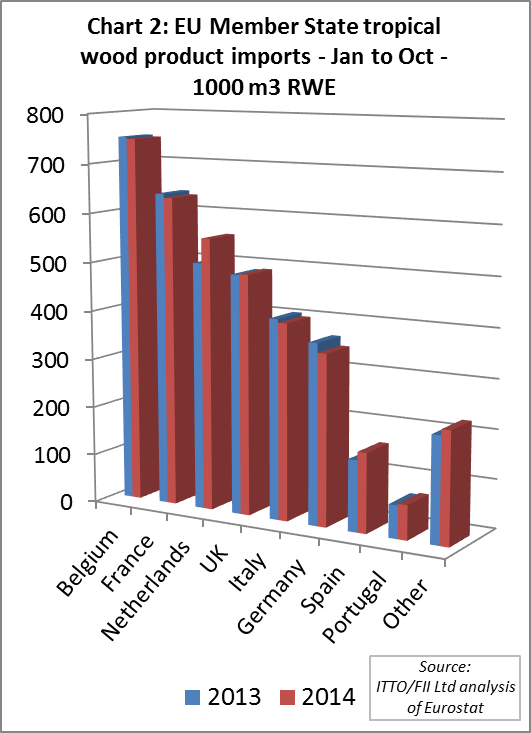

Total tropical hardwood imports into most EU countries remained fairly static at low levels between 2013 and 2014 (Chart 2). There were slight gains in a few countries including the Netherlands, Spain, Portugal and the UK, but these were offset by declines in Germany and Italy.

Belgium more important in supply to neighbouring countries

In the first ten months of 2014, the volume of tropical hardwood imports[1] into Belgium fell very slightly (-0.5%) to 748,000 m3 RWE. Belgium’s domestic market for tropical hardwood was still slow last year, but any weakness at home was offset by a rise in Belgium’s exports of tropical hardwood products to neighbouring countries. Belgium’s exports to other EU countries of all wood products identified as containing tropical wood was 251,000 m3 RWE in the first 10 months of 2014, 12% more than the same period in 2013. Most of this volume was destined for France, Netherlands and Germany.

Increased flow of tropical wood through Belgium suggests a continuing trend towards concentration of trade in a smaller number of larger importers close to the major ports. In part this reflects much tighter control of stock levels by merchants and manufacturers who prefer to buy small but regular volumes of mixed containers. To some extent this trend is being reinforced by EUTR which may be seen as another reason to avoid buying direct and instead rely on timber placed on the EU market by larger companies.

Weak construction depresses French imports

Direct imports of tropical wood into France were 632,000 m3 RWE in the first ten months of 2014, 1.2% less than previous year. The decline is partly due to the continuing weakness in the French construction sector last year. Already slowing in the first half of 2014, output in France’s construction sector contracted a further 0.6% in the three months to November according to the latest data from INSEE. Tropical hardwood plywood has also come under rising competitive pressure in France from imported Chinese plywood, European birch plywood, and other panel products.

Imports of sawnwood into France from Cameroon fell particularly dramatically last year. However there was a rise in French veneer imports from Gabon, encouraged by the EU’s decision to suspend the GSP tariff on okoume veneer from Gabon on 24 June 2014 and to backdate the suspension to 1 January 2014.

Netherlands tropical wood imports rise 10%

In contrast to France, the volume of tropical hardwood imports into the Netherlands increased 10% in the first ten months of 2014. Improving construction activity led to a particularly sharp increase in Netherlands imports in the first two quarters of 2014. However the rate of growth slowed in the third quarter of the year.

Demand for hardwood in the Netherlands has benefitted from the temporary VAT reduction on renovation activities implemented since early 2013. This is now due to remain in place until 30 June 2015 in an effort to offset continuing challenges in the Netherlands housing sector. These include low permit issuance, strict regulations for housing corporations, and government austerity.

Recognition of the Malaysian Timber Certification System since October 2013 alongside other PEFC systems and FSC for Dutch government procurement may well have boosted imports of tropical hardwood into the Netherlands last year. In the first ten months of 2015, Netherlands imports of Malaysian timber products were 246122 m3 RWE, up nearly 40% compared to the same period in 2013.

Slowing growth in UK tropical hardwood imports

After a sharp rise in the first six months of 2014, the rate of growth in UK imports of tropical hardwood slowed in the third quarter of the year. Overall, UK imports of tropical hardwood products were 490,000 m3 RWE in the first ten months of 2014, up only 0.4% compared to the same period in 2013.

The slowing pace of UK tropical hardwood imports was not due to any significant decline in the UK hardwood market. UK hardwood distributors remained very busy in the second half of 2014 driven by the on-going recovery in construction. However Chinese Mixed Light Hardwood plywood was taking a rising share of the UK market during 2014, largely at the expense of tropical hardwood plywood from Malaysia.

