The International Hardwood Conference (IHC) held in Copenhagen from 16-18 September identified access to raw materials, changes in global trade flow patterns and growing purchasing competition with buyers from other parts of the world as well as innovation in non-wood materials as key challenges currently facing the European hardwood industry.

At the same time, however, the conference also highlighted European countries’ common goals and interests in their commitment to the sustainable use of hardwoods and the promotion of an increased use of wood in society in general. The benefits of wood as an environmentally friendly, sustainable building material were emphasised as a major advantage in this context, as was Europe’s advanced educational system in the fields of architecture and wood engineering.

Innovation, creativity, new, high-end applications for hardwood as well as tapping into new markets were considered key to success.

Presentations held in the morning of the conference primarily focused on trade flow trends in the global and European markets as well as on the situation in major hardwood exporting and importing markets in Europe, the USA, Asia and Africa. In the afternoon, the focus shifted to the sustainable and creative use of wood in architecture, and furniture production as well as on new market opportunities for hardwoods.

China and Asia rule the timber world

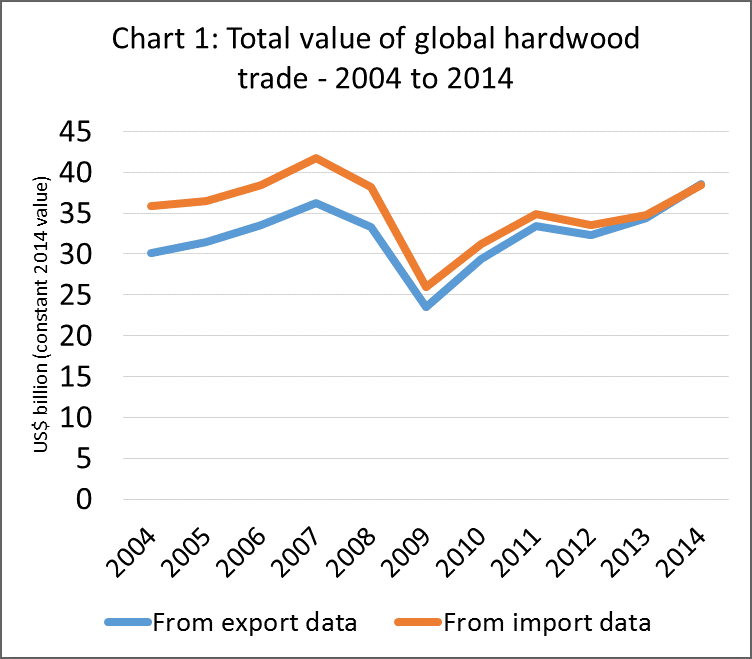

Rupert Oliver, speaking on behalf of the EU-funded and ITTO-hosted FLEGT Independent Market Monitoring (IMM) project, opened the Conference with an overview of global hardwood markets. He showed that the global value of hardwood trade, adjusted for inflation, had rebounded close to pre-crisis levels in 2014. The total value of global trade in hardwood products (including logs, sawn, mouldings/decking, veneer, and plywood) was around US$38.5 billion in 2014, an increase of 10% on the previous year (Chart 1).

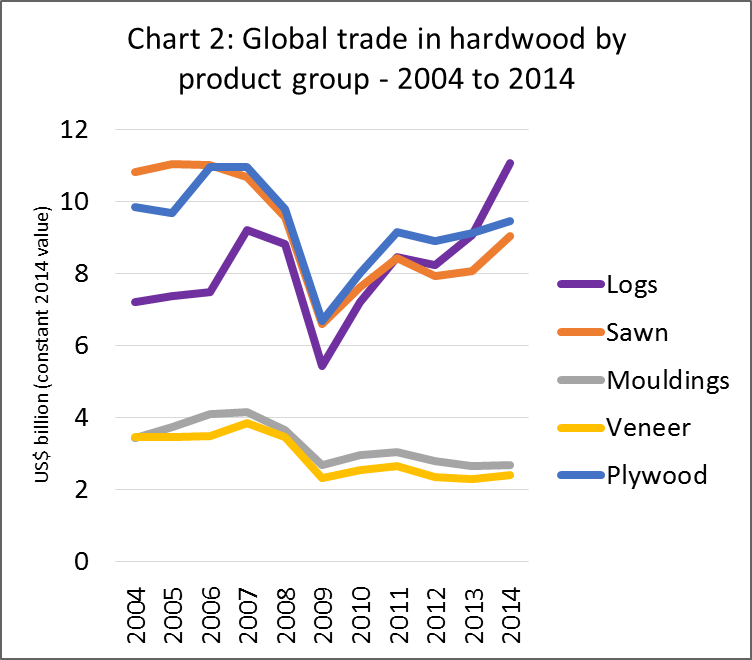

Analysis of the various product groups reveals that the upward trend was heavily dependent on a sharp increase in the global hardwood log trade. In fact, the total value of global trade in hardwood logs, at around US$11.1 billion in 2014, was significantly higher than the previous peak in 2007 (when global hardwood log trade was US$9.2 billion). The value of global trade in all other hardwood materials – sawn wood, mouldings, veneer and plywood – still falls short of the peak just prior to the financial crises that hit western industrialised nations in 2008 (Chart 2).

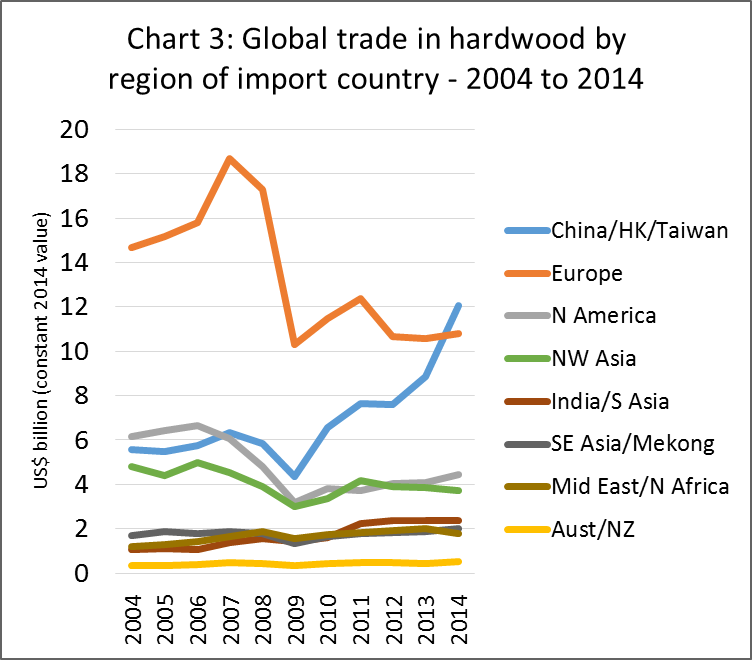

These trends are largely explained by the regional shift in global hardwood trade since the financial crisis (Chart 3). The value of China’s hardwood imports doubled between 2009 and 2014, to more than US$12bn. Although China’s imports of sawn hardwood have been rising, growth is still heavily concentrated in logs. The value of China’s log imports increased from just over US$2 billion in 2009 to close to US$7 billion in 2014.

Meanwhile the influence of Europe – traditionally a large buyer of further processed products like sawn wood, veneers or mouldings – has declined in global hardwood trade flows. The total value of hardwood imports by European countries (including intra-EU trade), fell from more than US$18bn in 2007 to just over US$10bn in 2009. The total value of hardwood imports by European countries has remained broadly flat since then.

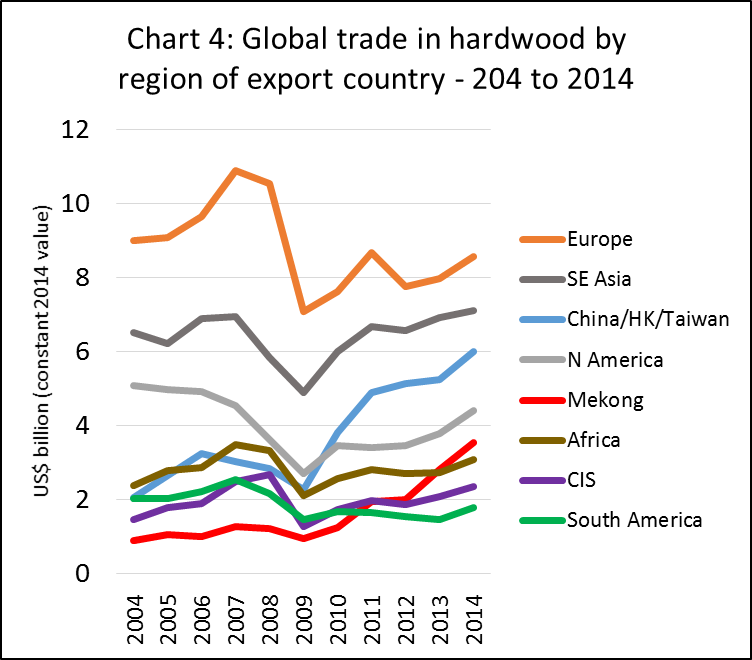

In terms of hardwood export value, the large volume of intra-regional trade means that, in total, European countries remain the largest source of internationally traded hardwoods (Chart 4). In 2014, European countries exported hardwoods with a total value of US$10.8 billion, 2% more than the previous year but well below the peak level of US$18.7 billion recorded in 2007. The increase in European country exports last year was driven partly by improved consumption in the UK and Spain and partly by rising sales of hardwood logs and sawnwood to countries outside Europe, notably China and Egypt.

However the value of hardwood exports by countries in other parts of the world have been rising more rapidly. There’s been a particularly rapid rise in the value of exports by China (dominated by plywood) and by countries in the Mekong delta region (including both rubber wood and hongmu species, both destined primarily for China). The value of exports by the USA has also been rising with a significantly higher proportion now destined for China and South East Asia and a lower proportion destined for Canada, Mexico and Europe.

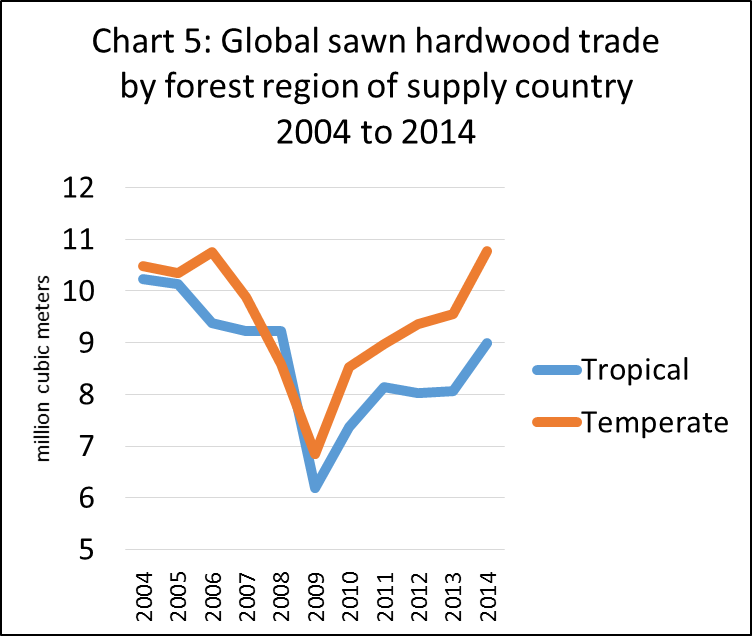

Considering just sawn wood, Mr Oliver showed that global trade in temperate hardwoods recovered much faster than tropical wood following the financial crisis (Chart 5). In fact global trade in sawn temperate hardwood reached 10.77 million m3 in 2014, 13% higher than the previous year and just exceeding the previous peak in global trade of 10.75 million m3 in 2006. Global trade in sawn tropical hardwood also increased sharply in 2014, rising 12% to reach 8.99 million m3. However, this level is still 12% down on peak levels in excess of 10 million m3 prior to the crises.

As major “barriers” to expansion of hardwood markets in Europe, Mr Oliver identified the difficulties arising from the global financial crisis, product innovations in non-wood materials, the shift in global economic activity and hardwood supply to emerging markets, freight and transport issues, EU production of wood-based panels and surfacing technologies and exchange rate movements, among other things.

On the other hand, new opportunities for hardwood are being created in Europe from increased use of wood in green building, interest in hardwood in higher-value structural applications, innovations such as thermal modification which extend applications for less durable species, rising awareness of carbon credentials as well as certification and legality verification, as well as architects’ and structural engineers’ increased knowledge of timber.

European hardwood production stable at 6 million m3

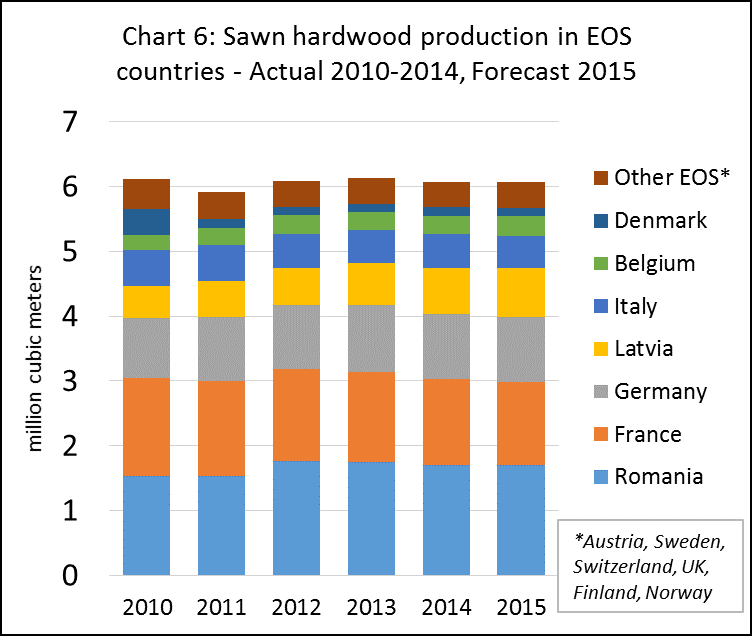

Jean-Francois Guilbert of French Timber assessed the European market from the perspective of the European hardwood sawmillers. Sawn hardwood production in member countries of European Sawmillers Organisation (EOS) was flat at around 6 million cubic meters per year between 2010 and 2014. Production is expected to remain at the same level in 2015 (Chart 6).

There have been minor shifts in European sawn hardwood production in recent years. Production in Romania, the largest supplier (mainly of beech) was rising between 2010 and 2013, but declined 3% to 1.70 million in 2014. Production in France, which has been declining slowly since 2010, fell a further 4% to 1.33 million m3 in 2014. Production in Germany fell 3% to 1.0 million m3 in 2014. However production in Latvia has been rising over the last 5 years and increased a further 9% to 717,000 m3 in 2014.

Mr Guilbert noted that exports to non-European countries, particularly China, were an increasingly important driver of production trends in the European sawn hardwood sector. Large quantities of European oak and beech logs are now destined for China which is making roundwood sourcing increasingly difficult for European sawmills.

However China is also an important market for European sawn wood, particularly oak. Sales of European sawn oak have remained relatively strong in China this year despite the recent economic slowdown. This was partly attributed to the weakness in the euro, which has given European timber a competitive advantage over hardwood traded in US dollars. The weak euro has also helped sales in Egypt, Mexico and the USA. Within Europe, Mr Guilbert identified the UK as a key market for sawn oak. For beech, Spain and Poland are important markets within Europe while Egypt is recovering strongly outside Europe.

Mr Guilbert noted that, such is the strength of international demand, European sawmills could sell considerably more but production is now constrained by limited log availability. While this is partly due to high log exports to China, other factors include increased fragmentation of private forest estates and reduced focus on commercial timber exploitation, the long-term lack of incentives for plantation establishment throughout much of Europe, and fierce competition for hardwood logs from the wine industry (mainly oak) and energy sector.

No real recovery in key hardwood consuming sectors

ETTF President Andreas von Möller spoke about recent trends in the European sawn hardwood market from the perspective of importers. He noted that at a European level, key hardwood-consuming industries in Europe – including construction, furniture, wood flooring and windows – had shown little or no recovery since the financial crises. He also stressed that developments differed greatly from one European country to the next. The furniture industry, for example, which EU-wide was still below pre-crisis levels in 2014, was growing strongly in Poland. Construction is good in Germany and the UK and recovering in Spain and the Netherlands, while France and Italy are still experiencing a downward trend.

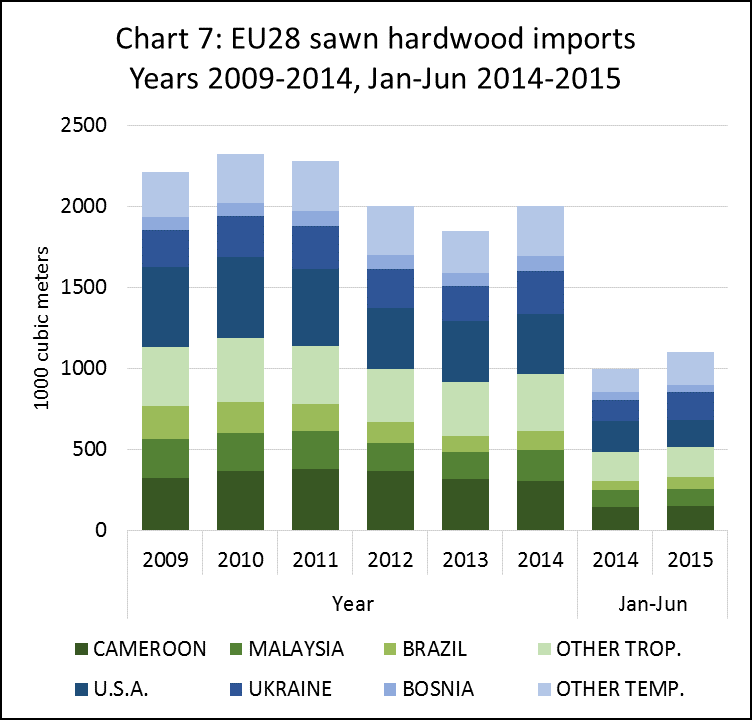

More positively, Mr von Möller noted that total imports of sawn hardwood into the EU28 were 1.97 million m3 in 2014, a rise of 9% compared to 2013. Imports have also continued to rise in 2015, reaching 1.1 million m3 in the first five months of the year, up 11% compared to the same period in 2014. However Mr von Möller echoed Mr Oliver’s assessment that temperate hardwoods have generally performed better than tropical hardwoods in the EU market in recent years. EU imports of temperate sawn hardwood were 1.10 million m3 in 2014, 12% up on the previous year and 41% down compared to before the financial crisis. This compares to tropical sawn hardwood of which 960,000 m3 were imported in 2014, 5% up on the previous year but still 63% down compared to before the financial crisis. Much of the gain in EU imports of sawn hardwood in 2015 is due to rising trade with Ukraine, Belarus and Russia (Chart 7).

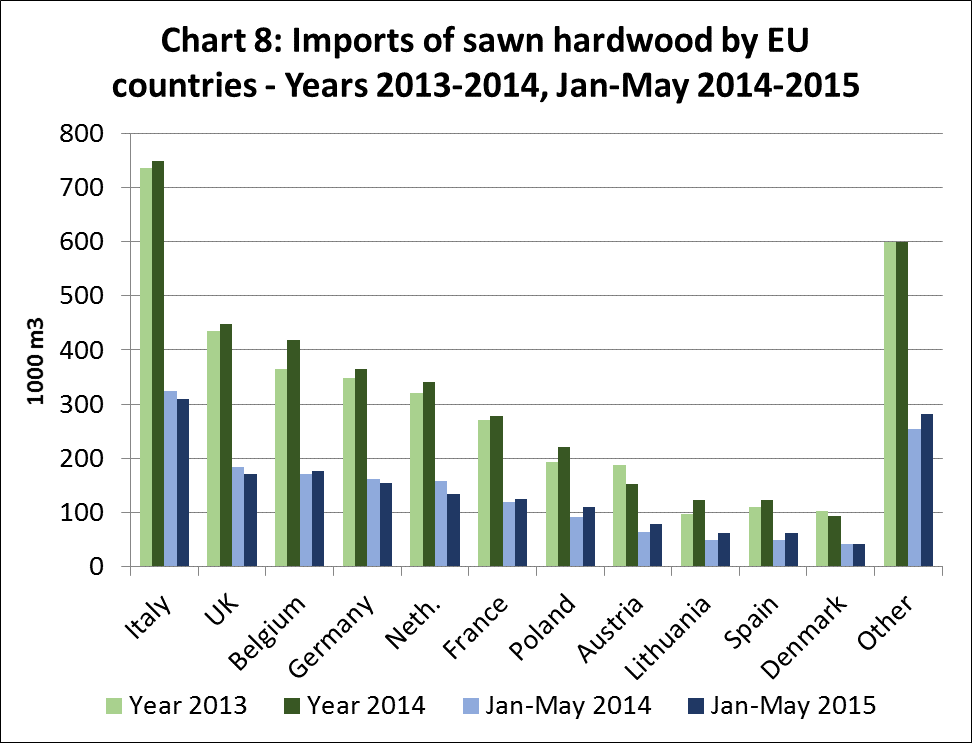

Mr von Möller also reported that the latest sawn hardwood import data indicates widely varying market conditions between EU member states this year. Imports declined in several large EU markets in the first five months of 2015, including the UK, Germany, Italy and the Netherlands. In fact amongst the five largest markets, only Belgium has increased imports this year. However imports into several smaller EU markets have registered double-digit percentage growth this year including Poland, Austria, Lithuania, Spain, Estonia, Slovenia, Hungary, Romania, Ireland and Croatia (Chart 8).

Mr von Möller went on to identify a number of key trends in the European sawn hardwood sector. Darker woods are currently favoured compared to light/reddish coloured timbers. In flooring, there continues to be a fashion for wider planks, particularly with “rustic” character. Narrow planks with “plastic” appearance lacking character and natural features are less favoured. He noted that there is regular on-going substitution – driven by price fluctuations and exchange rates – between American tulipwood and beech on the one hand, and a range of tropical species on the other, including wawa/ayous/obeche and limba.

Distribution networks for sawn hardwood in Europe have also undergone profound change since the financial crises. Generally there is now a strong preference for sourcing internally from elsewhere in Europe rather than importing from overseas. There’s much less willingness on the part of many European manufacturers and distributors to hold stock and a strong preference for buying from other European operators as and when products are needed. European operators are now much more inclined than in the past to spend time searching around a wide range of suppliers for the lowest price rather than to depend on a few regular suppliers. There’s also a much greater tendency to buy mixed container loads with smaller volumes of product in each specification than to buy full container loads of a single specification.

Timber-sector players worldwide are interdependent

Presenting to IHC on the Asian hardwood market situation, Ms Sheam Satkuru-Granzella, Director of the Malaysian Timber Council’s European office, highlighted the importance of global interlinkage and interdependence in the timber trade. She underlined the importance of China and India as wood consuming and remanufacturing countries and observed that current weakness in the Chinese market would significantly impact developing countries, particularly in Africa and Papua New Guinea.

Ms Satkuru-Granzella noted the growing importance of the Chinese domestic market as opposed to the re-export business. She also observed that while there has been recent strong growth in China’s imports of red “hongmu” timbers, China’s market for more modern furniture and finishing in lighter shades is also growing rapidly.

In Europe, Ms Satkuru-Granzella identified on-going economic consolidation as well as weakness in the European construction sector, with no major changes expected in the short-term, as major challenges facing the Asian hardwood business in Europe. She emphasised that Asian hardwood producers are focusing elsewhere due to subdued European demand. She also mentioned implementation of the EUTR as another challenge, noting problems associated with inconsistent application of the regulation across the EU.

Structural changes in US hardwood production and sales

Mike Snow, Executive Director of the American Hardwood Export Council, spoke about structural changes in the US hardwood industry that increased the sector’s emphasis on exports in recent years. Total US hardwood production peaked as long ago as 1999 and, after sliding for a few years, fell sharply by 49.3% between 2005 and 2009. US hardwood production started to recover from 2009 but is still way below peak levels. It’s also well below potential: as harvest has remained well below growth the volume of hardwood standing in US forests has more than doubled to over 11 billion cubic meters in the last 50 years.

Mr Snow noted that while demand for hardwood in some industrial sectors in the US has been rising, there has been a long term decline in US domestic consumption of graded lumber in the furniture and construction sectors. US lumber production has shifted from around 60% grade and 40% industrial lumber to 40% grade and 60% industrial. The vast majority of the graded lumber produced in the US is now exported.

In terms of US hardwood lumber exports, China and other Asian markets like Vietnam and Thailand have significantly gained in importance over the last ten years, whereas volumes to Europe have declined. China, in particular, saw disproportionate growth: between 1999 and 2006 US exports to China increased by 759.5% and between 2009 and 2015 by another 269.9%.

Mr Snow also confirmed the increasing importance of the Chinese domestic market as a wood consumer. He said that whereas a decade ago, around 80% of the American hardwood imported by China was further processed and re-exported, the proportions have now reversed with only around 20% re-exported and up to 80% destined for the domestic market.

Purchasing competition for African timber

Mr Ad Wesselink, Managing Director of Netherlands-based Wijma, identified purchasing competition from Chinese companies – which do not have to verify the legality of their purchases – and Chinese investments in Africa as key challenges for European companies active in African timber trade and manufacturing. Furthermore, African timber still struggles with image issues and certification is proceeding much too slowly. Added to this are serious logistical and transport issues. And of course the European market for tropical timber remains subdued.

Mr Wesselink noted that EU imports of African sawn wood decreased from 1.12 million m3 in 2004 to just 530,000m3 in 2014. The sharpest falls were registered between 2005 and 2009; since then imports have stabilised with slight fluctuations. African logs have fared even worse in the EU market, declining around 80% in the last ten years, to just 102,000m3 in 2014. Europe’s share in African tropical timber exports has therefore fallen from 78% in 2004 to 52% in 2014.

To turn the situation around, Mr Wesselink said the tropical timber sector must do more to raise awareness of progress in forest management. Around 5.5 million ha of forest in the Congo, Gabon and Cameroon is now FSC certified and large areas are legally verified, for example. These facts need to be communicated.

Due Diligence: costly and time-consuming

Armand Stockmans of Somex underlined the commitment of the EU trade to meeting the legality requirements of the EU Timber Regulation (EUTR) – even though Due Diligence remained complex and costly in many instances: Operators have to deal with different documents from each country and to adapt their due diligence accordingly.

Information on suppliers has to be collected for each company separately and through a variety of sources, including own visits and experience, the Internet and NGOs.

According to Mr Stockmans, European companies have to be prepared to end commercial relations with suppliers or to stop purchasing from certain regions in case of doubt, something that his company has done in South America, Africa and Asia.

Green building is a key new market opportunity

The afternoon session of the IHC focussed more on new market opportunities and the potential for increased use of hardwood as a construction material. Matti Kuittinen from Aalto University School of Arts, Design and Architecture reported a recent revival in wood construction. