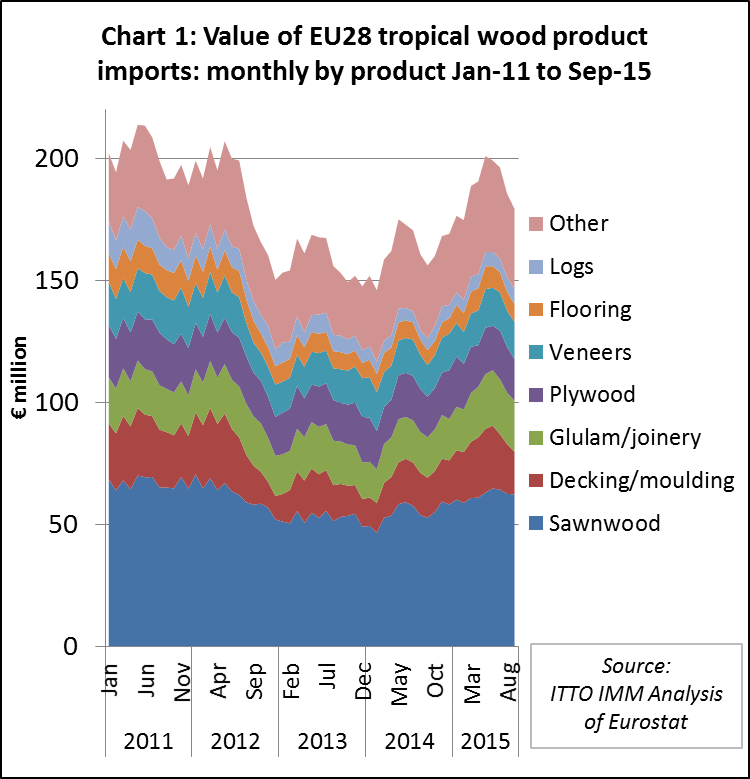

EU imports of tropical timber products increased sharply between September 2014 and April 2015 but slowed again in the four months to end September 2015 (Chart 1). Nevertheless, the value of EU imports of tropical timber across all product groups in the first 9 months of 2015 was, at €1.703 billion, 16% greater than the same period the previous year. So far EU imports of tropical timber in 2015 have been close to levels last seen in 2012.

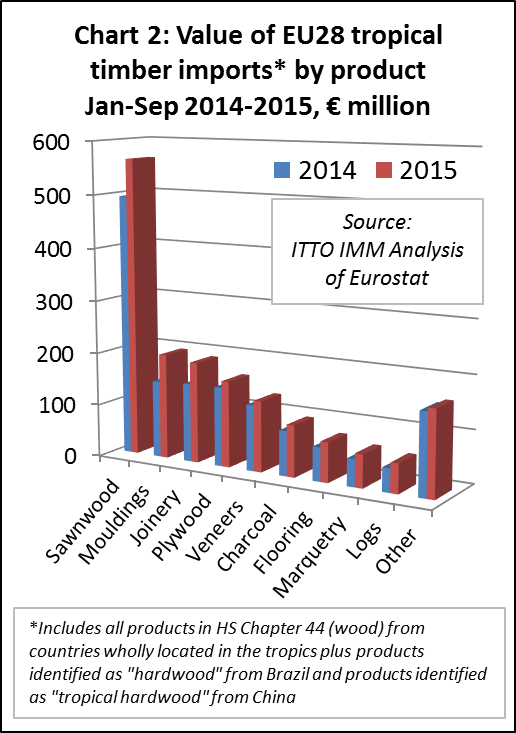

EU imports of all tropical wood products have increased this year. With the exception of plywood (+8.6%), veneers (+7.5%) and “other” (+4.3%), all tropical product groups showed double-digit import growth. Mouldings (+36.4%) and joinery (+28.2%) experienced the highest growth rates. Imports of sawnwood, the most important tropical product group in terms of import value, rose by 14.2% to €565.1 million. Imports of tropical logs (+24.1%) have also continued their upward trend this year after several years of steep decline (Chart 2).

Some of the increase in the euro value of tropical wood imports is due to the relative weakness of the European currency this year which has led to price inflation for European importers. However, this has been partly offset by producers lowering their sales prices and by a steep fall in freight rates as the year progressed. Further analysis of the data also shows that the quantity of EU tropical wood imports has increased across nearly all product groups.

Increased imports into all major EU markets

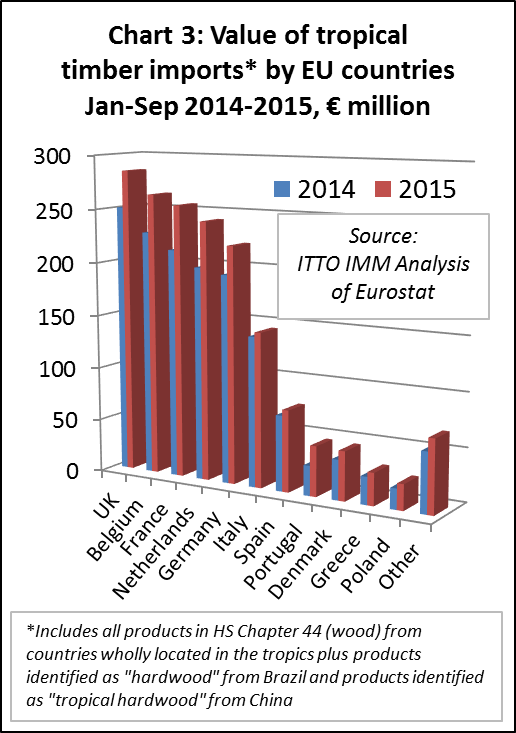

A closer look at the individual EU countries reveals that tropical timber deliveries to all important markets have increased this year, in most instances by a significant margin. Spain (+7.9% to €76.2 million) and Italy (+3.1% to €144.4 million) were the only major markets to show single-figure growth rates (Chart 3).

The UK has remained the most important tropical timber market in Europe this year, with growth of 13.7% in imports to €285.1 million across all product groups during the first nine months. There was also substantial growth in imports into Belgium (+15.6% to €263.9 million), France (+19.4% to €255.1 million), and the Netherlands (+21.3% to €241.9 million).

Deliveries of tropical wood to the German market increased 13.8% to €221.1 million in the first nine months of 2015. However, reports from German importers are slightly less positive. While some importers specialising in African timber report satisfactory business this year, those focused on Asian timber describe the market as difficult. The same is true for tropical plywood from South-East Asia, which is under intense competitive pressure from European and Russian poplar and birch products.

The German timber trade federation GD Holz reports that wood product sales in Germany have more or less stagnated in the first nine months of this year. Moreover, garden wood assortments, including decking, experienced decline by around 5%. The same is true for sawn timber. For building products and joinery, on the other hand, GD Holz reports growth of around 5%.

Sharp increase in EU sawn imports from Malaysia and Brazil

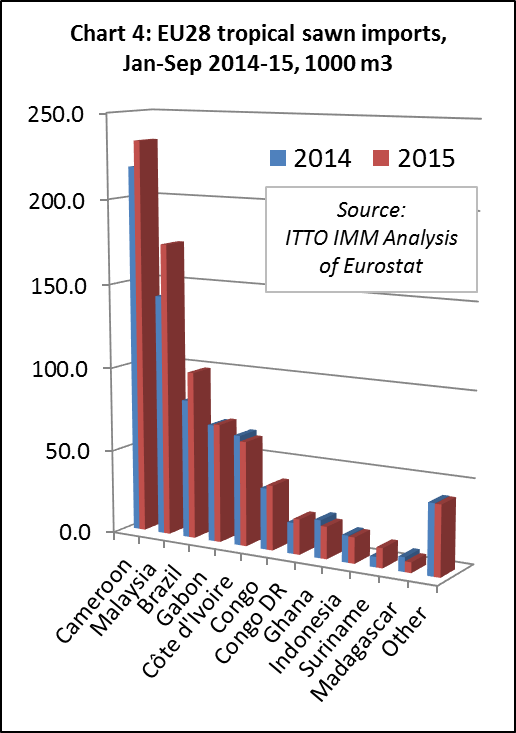

EU imports of tropical sawn timber increased by 9% to 793,100 m3 in the first nine months of 2015. Imports from Cameroon, the largest supplier, increased 7% to 233,000 m3. Import growth was even more rapid from Malaysia (+22% to 173,800m3), Brazil (+21% to 99,500m3), and the Democratic Republic of the Congo (+14% to 21,000m3).

Imports from Gabon (+1% to 70,400m3) and Congo (+6% to 38,500m3) recorded below-average growth rates. Meanwhile, imports from Ghana (-15% to 19,100m3) and Ivory Coast (-5% to 62,200m3) have declined this year (Chart 4).

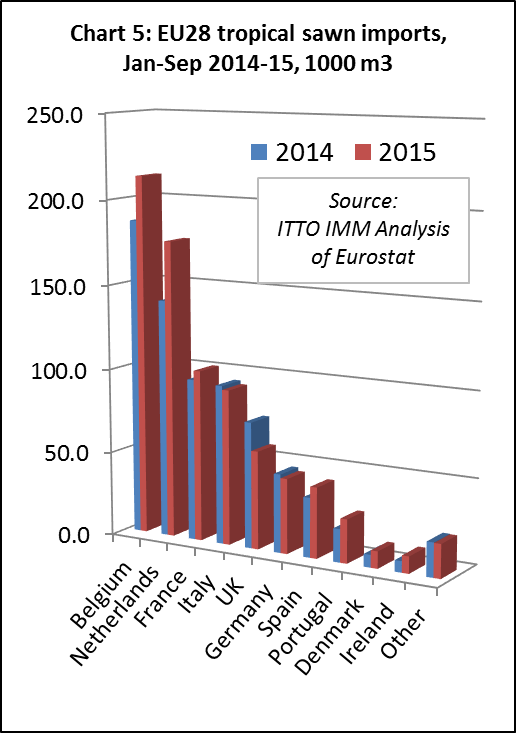

Market recovery in Benelux and France

The rise in tropical sawn wood deliveries to Europe was primarily due to higher imports into the Netherlands (+25% to 176,100m3), Belgium (+14% to 213,300m3) and, to a lesser extent, France (+6% to 101,400m3). By contrast, imports into the UK, which increased sharply in 2014, declined 22% to 58,100m3 in the first nine months of 2015. Tropical sawn wood imports into Germany (-5% to 44,400m3) and Italy (-2% to 92,000m3) have also declined this year (Chart 5).

In their latest statistical report (cover the first 8 months of 2015), the UK Timber Trade Federation (TTF) reports “all regions of the world except Central and South America have exported less to the UK in 2015 to date. Only a tripling of volumes from Guyana (from a relatively low base) has provided regional growth in 2015”. Hardwood deliveries to the UK from Asia declined 17% while imports from Africa were down 28% in the first 8 months of 2015. Despite the sharp uptick in imports from Guyana, UK hardwood imports from South and Central America were no more than 8,000m3 in the first 8 months of 2015.

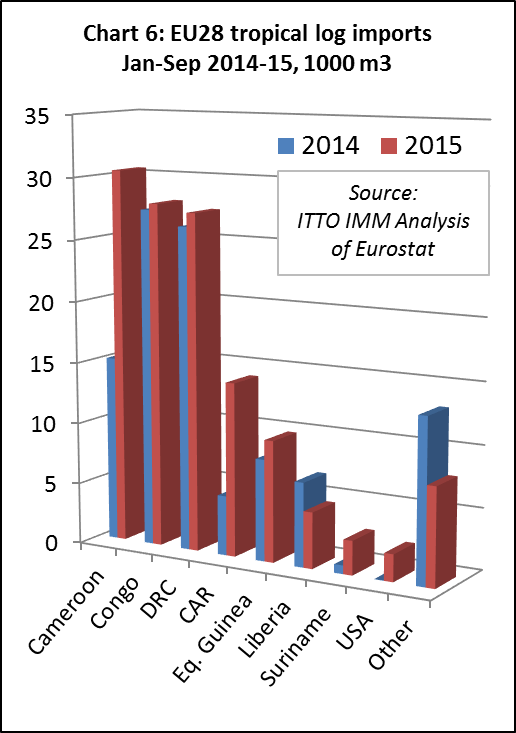

Tropical log imports up 24%

Following nearly a decade of continuous decline, EU imports of tropical logs have recovered a little ground this year. Imports increased 24% to 127,338m3 in the first nine months of 2015. Much of this import growth was concentrated in the first five months and the pace of imports slowed between June and September. EU tropical log imports from Cameroon doubled to 30,464m3 and deliveries from the Central African Republic almost tripled to 14,122m3 in the first nine months of 2015. Imports from Suriname also tripled from a low base to 2,776m3. However imports from Liberia declined 33% to 4,570m3 (Chart 6).

