The report this month focuses on flooring. The European flooring sector is going through a major period of change, and is also a good indicator of what is happening in the wider European wood industry. It’s a valuable source of information on the latest economic and fashion trends, and one of the few sectors where it is possible to analyse directly the competitive position of wood in relation to non-wood materials. On this last issue, the flooring sector clearly demonstrates how technological innovation in other material sectors continues to put enormous pressure on wood’s market position. It shows how the European wood sector is fighting back with initiatives focusing heavily on high product quality and strong environmental performance. It also shows how the European wood sector is responding to weak and negative growth in domestic markets by targeting export markets in other parts of the world, notably China. In doing so, it is seeking to exploit its particular strengths in the fields of design, technical innovation, product quality, and environmental performance.

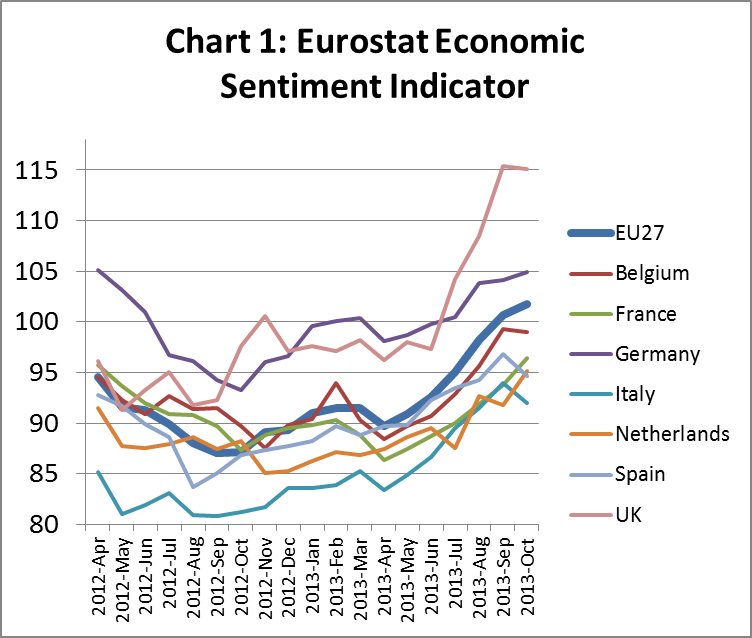

The Board of Directors of FEP, the European wood flooring association, met recently to discuss the market situation and recent economic indicators. There was some positive news: the latest Economic Sentiment Indicator of the EC continued its upward trend, increasing sharply both in the euro area and in the EU. In October 2013, the indicator rose for the sixth successive month in both regions, marking a two-year high in the EU (Chart 1).

Information provided by individual country representatives at the meeting indicated wide variations in market conditions at country level. However, overall they suggested that production fell further in the first half of 2013. Market conditions have also remained difficult in the second half of the year. Only slow recovery is expected in 2014.

The situation in individual European markets is as follows:

- Austria – harsh weather conditions in Austria led to a 2% decline in wood flooring consumption in the first half of 2013 compared to the same period in 2012.

- Belgium: wood flooring consumption contracted by more than 5% year-on-year in the first six months of 2013. However there are some early signs of economic improvement.

- Denmark: after a stable first quarter, wood flooring sales have been declining in recent months. Sales in the first six months of 2013 were 4% behind the same period in 2012.

- Finland: wood flooring consumption decreased by 3% in the first half of 2013 compared to the same period in 2012.

- France: wood flooring sales in the first half of 2013 were 10% less than the same period in 2012. French manufacturers blame weak consumer confidence and lack of political action to solve underlying economic issues such as declining competitiveness and high debt.

- Germany: wood flooring sales in the first half of 2013 were similar to the same period the previous year. Prospects are improving as the construction sector is now performing well. The number of building permits issued has been rising this year.

