In 2012, wooden floor consumption in Europe (excluding the UK) is estimated at 91 million m², a 4% decline compared to the previous year. Last’s years decline is a reversal of the trend in 2011 when there was a brief revival in European parquet consumption following a sharp fall in consumption following the financial crises between 2008 and 2010.

The 2012 consumption estimate is derived from FEP (European Federation of the Parquet Industry) based on a preliminary survey of country representatives at their recent meeting held at the DOMOTEX fair in Hannover. A more comprehensive assessment of consumption will be published at FEP’s annual General Assembly in June 2013.

In publishing their preliminary assessment, FEP stress that market conditions vary considerably between European countries and that this variation has increased. The German-speaking countries of central northern Europe are performing well with consumption rising slightly in 2012. Scandinavian and Nordic countries are reporting stable consumption or slight declines but no indication of a significant downward trend. However, market conditions in southern Europe, including in the traditionally large consuming countries of Italy and Spain, are very challenging with consumption falling more than 15% in 2012. There were also quite significant falls in consumption in France, Belgium and the Netherlands.

As regards the product mix, FEP report that strong demand for one-strip planks has helped compensate the decline in other product categories.

Apart from the shaky economy, major challenges for the sector result from high energy costs, continuously stiff competition, expensive transport & logistics, extremely high unemployment rates in some important EU regions and the volatile and uncertain EUR/USD exchange rate.

On the other hand, FEP are optimistic that the “overall EU parquet industry remains strong and resilient, fuelling the belief that it will successfully rebound as soon as the overall economic indicators take a positive turn”.

On releasing the results, FEP identified two factors which suggest better times might lie ahead: first, the “never ceasing innovative product creativity and evolutionary design of European parquet manufacturers”; and second “the multiple economic forecasts for 2013 which converge on a more optimistic business development in the half of the year, which should also boost overall consumer confidence.”

Optimism at Domotex that better times lie ahead

While Europe’s central role in the international flooring industry has diminished in recent years, Domotex held during January every year in Hanover, Germany, still claims to be the world’s leading trade show for the international flooring coverings sector.

The Domotex organisers issued the usual positive press release reporting another successful show in 2013. However early estimates of visitor numbers of around 40,000 were down significantly compared to 2012 when close to 46,000 attended the show. This may be partly explained by many of Germany’s largest flooring manufacturers choosing not to exhibit at Domotex this year and to focus instead on the BAU biannual German building show held a few days later in Munich.

Nevertheless, the Domotex show remains a truly international event. It attracted 1,350 exhibitors from 60 nations, including producers and suppliers of carpets, textile floor coverings, resilient floor coverings, parquet flooring and laminated coverings as well as installation, cleaning and application technologies. More than 60% of visitors were from outside Germany with over 80 nations represented. Half were from European countries other than Germany, while 21% came from Asia and 11% from the Americas. Attendance from Asian countries and North America increased compared to last year. The show’s attendees once again consisted primarily of wholesale and specialized retail buyers, at 30% and 20% respectively

Wooden flooring producers exhibiting at the show appeared quite optimistic about prospects for 2013. There was a widespread view that the crises may be nearly over and many producers were expecting sales to improve in 2013. Companies were generally reporting robust sales in Germany, and stable demand in Scandinavia and the UK. On the other hand, Italian and Spanish manufacturers were reporting very poor domestic demand. As a result they were focusing more on exports to other European countries, the Middle East and the USA.

As in previous years, the Domotex show again emphasised the extent to which oak dominates in the European flooring sector. Oak products were found on virtually every single stand, both solid wood and engineered. Many laminate producers were also reproducing artificially the “oak look”. Very few other wood species were on display – a bit of ash, walnut and elm, some maple for specialist sports floors, only a tiny quantity of tropical woods, and no cherry at all. There was also a bit of bamboo.

To bring diversity to the displays, the emphasis again was on the wide range of staining, varnishing, brushing, and other surface treatments that can be applied to oak. Oak flooring came in every shade from limed-white to black stain and finishes ranged from clean modern through to antique and rustic.

European oak preferred

The vast majority of European producers were using European oak rather than American white oak. Although some manufacturers claim otherwise, the widespread use of European oak instead of American white oak cannot be due to any real preference by European consumers. Since most oak flooring products are stained or subject to other treatments, consumers are very unlikely to be able to tell the difference between oak species.

The choice of European oak by European manufacturers is driven primarily by supply issues. Manufacturers are able to source lumber and strips most competitively from European sawmills, especially in the lower grades. Local sourcing also helps reduce risks associated with volatile exchange rates, long transport routes and the potential for delayed deliveries.

Chinese wood flooring manufacturers at the show were also focusing heavily on oak product ranges. They were equally keen to stress that these products are composed entirely of European oak (as opposed to Russian or American) in the belief that this aligned to European tastes. However in practice, it is well known that manufacturers in China often mix oak species in their products and it was difficult to assess the actual origin of the wood on display.

