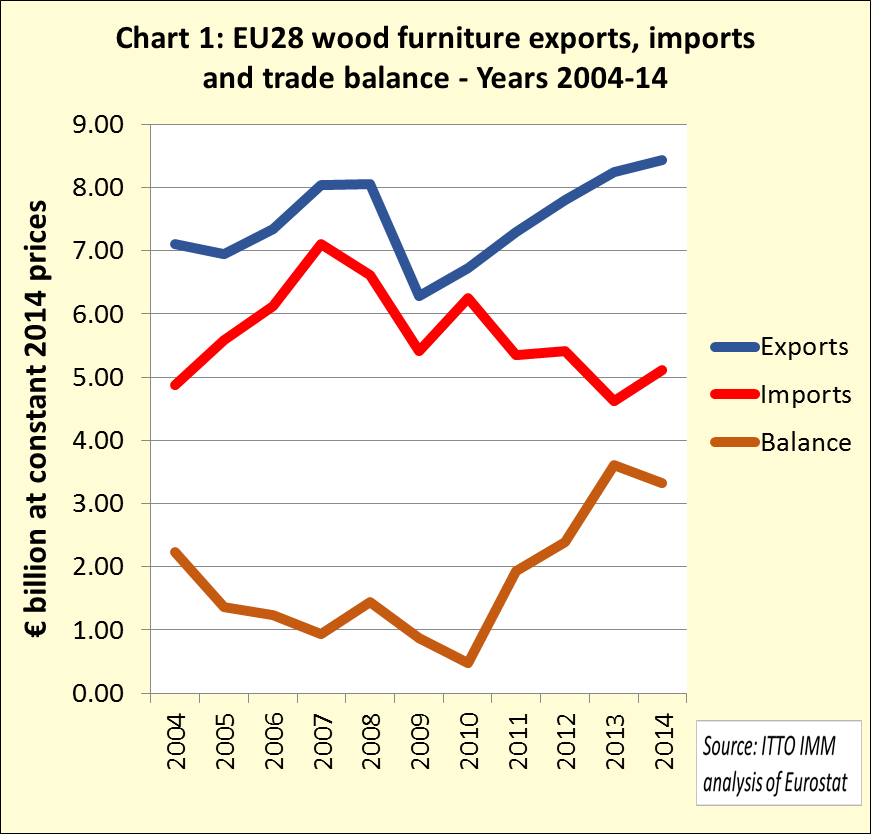

The sharp rise in the EU trade surplus in wood furniture between 2010 and 2013 came to a halt last year as the pace of increase in EU exports slowed while there was an upturn in imports (Chart 1). EU28 wood furniture exports were valued at €8.43 billion in 2014, 2.3% more than in 2013. EU28 imports of wood furniture were valued at €5.11 billion in 2014, 10.4% greater than the previous year.

The EU28’s trade surplus in wood furniture fell 8.2% from €3.62 billion in 2013 to €3.32 billion in 2014. Nevertheless, the trade surplus remains very high compared to the boom years prior to the financial crises when European manufacturers were focusing most of their attention on domestic sales and external suppliers, notably in China, were making significant inroads into the market.

These figures should be put into perspective. EU external trade in wood furniture is relatively small compared to total consumption, which is about €50 billion per year. There is much reliance on domestic manufacturers. Only about one quarter of wood furniture consumed in EU countries ever crosses a national boundary. Total internal trade in wood furniture between EU countries has averaged around €15 billion per year since 2009.

Wood furniture exports

While external trade forms only a small part of the EU furniture sector, it is becoming much more relevant to European furniture manufacturers. During the recession, manufacturers have become more focused on improving competitiveness relative to manufacturers in other countries, particularly China. With consumption static in domestic markets, European furniture companies are seeking to increase sales in other parts of the world.

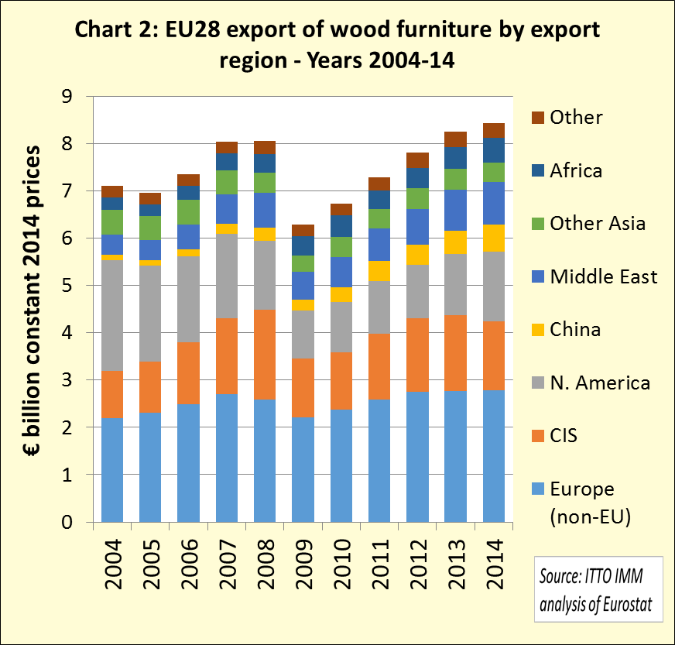

This more outward looking strategy has led to a consistent rise in EU wood furniture exports in the last five years (Chart 2). In 2014, EU28 export value increased to North America (+15% to €1.48 billion), China (+17% to €570 million), the Middle East (+3% to €900 million), and Africa (+11% to €520 million). These gains during 2014 offset a 9% decline in exports to the CIS region to €1.46 billion. Falling exports to the CIS are due mainly to slowing sales in Russia following economic sanctions in response to the Ukraine conflict and declining international prices for Russian oil and gas.

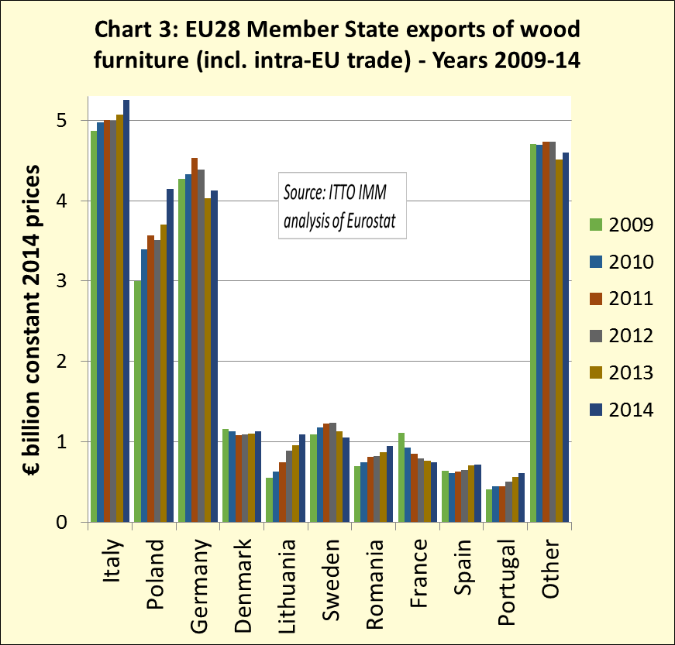

The rise in EU exports of wood furniture is being led by manufacturers in Italy, Poland and Germany (Chart 3). Preliminary data for 2014 indicates that exports of wood furniture (including intra-EU trade) increased from Italy (+4% to €5.25 billion), Poland (+12% to €4.14 billion) and Germany (+2% to €4.12 billion). Last year, Poland overtook Germany to become Europe’s second largest exporter of wood furniture. Wood furniture exports have also been rising rapidly from Lithuania, Romania, Spain and Portugal in the last five years. However exports from Sweden and France have declined while exports from Denmark have been stable (Chart 3).

EU wood furniture imports

After falling 14% in 2013, the value of EU wood furniture imports rebounded by 10% in 2014 to reach €5.12 billion (Chart 4). Imports from China fell 16% in 2013 but recovered by 14% to €2.81 billion in 2014. EU imports from the rest of the world also rebounded in 2014, increasing 8% to €2.3 billion after a 13% decline in 2013.

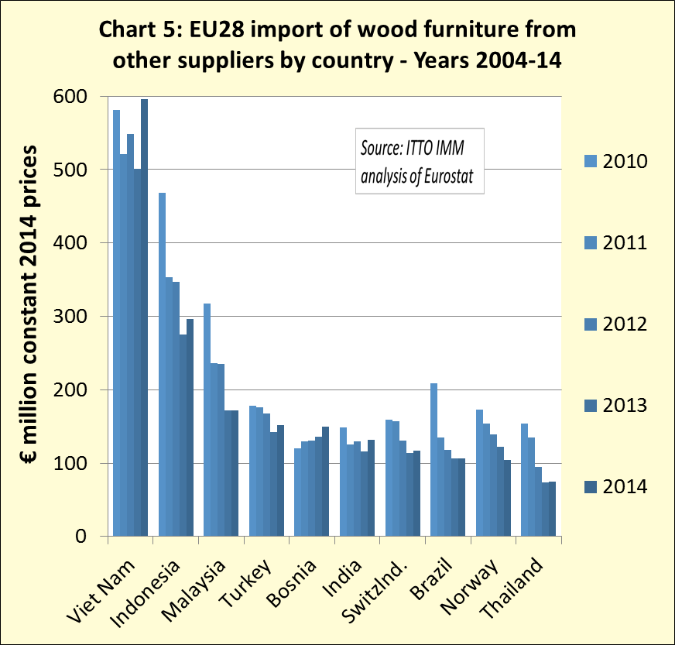

EU imports of wood furniture from Vietnam increased strongly last year, rising 19% to €596 million. This followed a 9% decline in 2013. After several years of declining sales, Indonesian wood furniture recovered a little ground in the EU market in 2014, with imports rising 7% to €296 million. There was also a 13% rise in imports from India to €132 million. Imports from Malaysia and Brazil remained stable between 2013 and 2014 at €172 million and €106 million respectively (Chart 5).

Analysis of economic indicators in Europe does not provide an obvious explanation for the sharp fall in EU wood furniture imports in 2013 and rebound in 2014. Throughout this period there was slow growth and flat consumer spending in the EU. Also exchange rates did not change significantly.

However demand in the UK, which is the largest European importer of wood furniture accounting for nearly one third of all imports from outside the EU, was recovering more strongly in 2014. There was also a particularly sharp increase in wood furniture import penetration into Germany, France, Italy and Sweden last year.

The EU wood furniture import trend in the last two years may have been affected by supply side issues. Some new wood furniture manufacturing capacity has come on-stream in Eastern Europe – notably in Poland, Lithuania and Romania– and this may have depressed EU imports from other regions in 2013. In 2014, slowing in China’s domestic market may have re-energised efforts by Chinese and other Asian manufacturers to increase sales in Europe.

Another factor is introduction of the EUTR in March 2013 which may have briefly disrupted EU imports of wood furniture as retailers struggled to obtain necessary assurances of legal wood origin from their overseas suppliers. If so, the rebound in 2014 may be a sign that overseas suppliers have been able to satisfy these new regulatory demands.