- Italy: after a poor year in 2012, wood flooring sales fell a further 11% in the first six months of 2013 compared to the same period in 2012. The Italian woodworking industries as a whole are going through an extremely difficult time, losing up to 25% of sales this year. Italian manufacturers are losing competitiveness, partly due to high taxes and labour costs. Imported products have also benefited from a more favourable EUR/USD exchange rate.

- The Netherlands: having fallen heavily in previous years, the wood flooring market has stabilised at a low level. Sales in the first half of 2013 were similar to the same period in 2012. The renovation market is now performing well but this has not yet led to a significant rebound in wood flooring demand.

- Norway: although construction of new buildings has weakened slightly this year, demand for wood flooring has been growing slowly this year. Sales in the first half of 2013 are estimated to have been 2% higher than the same period in 2012.

- Spain: there’s still no sign of any improvement in the Spanish market for wood flooring. Sales were down a further 10% in the first half of 2013 compared to the same period in 2012.

- Sweden: wood flooring sales were 3% down in the first six months of 2013 compared to the same period in 2012.

- Switzerland: wood flooring sales were slow in the first quarter of 2013, but recovered well in the spring. Sales for the first half of 2013 were 2% higher than the same period the previous year. However manufacturers claim the market is increasingly flooded by products “of dubious quality” which is undermining the image of real wood flooring.

Slow recovery forecast in the UK wood flooring sector

In the absence of a large domestic wood floor manufacturing sector, the UK is not represented at the FEP meetings. However it is a large consuming market for imported wood flooring. Insights into recent trends and future prospects in the market are provided in a new report by AMA Research entitled “Wood and Laminate Floorcoverings Market Report – UK 2013-2017 Analysis”.

According to the report, in 2012 the wood flooring sector (solid wood, engineered wood and laminates) accounted for 16% value share of the total UK floor coverings sector, estimated to be worth some £1.7 billion. At around £284 million in 2012, market value has risen marginally since the low of £281 million in 2011. However, market value last year was still 26% lower than the peak of £385 million achieved in 2007.

The report suggests that sales of wood laminates fell by 30% in value terms 2007-2011. However sales of laminates were still worth around £166 million in 2012 and accounted for 58% of the total UK wood flooring market. Wood laminates remain one of the most popular products in the DIY flooring sector.

In recent years, there has been a shift in focus from cut-price, bargain-basement laminated wood flooring products to higher-quality products. Sales of higher-margin and more desirable products have helped to offset some of the decline in DIY flooring sales in recent years. There are indications that the UK laminate market has now ‘stabilised’, with suppliers reporting a rise in sales during 2013 for the first time in many years.

In 2012, sales of solid and engineered wood floors in the UK were worth £104 million. Although still holding a smaller share of the overall UK market, these products have outperformed laminates in the UK in recent years. Solid and engineered wood flooring is more focused on the middle to upper sectors of the market which has been less volatile than the low end of the market. Sales of solid and engineered wood flooring declined 16% in the 2007 to 2011 period and the market returned to growth in 2012.

The report notes that imports dominate the UK wood floor coverings market, with the value of imports reaching a seven-year peak in 2010 before falling again 2011-12. China remains the key source country, accounting for over half (53%) of imports, in value terms, in 2012.

The contract sector accounts for around 44% of the market for wood floors in the UK. This sector has been less volatile than the domestic sector since the start of the recession. The contract sector recovered well in 2012 when it was estimated to be worth around £124 million. The domestic sector accounts for an estimated 56% value share of the total UK wood floors market and was worth £160 million in 2012.

Looking ahead, the total value of the UK wood flooring market is expected to rise by 1% in 2013 to reach £286 million. The market is forecast to experience 1-2% annual sales growth between 2013 and 2016 when value is expected to reach around £305 million. That is still 21% below the pre-recession peak of £385 million in 2007.

Growth in the domestic sector continues to be constrained by the slow pace of recovery in the housing sector. However demand should be positively influenced by government incentives aimed at stimulating home buying and housing output. Recovery for key commercial sectors is likely to be moderate, at best, in the short to medium term. Rising demand from commercial buyers will be offset, to some extent, by lower demand in the public sector.

European laminates producers report on new-season fashion trends

According to the Association of European Producers of Laminate Flooring (EPLF), manufacturers are preparing for the 2014 laminate flooring season with a range of creative decoration ideas. The wood look is still very dominant and there continues to be a strong fashion for longer and wider plank sizes.

Oak continues to dominate wood decors with its almost inexhaustible decorative potential. Yet floors with the appearance of delicately-grained ash or elm, or rich softwoods such as spruce and larch, are also rapidly gaining in popularity. In general, demand for decor that resembles elegant wood varieties is on the rise.

Dark colours have seen a slight decline, with the collections of European manufacturers instead presenting a varied spectrum of natural grey and beige tones – a trend that originated in the field of interior decor and which is now being adopted by the laminate flooring sector. A considerable amount of wood decor in the laminate sector no longer appears in its “natural” version, but rather with a discreet white or grey haze.

Laminate producers have also invested heavily in so-called “synchronisation technology” which matches surface structures with the relevant decor image. This allows production of rustic boards which not only look authentic but also feel like the real thing. Modern synchro-pore printing enables the authentic transfer of a wide variety of surface structures, from fine veins and pores to deep, distinctive knots.

Building on this technology, the rustic “used look” remains the key theme in European laminate flooring ranges. This appears in several varieties of commercial products, from construction timber styles with imitation cement traces, to laminate flooring that feels brushed, planed or freshly sanded. This rustic nature particularly comes into its own in the new rural-style wooden floorboard collections, which are increasingly being offered in longer and wider floorboard sizes.

European laminates industry emphasise premium quality in product promotion

Members of the EPLF are to being encouraged to use an assertive new slogan – ‘Quality and Innovation made in Europe’ – as a common foundation for their marketing efforts. The new slogan highlights the various core values that EPLF believes are inherent to European laminate flooring products. According to EPLF, these values are “certified quality, mature technology, excellent usage characteristics, eco-friendliness, and products that are pleasing to the eye and the touch – combined with ever new and creative designs”.

According to Volkmar Halbe, Chairman of the EPLF’s Market and Image Committee, “among wholesalers, the EPLF registered trademark has already established itself as a mark of quality in laminate flooring. The new slogan now conveys a clear statement of quality to the customer. The same quality implied by the label is what you’ll find inside the product. We are the world’s quality and technology leaders. That’s our USP. The new slogan enables EPLF members to communicate this pithily and effectively.”

The slogan is intended to identify the quality of EPLF members, especially in the growing export markets outside Europe. Volkmar Halbe says “in some foreign markets, especially China, more and more products are appearing that purport to satisfy load classes specified by the EN-13329 standard – but testing proves that this is not the case. Cheap imitations put the reputation of the whole laminate flooring industry at risk. We simply will not tolerate this. The EPLF is actively working to counter fake labelling. We hope that the new logo will help to support legal action taken by our members in cases of fake labelling by third parties.”

European laminates producers target Chinese flooring market

Much of the dialogue in the European wood flooring sector in recent years has focused on the rising tide of competition from Chinese manufacturers in their domestic markets. However, judging by recent reports from the EPLF, there is a growing focus on European manufacturers seeking to capture a larger share of the Chinese market.

Europe’s flooring manufacturers have recognised that their domestic markets are unlikely ever to recover the ground lost during the recession. Future opportunities for market development are now seen as heavily concentrated in other regions. China is seen as a particularly attractive target. US market research organisation Catalina Research estimate that total flooring sales throughout China amounted to 3.9 billion m2 in 2011 and forecast that demand for new floors will increase by 149 to 177 million m2 per year at least until 2025.

In addition to the growth of China’s overall market, European manufacturers reckon that there is significant potential for high-end laminated products to capture more market share. According to Catalina Research, in 2011 laminate flooring made up just 4% of China’s market (156 million m2), with solid wood and bamboo floors accounting for 4% (156 million m2). This compares to tiles, which represented a massive 75% (2.93 billion m2) of all flooring products sold in China in 2011, carpets with 9% (351 million m2), and elastic floors with 5% (195 million m2).

Several years ago laminate flooring began to be manufactured in China, causing the import market for European manufacturers to collapse. In 2012 China produced 28% of the world’s laminate flooring, moving into the top spot for the first time (with Germany accounting for 27%).

However, European manufacturers report that sales of their branded products in China also began to recover in 2012. Imports into China and Hong Kong of high-quality, specialist brand-name goods manufactured by European companies once again exceeded 3 million m², after having fallen to 2.3 million m2 in 2011. Several European manufacturers, such as Pergo, Skema and Unilin, are already active on the Chinese market, and they could soon be joined by other names.

European manufacturers believe the high-end segment of the Chinese market offers particular potential for European-made quality laminate flooring. European manufacturers are seeking to position themselves unambiguously in the premium segment, for example through widespread of their new slogan (see above).

EPLF believes there is a growing demand in China for genuine European-made flooring which is subject to strict EU norms, meeting very high standards of product quality, sustainability and eco-friendliness. According to Volkmar Halbe, Chairman of the EPLF’s Market and Image Committee, “because Chinese customers are increasingly demanding these qualities, Chinese manufacturers will quickly attempt to catch up. But the EPLF is convinced that European manufacturers, with their production expertise, are well positioned to maintain the lead over Chinese competitors”.

Particular efforts are being made to influence interior designers for commercial premises and affluent private clients in China. For example, according to Raffaele Ferrara of Italian manufacturer Skema, “interior designers are focusing on Western style and importing European tastes into the Chinese market. Grey and beige decors, in vogue in Europe for the past couple of years, are also doing very well in Chinese cities. In general, light and mid tones are very popular, while walnut and smoked oak are the dark decors of choice. Recently we have also seen a rise in demand for high-quality synchro-pore finishes. Formats are changing too: in addition to standard boards the Chinese market is slowly but steadily acquiring a taste for long board and tile formats.“

Tarkett publishes analysis of flooring market

It’s very rare for a large corporation makes public a very detailed analysis of its product markets, competitive position and plans for the future. However one of the world’s largest flooring manufacturers has done just that in preparation for filing of an initial public offering (IPO).

On 4 October, the French company Tarkett which is 50% owned by U.S. private equity firm KKR submitted a registration filing for an IPO on the Paris stock exchange that could value the company at as much as €2.5 billion euros ($3.41 billion).

The documents filed by Tarkett include an assessment of the size and prospects for the global flooring market. Tarkett is well placed to undertake such an analysis due to its participation in a wide range of market segments in several of the world’s largest consuming countries.

The Tarkett Group

Tarkett sells close to 500 million square meters of flooring each year, and operates 30 manufacturing sites around the world. In 2012, Tarkett generated net consolidated revenues of €2,319 million. Tarkett are the number three flooring company worldwide (based on 2012 sales). Tarkett claim to have the most diversified geographical footprint in the industry, selling into over 100 countries and with well-developed distribution networks in Europe, North America, CIS, China, and Brazil. The company’s main competitors focus their operations either in North America or Europe and generally concentrate on a more limited number of products.

Tarkett has 30 production sites worldwide, including 12 in Western Europe, 3 in Eastern Europe, 2 in Russia, 11 in North America, 1 in Brazil, and 1 in China. Production facilities are located as close as possible to consuming markets so as to minimize transport costs and customs duties and remain competitive with local players. Tarkett are the number one vinyl flooring company worldwide and the leading flooring company in Russia and more generally in the CIS, as well as in a number of major European countries, including France and Sweden. One site in Russia has more than 1000 employees and has the largest production capacity of vinyl flooring in the world.

Wood and laminate flooring accounts for 10% of Tarkett’s 2012 sales. These products are destined primarily for Europe and North American markets, mainly residential renovation projects and, to a lesser extent, commercial applications such as retail, hospitality, offices and indoor sports facilities. In line with broader industry trends, Tarkett has shifted from manufacturing plank to engineered multi-layer wood products.

Most of the wood used by Tarkett comes from Europe. Tarkett is currently restructuring their European wood business to improve efficiency and reduce costs, for example by transferring manufacturing capacity from Scandinavia to Ukraine, which is closer to the source of raw materials and offers lower labour and other costs.

Innovation is a key part of the company’s market development strategy. Recent innovations have focused on development of ecologically sustainable flooring solutions. In the wood flooring sector, a staining process is now used to adapt to demand in different markets and regions, in particular by offering flooring that resembles exotic wood. Going forward, Tarkett is looking to expand production of luxury vinyl tiles (LVT) in line with growing global demand for these products. The company is also planning to launch phthalate-free vinyl products, initially targeting the European market.

Assessment of the global flooring market

Tarkett’s review of the global flooring market is based on a number of sources, including studies and statistics from independent third parties (in particular Freedonia, the European Federation Parquet Industry Federation and the European Resilient Flooring Manufacturers’ Institute).

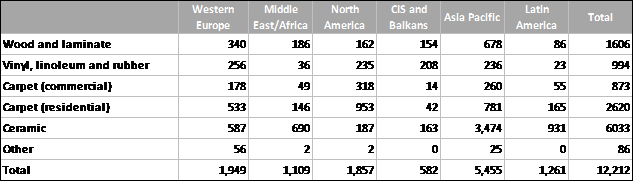

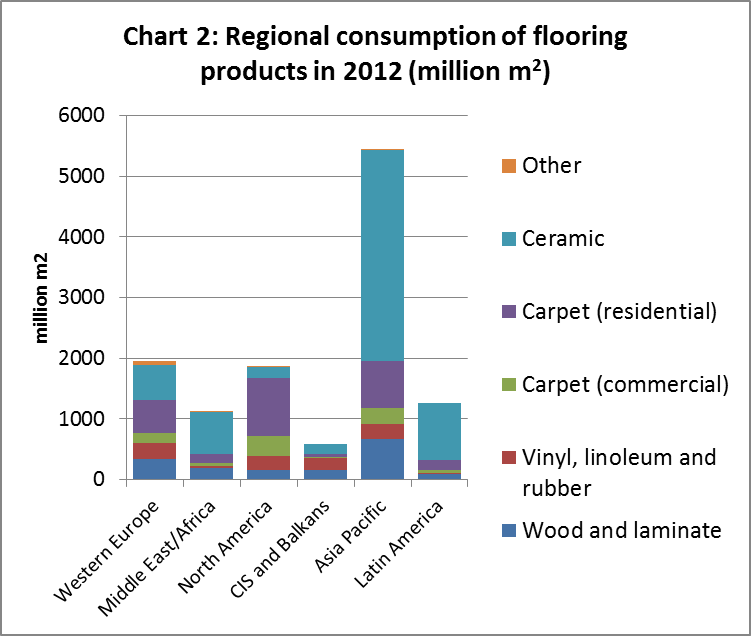

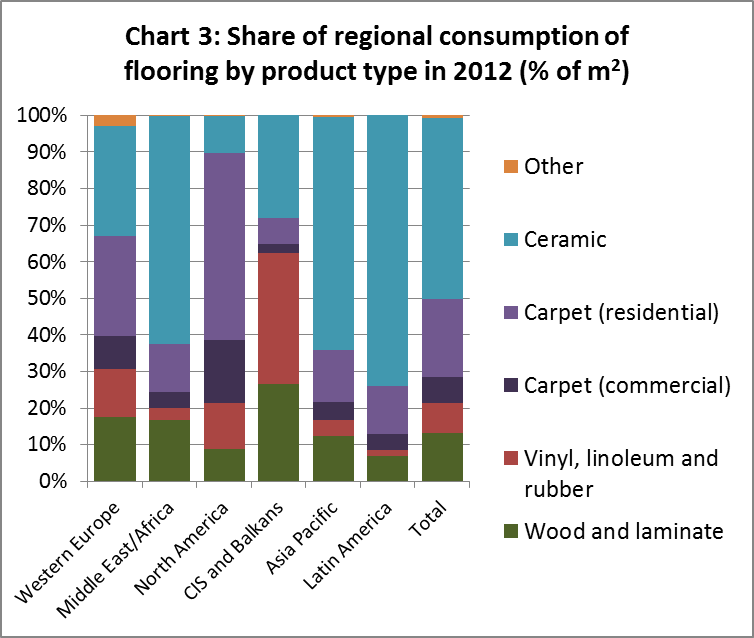

Tarkett estimate that approximately 12.2 billion square meters of flooring were sold globally in 2012, excluding sales of specialized products such as concrete, bamboo and metal flooring (Table 1, Charts 2 and 3).

Table 1: Regional consumption of flooring by product type in 2012 (million m2)

Wood flooring types accounted for only 13.2% of world sales in 2012, although share was closer to 20% in Europe and the Middle East. Nearly half of global flooring consumption in 2012 (49.4%) comprised ceramics. This is particularly due to the huge dominance of ceramic floors in Asia. Carpet accounted for 28.6% of wood flooring demand in 2012. Carpets are particularly dominant in North America where share is approaching 70%. Resilient flooring types (vinyl, linoleum and rubber) accounted for 8.1% of global flooring demand in 2012, with share rising as high as 35.7% in the CIS and Balkans.

Western European flooring sector

According to Tarkett, demand for flooring in Western Europe in 2012 was 1.95 billion square meters, representing 16.0% of global demand. Carpet was the leading flooring type in this region, accounting for 36.4% of demand, followed by ceramics (30.1%), wood and laminates (17.4%) and resilient floors (13.1%).

In Western Europe, demand for different categories of flooring products varies significantly from country to country, especially between Northern and Southern Europe. For example, carpet is frequently used in the UK, whereas wood floors are more popular in Scandinavian countries. Sales of wood and laminate flooring in Norway, Sweden and Finland represent, respectively, 60%, 40% and 48% of total flooring sales in those countries. Ceramic is a very popular product in Southern Europe, representing 52%, 51% and 66% of demand in Italy, Spain and Portugal, respectively. In Germany and France, the breakdown by product category is more balanced.

Recent flooring trends vary between European countries. In the UK, weak new build activity led to a decrease in flooring demand. This was only partly offset by an increase in do-it-yourself improvements and home renovations. The French flooring industry has suffered as a result of an uncertain economic environment. Flooring demand was less affected by the economic crisis in Scandinavia and Germany, although there was a decrease in sales of wood and laminate flooring in a highly competitive environment.

Tarkett believe that overall flooring demand in Western Europe is currently stable, despite an economic context that continues to be uncertain. Looking forward, Tarkett forecast that, after a steep decline in recent years, total demand for wooden and laminate floors in Europe will decline more slowly at around 1% per year between 2012 and 2016. Demand for wooden floors may increase slightly in the UK and in parts of Scandinavia. However demand for wooden floors is expected to decrease slightly in France and Germany. Sales volumes of laminate flooring are also likely to continue to decline slowly in Western Europe during this period.

Tarkett estimate that total Western European demand for resilient floors will rise by 1% per year between 2012 and 2016. Much of the growth in this segment should be driven by the commercial market, in particular in Germany and the UK. Total demand for carpets is expected to remain stable in Western Europe between 2012 and 2016.

Tarkett’s own operations in Europe focus on vinyl resilient flooring, wood flooring and laminate flooring. Most of Tarkett’s sales of resilient flooring are in France, Germany and the UK, while the majority of their wood and laminate flooring sales are in Scandinavia. Tarkett are the number one vinyl flooring company in Europe and the leading flooring company overall in France and Sweden. Tarkett is also the third manufacturer of wood and linoleum flooring in Western Europe. Tarkett estimate that they sell between 25% and 30% of all vinyl flooring products sold in Europe. However Tarkett account for less than 5% of laminate flooring sales in most countries.

Tarkett’s main competitors in the region are other European groups, which generally concentrate their businesses on a limited number of countries and products. The most important competitors in this region are Forbo (resilient flooring), Gerflor (resilient flooring), Kahrs-Karelia Upofloor (wood flooring), Beauflor (resilient flooring), James Halstead (resilient flooring) and Bauwerk-Boen (wood flooring). The American groups Mohawk (Unilin/Marazzi) and Armstrong Flooring (DLW) are present in Europe, but with relatively modest business volumes compared with their presence in North America. Tarkett faces smaller local competitors in some markets although economies of scale for the most complex products tend to limit the role of these companies.

Flooring demand in North America

Tarkett estimate that in 2012, demand for flooring in North America was 1.9 billion square meters. That is 15.2% of global demand for flooring products. Demand in North America is dominated by carpet, which represented 68.4% of total volumes sold in 2012. 8.7% of total flooring sales were wood and laminate products and 12.7% were resilient flooring.

Between 2006 and 2011, North American demand for flooring fell, mainly due to the decrease in new construction during the financial crises. However, the U.S. construction market grew in the fourth quarter of 2012 and continued to improve in 2013, due primarily to the residential market. As the U.S. economy recovers, Tarkett forecast strong growth in North American demand for all flooring product types at a rate of 5-6% per year between 2012 and 2016.

Tarkett’s flooring sales in North America are divided fairly evenly among commercial carpet, resilient, rubber flooring, and vinyl and rubber accessories, with wood and laminate flooring accounting for a smaller portion of sales. In this region, Tarkett are the second largest resilient flooring company and the second largest rubber flooring company. Tarkett estimate that their products account for approximately 18% of resilient flooring sold in North America. Following the 2012 acquisition of Tandus, Tarkett are also the fourth largest commercial carpet company in North America. Tarkett’s Johnsonite products occupy a leadership position in the vinyl accessories market.

Main competitors on the U.S. market are Mohawk, Shaw Floors, Armstrong Flooring, Interface and Mannington, which generally concentrate a large majority of their sales in North America. In keeping with the strong North American preference for carpet, this product category represents a significant share of these companies’ sales (this is particularly the case for Mohawk, Shaw and Interface). However, some of these companies, including Mohawk, Armstrong and Mannington, also market resilient flooring, as well as wood and laminate flooring. Competitors for Tarkett’s Johnsonite products include Nora, a rubber flooring manufacturer, as well as local manufacturers.

CIS and the Balkans

In 2012, the demand for flooring in Russia, the other CIS countries and the Balkans (the former Yugoslavia) was 582 million square meters, representing 4.8% of global flooring demand. In these countries, resilient flooring is most popular, representing 35.8% of total flooring demand. Other than resilient flooring, the main products sold are ceramic tiles (28.0% of total flooring demand), wood and laminate flooring (approximately 26.5%) and carpet (9.6%).

Unlike Western Europe and North America, resilient flooring is used primarily by the residential market in the CIS countries. This difference can be explained by the history and climate of these countries. Most of the residents of these countries became the owners of their homes following the dissolution of the Soviet Union. For these new homeowners, renovation is a high priority, and resilient flooring is both well-suited to local tastes and attractive for household budgets.

Due to economic growth in CIS countries, renovation demand in the region has grown significantly in recent years. This trend is expected to continue. The Russian statistics agency Rosstat estimates that, out of the three billion square meters currently installed in Russian residential housing stock, approximately two billion square meters require renovation.