Strong fashion for wider boards

Domotex demonstrated a strong fashion in Europe for wider boards. Most stands were displaying wide solid boards or one-strip multi-layered products. There were very few narrow solid boards or two-strip or three-strip engineered products. Some high-end producers were offering very wide boards in excess of 8 inches. Even laminate products were printed with wide board surface patterns.

Wood flooring manufacturers at Domotex suggested demand for oak will remain strong for the foreseeable future. Some believed the strong fashion for walnut may have peaked, although walnut floors are still selling well. There still seems little prospect of any significant increase in demand for beech or cherry in the European flooring sector. Prospects for maple are a little better, with some manufacturers expecting rising demand for maple in high performance sports floors and in floors for high-traffic public areas.

Tropical wood species are generally out of fashion in the European flooring sector. These species also tend to be considered high risk under the EU Timber Regulation unless backed by FSC or other third party forms of legality verification. As a result, more limited availability is likely to increasingly restrict tropical wood floors to a high value niche in the future.

Integrating wood flooring into interior sign

A key theme of Domotex 2013 was to try to better integrate floor coverings into the broader field of interior design. This was encouraged by the show organisers through introduction of the “Flooring Deluxe” exhibition to Domotex this year. The exhibition involved 15 specially arranged booths (so-called “Concept Rooms”) with installations created by young designers in collaboration with floor covering manufacturers.

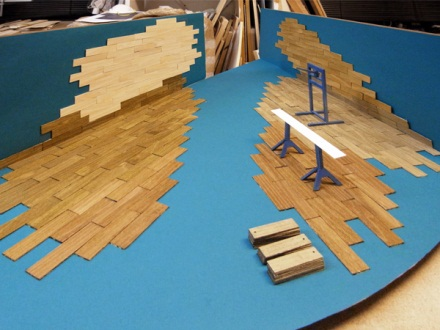

The wood flooring section of “Flooring Deluxe” was represented by Poland’s Baltic Wood working in collaboration with the German designer Mark Braun. The resulting installation displayed embossed wood parquet in a domino-like formation on both wall and floor. This was set against a petrol-blue background (see photo). According to Braun, the aim was to consciously break with wood parquet’s conventional application to emphasise its natural colour and surface feel. Another aim was to reintroduce the idea of wood as wall panelling.

After three days of voting by an expert panel and visitors, Braun’s wood display was recognized as the best project in the floor coverings category. The result emphasises the enduring attraction of real wood floors and panelling. It also suggests strong consumer interest in innovative designs which combine wood’s natural texture with modern materials and bold colours.

Installing Mark Braun’s award-winning display at Domotex

Decline in European laminate flooring sales during 2012

Another indication of challenging market condition in the European flooring sector in 2012 is provided by data released by the Association of European Producers of Laminate Flooring (EPLF). The association represents the leading producers of laminate flooring in Europe. The 22 member companies account for around 55% of the global market for laminated floors and around 80% of the European market.

In recent years, laminate flooring has taken a rising share of the European floor covering market, mainly at the expense of textiles. According to market research by Intercontuft, laminates share of this market increased from 12.7% in 2004 to 14.3% in 2010 (wood’s share increased from 5.1% to 5.6% during the same period). European and international production capacity of laminate flooring increased rapidly in the years before the recession. However, during the recession, excess capacity and on-going moves by manufacturers to replace décor papers with direct printing meant that prices for laminate flooring remained low. High street prices for laminate flooring may be as low as €5-10/m2 with little variation between looks and specifications.

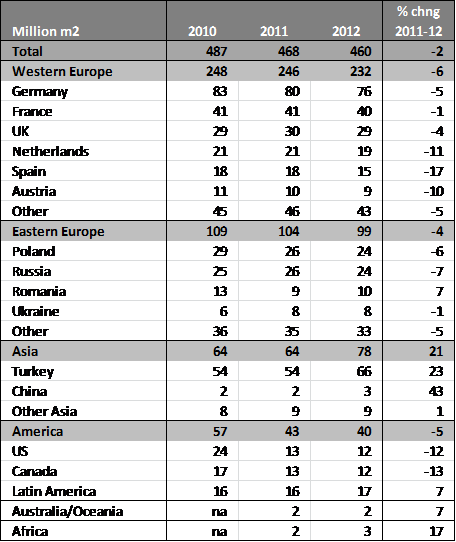

The problems associated with low pricing and tight margins in the sector are now being made worse by declining consumption. The latest EPLF data shows that European sales of laminated flooring by EPLF members fell sharply during 2012 (see table). Last year the volume of laminate flooring sales fell 6% in Western Europe and 4% in Eastern Europe. The decline in sales was apparent across nearly all the leading European markets. European manufacturers also suffered from declining sales in North America. However manufacturers have had some success to offset these losses by increasing sales to other markets outside Europe, including Turkey, Latin America, China and Africa.