UK tropical hardwood demand also remains very heavily oriented towards sapele, with very little interest being shown in lesser known or secondary species. As a result the UK struggled to obtain adequate supplies, particularly with the slow movement of goods through Douala port in Cameroon during 2014. This encouraged some increased interest in Malaysian meranti in the UK last year. Sales of chemically and thermally modified wood products have also been rising in the UK, taking share from tropical hardwood.

Tropical wood regains some share in Italian market

Italian imports of tropical hardwood imports fell only slightly in 2014 despite evidence of a continuing sharp downturn in construction and other economic activity. Overall Italy imported 400,000 m3 RWE of tropical hardwood products in the first ten months of 2014, only 1.7% less than the same period in 2013. However this is hardly cause for celebration after seven years of near continuous decline in Italian tropical hardwood imports (from over 1.4 million m3 RWE in 2007).

The relative stability in Italian imports in 2013 and 2014 despite continuing contraction in end-use sectors, is partly due to tropical hardwood reclaiming some of the share lost to US hardwoods, particularly in the mouldings sector, as prices of the latter have risen. This boosted Italian imports of sawn wood from Gabon and Ivory Coast in 2014.

Italian timber merchants and manufacturers have also increased sales into other parts of Europe. For example EU internal trade data indicates that Italy’s exports of tropical hardwood plywood to other EU countries increased from 55,000 m3 in the first ten months of 2013 to 63500 m3 in the same period in 2014, most destined for Germany, Netherlands and France.

Indonesian wood fares well in Germany in 2014

Imports of tropical hardwood products into Germany were 348,000 m3 RWE in the first ten months of 2014, down 5.2% compared to the same period in 2013. After two years of robust growth, Germany’s construction sector contracted during 2014. Germany’s imports of tropical sawn hardwood declined from all four the country’s largest suppliers – Malaysia, Ghana, Cameroon and Ivory Coast.

However at least one tropical supply country fared well in Germany last year. German imports of Indonesian plywood, S4S sawn lumber, mouldings, veneers and flooring components all increased in 2014. This may be at least partly due to mandatory SVLK certification of Indonesian products. Implementation of a tough EUTR inspection regime in Germany and the government’s decision to confiscate a consignment of African wenge logs due to an alleged breach of the law, have sensitised importers to the need for legally verified timber.

Pick up in Spanish and Portuguese imports

After several years of contracting demand, there was a pick-up in demand for tropical hardwood products in Spain and Portugal in the first 10 months of 2014. In RWE terms, imports into Spain were nearly 12% higher than the same period the previous year, while imports into Portugal were 5% higher. This is an encouraging sign that the painful structural reforms imposed by both countries in the wake of financial crises are beginning to stimulate more economic activity.

Although Spain’s imports of tropical hardwood from Cameroon fell last year, the country was importing more from Ivory Coast, Brazil, Gabon and the Congo countries. Portugal was importing more from Brazil in 2014. Spain’s tropical hardwood imports consist primarily of sawn wood and veneers, whereas Portugal imports mainly tropical sawn wood with a declining volume of logs.