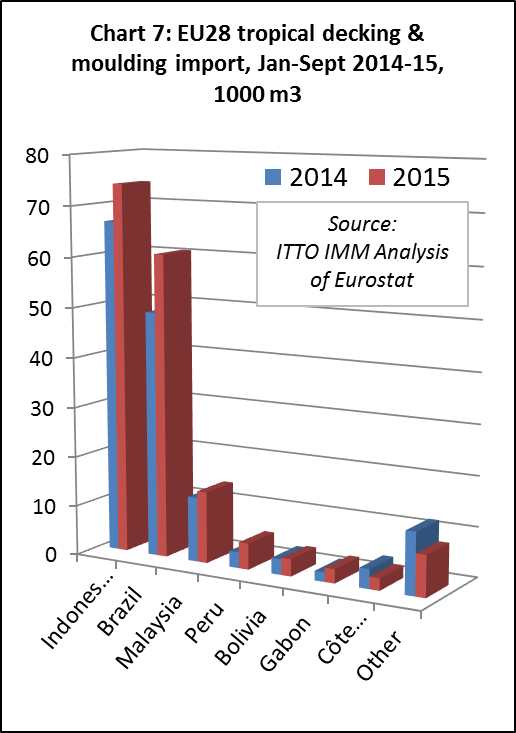

Rising EU decking imports from Indonesia, Brazil and Malaysia

EU imports of tropical mouldings (which includes both interior mouldings and exterior decking products) were 171,218 m3 in the first nine months of 2015, 12% more than the same period in 2014. Imports increased from all the major supply countries including Indonesia (+10% to 74,059m3), Brazil (+24% to 60,672m3) and Malaysia (+10% to 14,307m3). Deliveries from several other countries, including Peru, Bolivia and Gabon, also increased from a low base. However imports from Ivory Coast were much lower than last year (Chart 7).

Forecast of slow economic recovery

The EU continues to recover only gradually from the financial and economic crisis. The European Commission’s Autumn Economic forecast, published on 5 November, notes that the economic recovery in the EU is now in its third year and that “it should continue at a modest pace next year despite more challenging conditions in the global economy”. The European economy continues to benefit from low oil prices, accommodative monetary policy and the relatively weak external value of the euro, which is helping boost competitiveness, according to the EC.

Looking forward, the EC forecasts GDP growth to rise from 1.9% this year to 2.0% in 2016 and 2.1% in 2017. In making this assessment, the EC comments that “the impact of the positive factors is fading, while new challenges are appearing, such as the slowdown in emerging market economies and global trade, and persisting geopolitical tensions. Backed by other factors, such as better employment performance supporting real disposable income, easier credit conditions, progress in financial deleveraging and higher investment, the pace of growth is expected to resist the challenges in 2016 and 2017. In some countries, the positive impact of structural reforms will also contribute to supporting growth further”.

Recent reports from IFU, an economic research institute based in Germany, are slightly less optimistic. IFU’s index for the economic climate in the euro area dropped by two percentage points in the fourth quarter of 2015. IFU note that “while assessments of the current economic situation brightened slightly, the six-month economic outlook continued to cloud over. The euro area economy continued its recovery at a subdued pace”.

Regarding the current economic situation, experts surveyed by IFO in Greece, Finland, France, Italy, Spain, Austria, Portugal, and Cyprus continued to assess the situation negatively. In most other euro countries the situation was described as satisfactory. IFU’s six-month economic outlook remains positive overall but was scaled back in several countries, especially in France, Spain and Portugal.

PDF of this article:

Copyright ITTO 2020 – All rights reserved