Sales of laminate flooring by EPLF members 2010-2011

Laminate flooring industry seeks to do more than duplicate wood

Reviewing information supplied by the EPLF, demand for laminate floors in Europe is still heavily oriented around the “all-rounder oak”, as it is in the real wood sector. There is a strong preference for the wide “country-house” plank, with or without a V-joint. However EPLF also note that there are signs of three-strip planks re-gaining popularity in the laminates sector, although less for isolated installations and more often as part of an integrated interior design scheme. The trend is towards floors with a consistent pattern direction to create a more elegant appearance. For tile designs, large, rectangular formats are preferred, which create a spacious effect in larger areas.

In recent years, the laminates industry has invested heavily in perfecting digital printing technologies to allow near perfect replication of the look of real wood and other natural materials. However, according to EPLF, the industry now has ambitions to move beyond mere duplication. It is challenging real wood and other floor types by seeking to deliver finishes which, while authentic and “natural”, are also unique and striking. For example the heavy knottiness of pine may be combined with the medium-brown shades of oak, perhaps with subtle white effects added. Elm, a pale wood with dark beige tones in nature, may be given a dark shade with reddish brown effects.

EPLF note that the range of possibilities to modify laminated decors is expanding all the time, now including colouring, bleaching, etching, whitewashing, oiling, and waxing. These techniques can be used not only to duplicate nature, but to produce “never-before-seen” extreme surface finishing styles. This is combined with sophisticated haptics and texturing so that, according to the EPLF, “the floors appear more interesting and life-like than the wood from which they were modelled”.

EPLF note that these same principles are also being applied to stone designs. The industry is now focusing attention on improving and promoting stone decors – including slate, marble and granite – which to date have been far less popular than wooden decors.

It’s an ambitious agenda, to try to do better than nature through use of modern technology and materials. The response of consumers is still uncertain. For now, the majority still seem to prefer the look and feel of natural oak.

Technical developments

In addition to delivering new designs, the laminates industry is seeking to build market share through improved technical performance. According to Dr. Theo Smet, Chairman of the Technical Committee of the EPLF: “The response of the EPLF members to the generally tough economic conditions is a clear commitment to technical quality, the development of innovative products, further transparency in terms of technical features and work on complete laminate flooring systems. This means combining laminate flooring with what lies beneath them, for example taking account of underfloor heating and cooling, soundproofing, cleaning, care and environmental aspects.”

Participation in the European laminates market is a complex and demanding process requiring compliance to a wide range of technical standards. The EPLF assists members through active participation in on-going standardisation work in Europe. For example it is participating in Technical Committee CEN TC 134 (Laminate, Textile, Resilient) which is now revising the European Norm (EN) 14041. This standard introduces environmental aspects into CE marking of flooring materials, especially relating to indoor air quality, VOC emissions and potentially hazardous substances. EPLF also recently contributed to finalisation of EN 16094 (test procedures for determining resistance to micro scratches) and drafting of EN 16354 (covering requirements for underlay materials). Further standardisation projects include the revision of the standards for laminate floor coverings EN 13329 (thermoset resins), EN 14978 (electron beam-hardened acrylic surfaces), and EN 15468 (direct printing).

Environmental groups react to EUTR

The EU Timber Regulation (EUTR), which regulates illegal timber trade, entered into force on March 3. Import of illegal timber is prohibited under EUTR. Failure to comply can land importers with up to two years imprisonment or a 50,000 Euro fine, in addition to confiscation of timber. Companies importing timber into the EU are required to carry out ‘due diligence’ to ensure that the timber was logged according to the producer country’s laws, including for example, knowing the details of each logging licence under which timber is cut and taking measures to verify that all relevant laws are followed.

An immediate effect of EUTR has been to encourage campaigns by European environmental groups targeting specific species and supply sources perceived to be high risk of illegal logging. So far, the main focus has been on tropical products and countries. Following a report that illegal Liberian timber was found in a French port, Global Witness campaigner Alexandra Pardal told the BBC: “Almost all timber from tropical rainforests carries a high risk of illegality and should be checked out thoroughly – if there’s any suspicion at all, don’t touch it”. A recent Greenpeace report singled out the Democratic Republic of Congo as “clearly extremely high risk”.

China is also frequently mentioned by environmentalists as a participant in the illegal trade. In March, the WWF’s Beatrix Richards told the BBC “much of the illegally traded timber comes from central Africa and South-East Asia, with a significant proportion being processed in China and Hong Hong before being shipped to EU nations, particularly the UK”.

Timber exporting countries in both Africa and South East Asia are negotiating bilateral Voluntary Partnership Agreements (VPAs) on timber trade and forest governance with the EU. A key objective of the VPAs is to implement rigorous procedures for “Legality Licensing” of all wood exported from partner countries into the EU. Wood covered by these licences will be exempt from control under the EUTR. However the conclusion of some VPAs has been delayed and no tropical country is yet in a position to issue a VPA license. In the meantime, wood imported from VPA countries must trade under the EUTR.

PDF of this article:

Copyright ITTO 2020 – All rights reserved