The commercial market in the CIS region has been slower to develop, but shows strong growth potential. Commercial end-users initially chose residential resilient flooring for their first renovation projects. These floors are not well-adapted to high-traffic commercial premises. Moreover, Russia has adopted stringent fire regulations for commercial products. As a result of these factors, the resilient flooring market has shown moderate growth in recent years, although its size remains modest compared to the residential market. Tarkett forecast that total demand for resilient flooring in the region will increase by 47% per year between 2012 and 2016.

Over the last several years Russians have begun to buy laminate floors in order to give the appearance of wood floors while remaining within a reasonable budget. Tarkett forecast that total demand for laminate flooring in the region will increase by 7% per year between 2012 and 2016.

Tarkett has been doing business for more than 20 years in the CIS and the Balkans, primarily in Russia, Serbia, Ukraine and Kazakhstan. As a result of their long-standing presence in this geographic region, they consider themselves a “local” company and a market leader. Tarkett are the number one resilient flooring company in Russia, Ukraine, Kazakhstan, Serbia and Belarus, and the number one wood flooring company in the CIS.

Tarkett’s market leadership in the Russian resilient flooring market is the result of the company’s well-known brands, local production, well-developed distribution platforms and deep understanding of local tastes. In the resilient flooring sector, Komiteks and Juteks/Beaulieu, two local companies, are the other leading companies in this region, alongside the international suppliers IVC and Forbo.

In the laminate flooring market, Chinese manufacturers occupy a leading position due to their ability to offer low-cost entry-level products. The other principal companies in this market are Kronostar, Kronospan, Classen and Unilin. Tarkett are not as strong in laminate flooring as in resilient flooring. Tarkett are currently the number four laminate flooring company in Russia.

Asia-Pacific Region

Tarkett estimate that in 2012, demand for flooring in the Asia Pacific region reached 5,455 million square meters, representing 44.7% of global flooring demand. Ceramic is the most frequently used material in Asia Pacific, as a result of local climate, ease of manufacture and the multiplicity of local suppliers.

Tarkett note that, given the size of its residential housing stock, China is, by volume, the largest in the world. Drawing on a market study conducted in collaboration with a consulting firm, Tarkett believe that government initiatives in China will continue to sustain the construction market. Tarkett also forecast that aging of the Chinese population will fuel growth in the retirement home sector, in addition to projected growth from the healthcare and education markets. Vinyl flooring’s market penetration is still limited, but this product category may grow in the future.

For the period 2012 to 2016, Tarkett forecast 6% annual demand growth for resilient flooring, and 4% for carpets and wood and laminate flooring in the Asia Pacific region.

Tarkett’s position in this region is still in a development phase. The company sells primarily vinyl flooring to commercial users in Australia and China. Tarkett recently strengthened their presence in China by acquiring a primary distributor there. Tarkett also gained a commercial carpet production site in China with the acquisition of Tandus. Main competitors in Asia Pacific for vinyl flooring are Armstrong, Gerflor, LG and Forbo, as well as local Chinese manufacturers.

Latin America

In 2012, demand for flooring in Latin America reached 1,261 million square meters, representing 10.3% of global flooring demand. Ceramic is the most frequently used material in Latin America. Tarkett believe that flooring demand in the region is likely to grow. In Brazil, in addition to structural factors, the economy could benefit significantly from the 2016 Olympic Games and from the 2014 Soccer World Cup. In this region, sales of luxury vinyl tiles continue to grow at a faster pace than the general flooring market.

In Latin America, Tarkett does business principally in Brazil, where most of sales are vinyl products for commercial end-users. Tarkett’s position in Latin America was strengthened in 2009 with the acquisition of Fademac, a Brazilian vinyl-flooring manufacturer. Main competitors in vinyl flooring in Latin America are Gerflor and Forbo.

PDF of this article:

Copyright ITTO 2020 – All rights reserved