EU tropical hardwood log imports slide even further

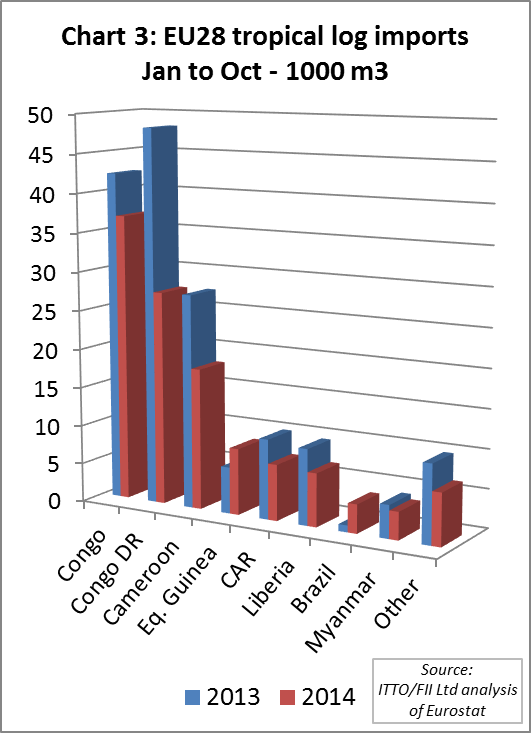

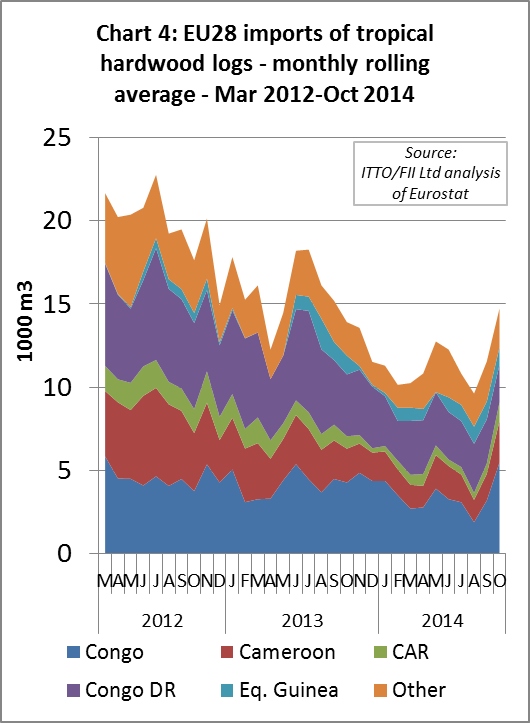

EU imports of tropical hardwood logs were 119,000 m3 in the first ten months of 2014, 25% less than the same period of 2013. Imports fell particularly dramatically from the Democratic Republic of Congo, down 43% at 27000 m3 in the first 10 months of the year (Chart 3). Analysis of monthly data indicates that while the general trend in EU imports of tropical logs has been downwards over the last 3 years, there was a sharp increase in imports in September and October 2014.

[1] Refers to total roundwood equivalent volume of logs, sawnwood, mouldings & decking, veneers, plywood, flooring and glulam

Minor recovery in EU imports of sawn tropical hardwood

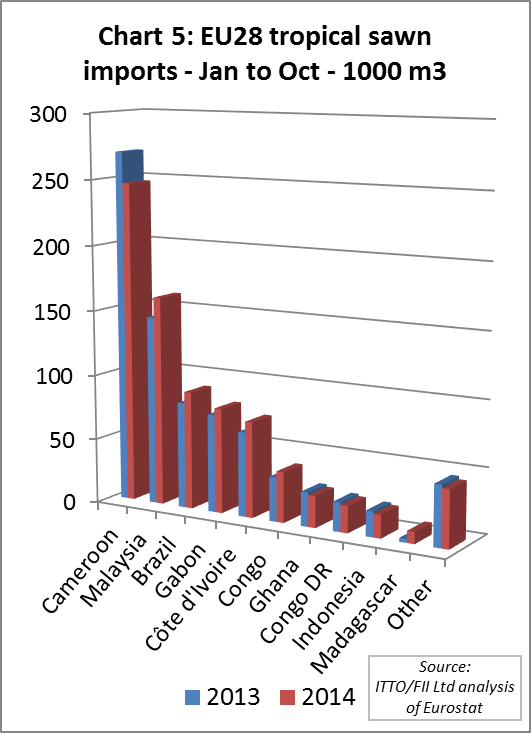

EU imports of sawn tropical hardwood were 806,000 m3 in the first 10 months of 2014, 2% more than the same period in 2013. Imports from Cameroon fell 9% to 247,000 m3 (Chart 5). However, this decline was offset by rising imports from Malaysia (+11% to 161,000 m3), Brazil (+11% to 90,000 m3), Gabon (+7% to 81,000 m3), Ivory Coast (+13% to 73,000 m3) and the Republic of Congo (+14% to 39,000 m3).

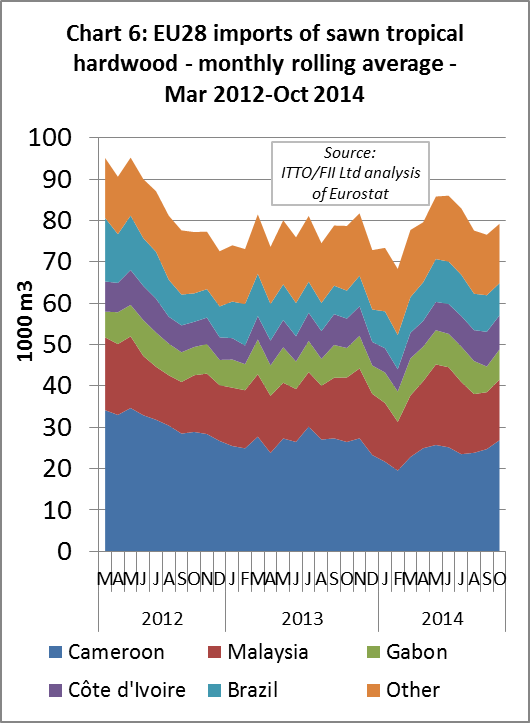

Monthly data indicates that after a slow start to 2014, EU imports of sawn hardwood increased strongly between March and June (Chart 6). Imports fell away again in third quarter of 2014 as consumption had not kept pace with imports and European stocks had begun to build.

However there was a slight uptick in EU imports in October 2014, mainly because wood at last began to flow more freely from Cameroon. This followed introduction of emergency measures by the Cameroon authorities to reduce serious congestion at the port. These measures included commissioning of new cranes and the allocation and redevelopment of more transit space for timber shipments.

Looking forward, port congestion is widely expected to become less of a problem in Cameroon following the recent announcement by the Minister of the Economy, Planning and Regional Development that the Limbe Deep Seaport supported by South Korean investment should become operational during 2015. The Kribi Seaport in Cameroon, supported by US$567 million of Chinese investment, is also reported to be 60% complete and is expected to provide a large new harbour serving all of Central Africa.

Better EU demand for Asian decking in 2014

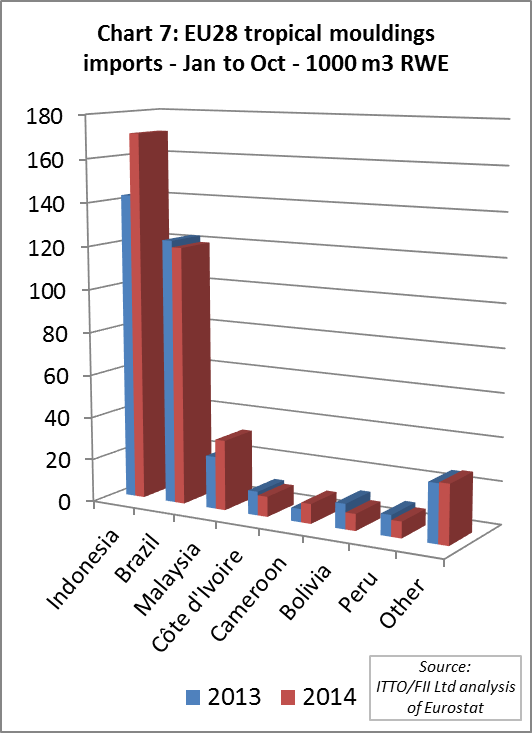

EU imports of tropical hardwood mouldings and decking in the first 10 months of 2014 were 385,000 m3, 8% more than the same period in 2014. Imports from Indonesia during the period were 171,000 m3, a 20% gain on 2013 (Chart 6). Imports from Malaysia also increased 34% to 33,000 m3. However imports from Brazil declined 2% to 120,000m3.

Brazilian decking products were the target of a Greenpeace campaign in Europe in 2014. Several large European retailers put their sales of ipe decking on hold following Greenpeace allegations that legal documentation provided by Brazilian exporters does not meet EUTR requirements.

According to a recent report by the European Timber Trade Federation, investigations by the Belgian EUTR authorities and customs into six containers of ipe decking imported into Belgium alleged by Greenpeace to derive from an illegal source were still ongoing in December 2014. The Belgian authorities were awaiting ‘clarity’ on legality documentation from Brazil and the Belgian importers.

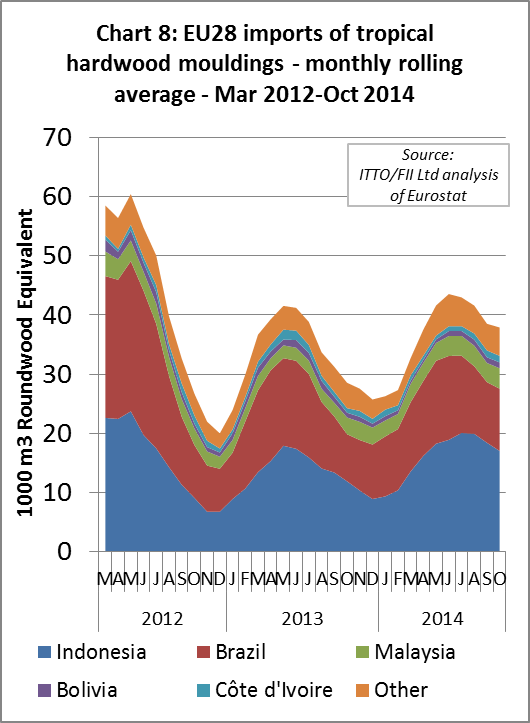

Monthly data for 2014 reveals the usual steep rise in EU imports of moulding and decking products during the second quarter, levelling off in June/July and then declining towards the end of the year (Chart 8). Overall the European summer decking season in 2014 was marginally better than in 2013 when imports were seriously undermined by over-stocking from the previous year.

Although European importers are quite optimistic about demand for decking in the coming 2015 season, there are concerns that higher prices for tropical hardwood decking will lead to increased substitution by alternative products, notably wood plastic composites. Indonesian bangkirai exporters are quoting significantly higher prices this year due to rising log and labour costs. The relative weakness of the euro against the dollar is a further disincentive for European importers. Supplies of Brazilian decking are also expected to be limited as more product is diverted to the more buoyant U.S. market.

PDF of this article:

Copyright ITTO 2020 – All rights reserved