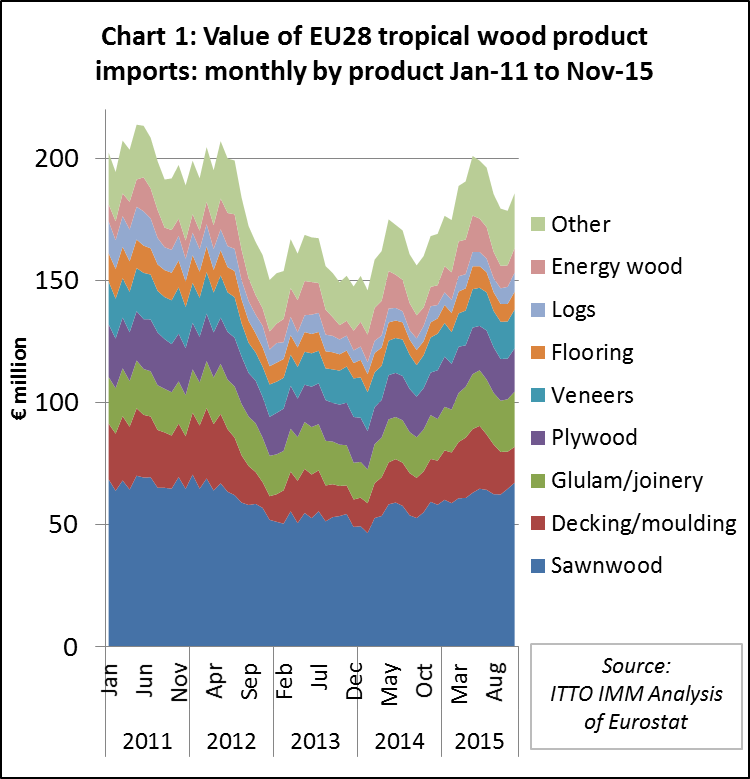

European imports of tropical timber showed healthy growth between January and November of last year, with total value rising 15% to €2.059bn (2014: €1.788bn). The first quarter of 2015 was particularly strong, with an increase of 20.5% over the still relatively weak first three months of 2014. After a dip in summer 2015, imports picked up again between September and November last year (Chart 1).

Sharp increase in EU imports of tropical LVL, mouldings & flooring

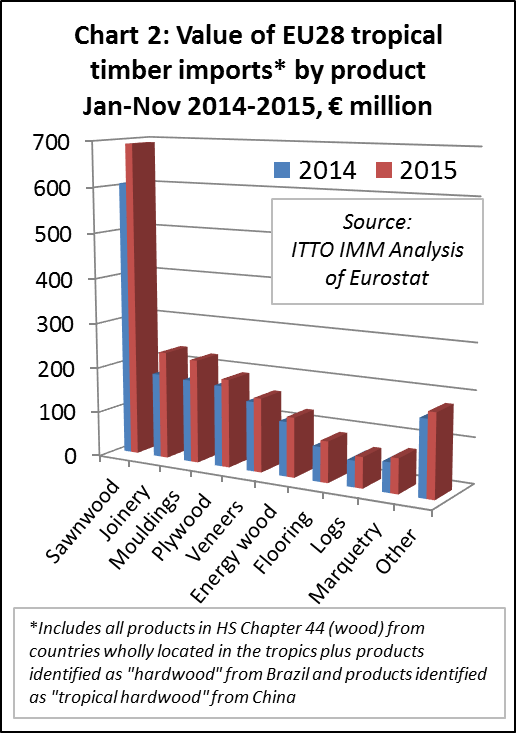

European imports of all major tropical wood products increased in the first eleven months of 2015. There was particularly strong growth in the value of EU imports of tropical joinery products (mainly LVL) which increased 27.2% to €237.2 million, together with mouldings/decking which increased 25.3% to €228.1 million. There was also good recovery in the value of sawn wood imports, which were up 14.3% at €692.3 million. After many years of consistent decline, there was even a minor rebound in EU imports of tropical logs, up 18% from a small base to €67.4 million. A similar increase (+18.7% to €89.7 million) was recorded in imports of tropical wood flooring. However imports of tropical plywood (+9% to €194m), veneers (+6% to €162m) and energy wood (+9% to €130m) only increased by single-figure percentages in each case (Chart 2).

Broader-based recovery in the EU tropical wood imports

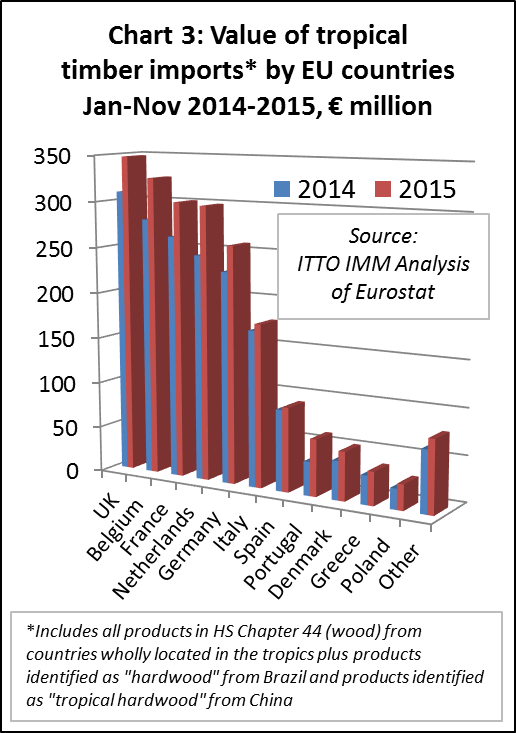

While the growth that occurred in EU tropical wood product imports during 2014 was due mainly to rising consumption in the UK, the 2015 recovery was much more broadly based. In the first eleven months of 2015, there was double–digit growth in tropical wood import value into Belgium (+16% to €325m), Denmark (+25% to €53m), France (+14% to €301m), Germany (+12% to €258m), the Netherlands (+22% to €298m) and the UK (+12% to €348m).

Among crisis-ridden southern European countries, Portugal fared very well, with a sharp 67.7% increase in imports to €62m during the first 11 months of 2015. The rise in imports into Italy (+4% to €177m) and Spain (+4% to €92m) was more moderate but heading in the right direction. Even Greece recovered ground last year with import growth of 16% to €36m (Chart 3).

The rise in the euro value of EU imports is partly due to exchange rate movements. The average euro/US$ exchange rate was 1.11 in 2015 compared to 1.32 in 2014 implying that inflated prices for many imported wood products last year. However closer analysis shows significant growth in the volume as well as value of tropical wood imports in most product sectors.

EU tropical sawn imports exceed 1 million m3 in 2015

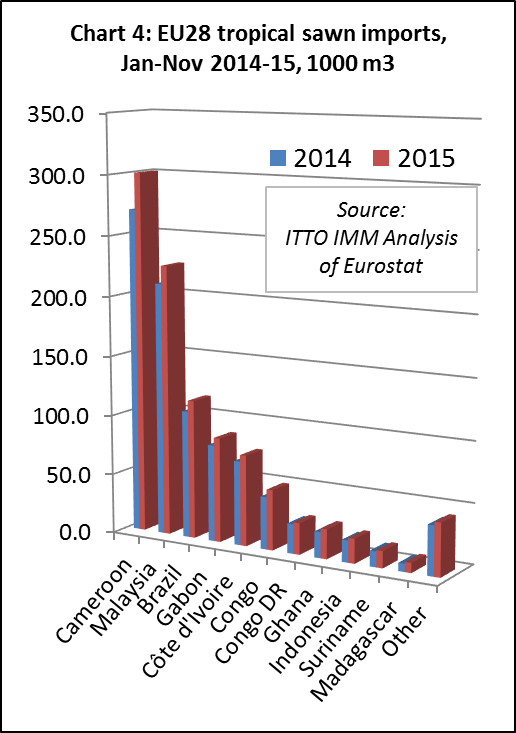

EU imports of tropical sawn wood in the first 11 months of 2015 were 992,000 m3, 9% more than the same period the previous year. It’s therefore almost certain that EU imports for the full year will exceed 1 million m3 for the first time since 2012. While an encouraging landmark, this is still well down on levels prevailing before the crises when annual imports exceeded 2 million per year.

Cameroon, from which the EU imported 300,800 m3 in the first eleven months of last year, an increase by 11%, cemented its leading position as the EU’s most important supplier of tropical sawn wood. The four next largest suppliers all registered lower growth rates: imports increased by 7% from Malaysia to 225,700 m3, by 9% from Brazil to 115,700 m3, by 8% from Gabon to 87,200 m3, and by 8% from Ivory Coast to 75,800 m3.

However there was an above average in imports from several smaller suppliers including Congo (+15% to 50,200 m3), Ghana (+14% to 24,700 m3) and Indonesia (+12% to 20,400 m3) (Chart 4).

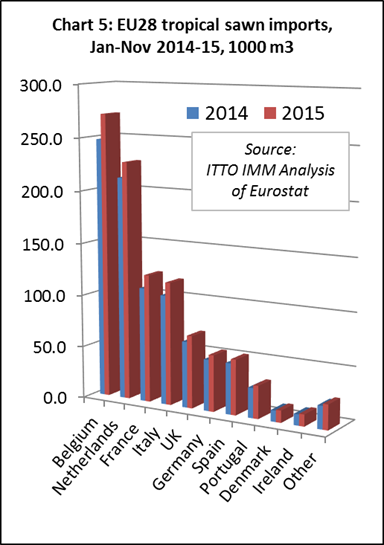

Consistent growth in tropical sawn imports across the EU

All the largest EU markets imported more tropical sawn wood in the first eleven months of 2015 compared to the previous year. Growth rates were quite evenly spread, ranging between +7% and +12% (Chart 5).

Belgium was the largest single importer of tropical sawn wood in 2015, with volume rising 10% in the first 11 months of the year to 271,000 m3. Much of this volume is destined for neighbouring EU countries rather than consumed in Belgium. Imports into the Netherlands were also on the rise last year, up 7% to 227,400 m3. This is a reflection both of increased domestic construction activity in the Netherlands and of the country’s important role as an entry-point for hardwoods distributed throughout the continent. There was 12% growth in imports by France and Italy, to 122,300 m3 and 117,400 m3 respectively, particularly encouraging as these countries have been very slow to recover from the market downturn.

Meanwhile the positive trend in imports by the UK and Germany continued, with a 10% increase in each case to 69,400 m3 and 53,900 m3 respectively. Imports into Spain and Portugal, too, experienced healthy growth rates: Spain’s imports rose by 9% to 52,800 m3 and Portugal’s by 10% to 31,300 m3.

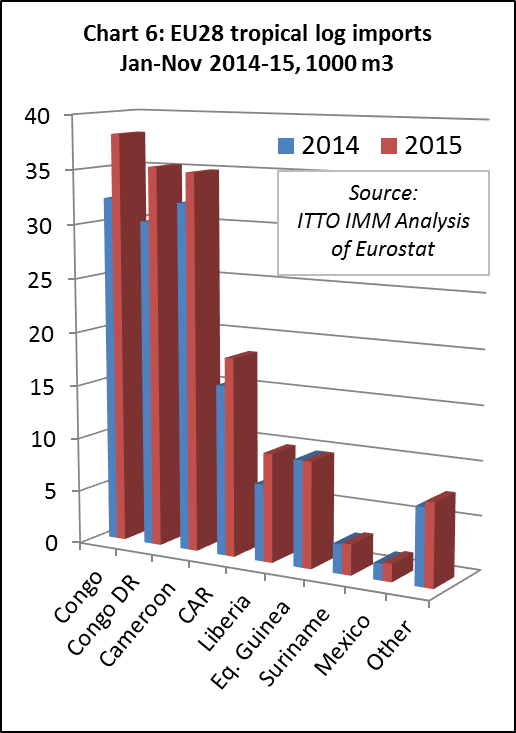

Log imports on the way up again

European imports of tropical logs gained ground in the first eleven months of last year, rising 14% to 158,954 m3. Imports were almost exclusively sourced from African countries although Suriname is now established as a small but consistent supplier of logs to the EU, particularly of denser and FSC-certified wood for sea defence works and similar heavy-duty applications.

EU imports of tropical logs increased sharply from Congo (up 18% to 38,136 m3), Democratic Republic of the Congo (up 17% to 35,277 m3), Cameroon (up 9% to 34,936 m3), and Central African Republic (up 16% to 18,471 m3). There was also a resumption in log imports from Liberia, which jumped 41% to 10,094 m3 in the first 11 months of last year (Chart 6).

Much of the growth in EU imports of tropical logs was concentrated in Belgium and Portugal, the second and third most important EU importers after France, which at 63,943 m3 only imported 1% more than in 2014. Belgium imported 28,979 m3 between January and November 2015, more than twice as much as the year before (+122.6%). Portugal shows a similar trend: at 28,226 m3 the country imported 57.9% more than in 2014. And Italy, too, boosted its import volume by 49% to 15,583 m3.

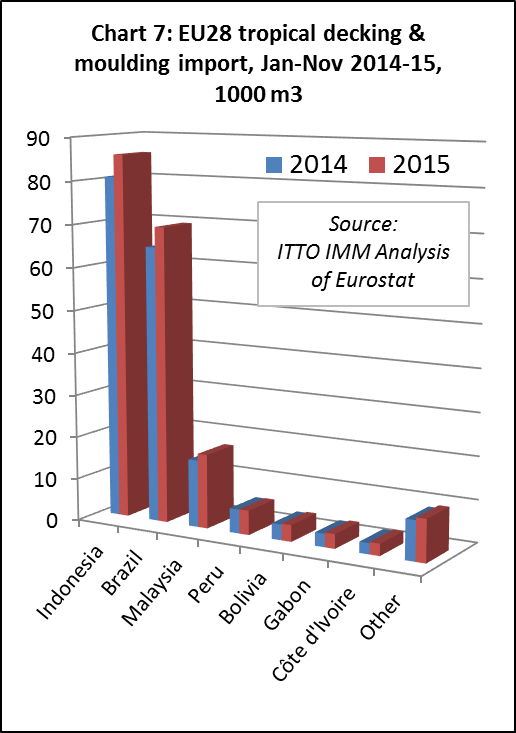

Growth in decking/moulding imports despite rising prices

EU imports of “continuously shaped” wood (HS code 4409), which includes both decking products and interior decorative products like moulded skirting and beading, increased 7% to 199,000 m3 in 2015. EU imports of tropical decking and moulding products increased from all the leading suppliers including Indonesia (+6% to 85,800 m3), Brazil, (+7% to 69,600 m3) and Malaysia (+10% to 17,500 m3). (Chart 7).

The 7% rise in the volume of EU imports of tropical moulding/decking in the first 11 months of 2015 is considerably less than the 25% gain in import value. This is because most product is sourced from South-East Asia and Brazil where suppliers invoice in US$ dollars (in contrast to African suppliers who generally invoice in euros). It is also clear that the steep fall in container freight rates experienced during the course of 2015 was insufficient to offset the rise in US dollar-based prices. Nevertheless it is encouraging that European import volume showed some growth despite rising prices.

EU recovery “at a moderate pace and amid risks”

It remains unclear whether these encouraging signs will turn into a lasting growth trend. The German IFO Institute’s most recent Eurozone Economic Outlook suggests that European economic recovery is likely to continue “at a moderate pace and amid risks”.

IFO estimates that real GDP in the euro-zone was 1.5% in 2015 and that growth will continue by 0.4% in both the first and second quarter of 2016. Private consumption is identified as the main driver behind the upturn stimulated by a renewed drop in oil prices. There is also expected to be a significant stimulus from fiscal and social policy, particularly in Germany, not least due to far higher government expenditure on consumption and transfers related to the influx of refugees. Construction investment is also expected to grow sharply in Germany over the forecasting period.

According to IFO, main risks facing the European economy are unrest in the Middle East, which could yet lead to a surge in oil prices. Moreover, the structural transformation of the Chinese economy involves risks for Europe as well, as it could lead to capital outflows from the emerging countries. “This, in turn, may cause strong financial market turbulence, or even exchange rate crises”, risks to which the euro-zone has proven particularly vulnerable.

PDF of this article:

Copyright ITTO 2020 – All rights reserved