CSIL report consistent rise in global furniture trade to $128 billion

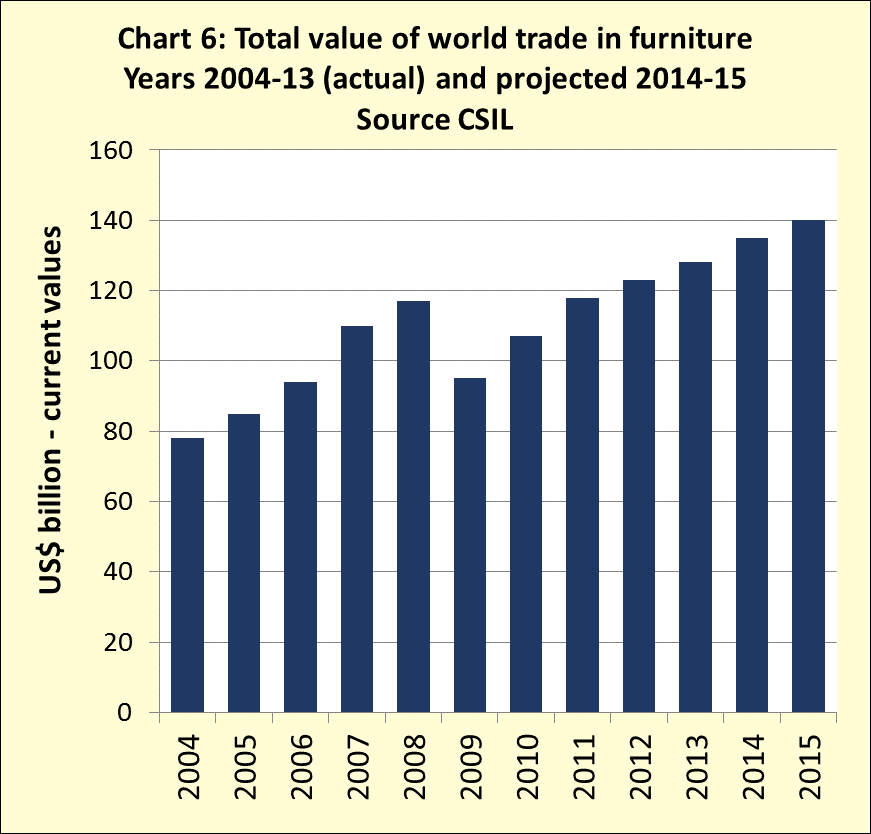

The latest edition of World Furniture (www.worldfurnitureonline.com), the quarterly journal of the Italy-based furniture industry research association CSIL, includes a wide ranging review of recent developments in the international furniture sector. The CSIL analysis of world furniture trade, which draws on data from the world’s 70 largest economies, indicates that total trade value was US$128 billion in 2013, around 1% of all global trade in manufactured products. The leading furniture importers during the year were the United States, Germany, France, the UK and Canada.

The annual trend in global furniture trade reported by CSIL is shown in Chart 6. In the period 2004 to 2008, global trade was rising driven primarily by imports into the United States, with smaller increases into the United Kingdom, France, Germany and Canada. Trade declined during the financial crises in 2009, but there was uninterrupted growth in the 2010 to 2013 period. This was driven mainly by recovery in North America and growth in emerging markets. The European market remained relatively weak during this period, although there was some growth in imports into Germany and the UK.

CSIL estimates that growth in global trade continued into 2014 and project a further increase to close to $140 billion in 2015. Import penetration for furniture (measured as the ratio between imports and consumption) is presently about 30% on a world scale.

According to CSIL, the main furniture exporting countries in 2013 were China, Italy, Germany, Poland and the United States. The relative positions of the main exporting countries changed considerably between 2004 and 2013. China has become the world’s leading exporter, overtaking Italy which is currently in second position. Between 2004 and 2013 China increased share of global furniture trade from 14% to 38%. Another major change is the rapid emergence of Vietnam, which jumped from 15th to 6th position in the period 2004 to 2013.

CSIL highlight that a significant proportion of furniture trade is more accurately described as “intra-regional” rather than truly “international”. This is particularly true of Europe. In the EU plus Norway, Switzerland and Iceland, 76% of trade takes place between countries within the region and only 24% is with countries in other parts of the world. In the NAFTA area (USA, Canada and Mexico), about 27% of foreign furniture trade is within the three countries and 73% is with countries outside the region. In the Asia and Pacific region, about 39% of furniture trade is within the region.

Western European furniture market recovers slowly

The latest edition of World Furniture also provides CSIL’s update on recent trends in furniture consumption and production in Western Europe. CSIL note that the region’s furniture sector has faced significant difficulties in recent years but is now slowly recovering.

CSIL estimate that total Western European furniture market value was €71 billion at producer prices in 2013, a slight downturn compared to the previous year and below pre-crises levels. However the market remains globally significant, accounting for one quarter of the value of world furniture consumption, 40% of world furniture import value and 30% of world furniture export value. CSIL estimate that the market grew by 0.5% in 2014 and project 1% growth in 2015.

CSIL identify the dominant markets in Western Europe as Germany, France, the UK and Italy. These four countries together account for two thirds of total furniture demand in the region. Market performances have varied widely between countries. While several markets including Spain, Italy and France, are still well below pre-recession levels, others are performing well including Norway, Switzerland and Sweden.

CSIL identify the following factors as major causes of recent weak demand in Western Europe: decreasing household disposable income; reduced consumer purchasing power; the slowdown of residential construction; economic uncertainty; and overall negative perception and expectations of European consumers.

The role of imports has also generally increased in all Western European markets according to CSIL. This is due both to rising levels of trade with countries in Eastern Europe (notably Poland) and with Asia. In total, around 50% of furniture consumed in Western European countries is imported. The leading Western European importers are Germany, France and the UK. Imports into Germany have increased particularly rapidly and now account for 25% of total western European furniture imports.

Western European furniture production stabilises at 15-20% below pre-crises level

In recent years, Western European furniture production has stabilised at around 15% to 20% of pre-crises levels. CSIL estimate that western European furniture production had a total value of €63 billion in 2013, around 18% of world furniture production. This compares to the Asia-Pacific region, which accounted for 57% of world production in 2013, and North America which accounted for 13%.

In 2013, Germany and Italy accounted for 50% of total Western European furniture production. An additional 27% of production was in France, the UK and Spain. Another 10% of production derived from Scandinavian countries (Sweden, Denmark. Norway and Finland).

The global competitiveness of Western European manufacturers has suffered from high labour and other costs of production. Fragmentation is another problem – there are an estimated 81,000 producers in Western Europe.

Nevertheless, CSIL report that Western European manufacturers remain dominant in their home markets. As a whole, around 55% of furniture produced in Western Europe is consumed in the domestic market. Of that which is exported, nearly 80% is traded with other European countries. Of the remainder: 8% is exported to the Middle East and Africa (up from 4% in 2003); 6% is exported to Asia (up from 4% in 2003); 6% is exported to North America (down from 10% in 2003); and 1% is exported to Central and South America (unchanged in the last decade).

Structural changes in Western European furniture sector

Weak demand and technological developments are driving major structural changes in the Western European furniture market. There has been an increase in the level of concentration in the retailing sector. According to CSIL estimates, the top 15 furniture retailing companies accounted for 25% of the Western European market in 2012 compared to 21% in 2010. This has been driven partly by closures and acquisitions, and partly by growth in market share of the larger furniture chains.

More furniture retailers in Europe are now operating in more than one country. About 20% of leading furniture retailers sampled by CSIL were operating in other countries.

In all European countries there has also been a sharp increase in the volume of furniture distributed by larger specialist furniture retail groups. Large specialist furniture retailers accounted for 61% of furniture sales in Western Europe in 2013 compared to only 41% of 2003.

However CSIL’s data shows that the share of smaller independent retailers in the western European furniture market has decreased from 31% in 2003 to 22% in 2013. The decline has occurred in nearly all Western European countries, the only exceptions being Austria and The Netherlands.

A larger proportion of furniture sales in Western Europe now consist of low cost items offered by larger distributors. There is also an increasing trend towards online sales with consumers taking more time to compare prices. Overall the combination of company promotions and discounts and a shift to lower cost alternative products has led to a significant decline in the average purchase price of individual furniture items.

This in turn is feeding through into declining per capita expenditure on furniture in almost all western European countries. CSIL estimate that European per-capita expenditure on furniture fell from €321 in 2008 to €262 in 2013.

While smaller independent retailers are suffering from these trends, many leading European retailers have performed well in recent years. CSIL analysis of the financial reports of leading furniture retailers in Western Europe indicated that sales by these larger companies increased by 5% on average in the 2010 to 2012 period.

“State of health” of European furniture industry

In 2014, CSIL surveyed the financial reports of around 1500 European furniture manufacturing companies to assess the “state of health” of the industry. In total, the surveyed companies employed around 375,000 people and had turnover of €58 billion in 2013, 70% of total European furniture production.

Total turnover of the 1500 companies declined by 10% between 2008 and 2009 during the financial crises. Since then the performance of companies has been mixed. By 2013, the turnover of around two thirds of companies was higher than it had been in 2009. However one third of companies still had a turnover below the 2009 level in 2013. In Spain and in Italy, almost 60% of companies in the CSIL sample had turnover below the level of 2009 in 2013.

The average added value across the 1500 surveyed companies was 24% of turnover in 2013. The rate of increase in added value is even lower than the rate of increase in sales. CSIL suggest this is because European furniture companies are becoming less reliant on in-house manufacturing and instead are purchasing more components or sub-contracting activities. Increased competition has also contributed to lower furniture retail prices and reduced margins.

CSIL note that overall profit margins amongst surveyed companies were generally higher in Eastern Europe than in Western Europe. Profit margins have been particularly low in France in the last two years. In 2013, Eastern European manufacturing companies accounted for 28 of the 50 fastest growing furniture manufacturers in Europe, up from only 17 of the top 50 in 2012.

IKEA group continues to increase global share

Globally, the Ikea Group’s sales were €29 billion in the 2014 financial year (12 months to 31 August 2014). Net income was €3.3 billion ($3.8 billion), the same as the previous year. However the Group reported a rising share of furniture sales in almost all markets. This was partly driven by price reductions which averaged 1% across the entire product range. This led to a 0.4% reduction in gross margin to 42.9%.

The Ikea Group is the world’s largest furniture retailing company, owning 315 outlets in 27 countries as of 31 August 2014. The Group reported that store visits increased by 4.7% to 716 million during the 2014 financial year while visits to its website grew by 15% to 1.5 billion.

Ikea’s sales in Europe, which accounts for almost 70% of Group turnover, improved a little during the 2014 financial year after a long period of lacklustre performance. Ikea’s sales held up well in North America and expanded in China and Russia during the 2014 financial year. Ikea’s largest markets in terms of sales in the 2014 financial year were Germany, the US, France, Russia and the UK.

The Ikea Group is targeting 50 billion euros in sales by 2020 as it adds outlets, expands its online offering and introduces collections more frequently. €200 million has also been set aside for “Tack!”, a new loyalty programme.

Sustainability is another part of the Group’s business development strategy. Within its own operations, the Ikea Group produced renewable energy equivalent to 42% of the total energy consumed, and aims by the end of 2015 to have invested and committed to invest €1.5 billion in renewable energy projects – chiefly offsite wind farms and photovoltaic (PV) panels.

During the 2014 financial year, the Ikea Group recorded a 58% increase in the sales value of “products that enable people to live a more sustainable life at home”.

AHEC highlight continuing focus on oak and walnut in European furniture

A recent report from the American Hardwood Export Council (AHEC) reviews hardwood furniture trends based on a visit to the annual IMM furniture show in the German city of Cologne in January. AHEC interviews at the show suggest that after more than five years of poor sales and falling consumption, the market for high-end furniture in Europe is improving. Many exhibitors of hardwood furniture anticipated a better show for sales than the previous year.

As in previous years, oak and walnut dominated the look. Nearly all walnut was from the United States, while most oak was European. AHEC suggest this is primarily due to the easy access to European oak by Central European manufacturers. These manufacturers are also now able to utilise relatively low grades and short specifications which can be sourced very competitively. Increasing use of these grades has gone hand-in-hand with deliberate marketing of the “rustic” look in oak furniture. AHEC also suggest that solid wood is in vogue and there appears to be less veneer used than in the past.

AHEC note that the only tropical wood on display was in the international section and mainly in the Indonesian pavilion. Temperate species other than oak and walnut were also not much in evidence. There was some beech, mostly for chairs and table legs but not for large visual surfaces of table tops and cabinet doors. There was also a bit of ash (mostly European). However, the smoother, cleaner grain and texture of maple and cherry is currently less favoured. Maple was mostly being used in small quantities in white finishes as a contrast to the dark walnut and rustic oak.

AHEC observed that there was lack of strong environmental messages and branding at the show, surprising given that IMM Cologne is the main shop window for high end commercial furniture sold in Europe. Most furniture manufacturers apparently have yet to embrace LCA or EPDs for active market development – although some companies are now considering this as a way to differentiate product in a highly competitive market.

PDF of this article:

Copyright ITTO 2020 – All rights reserved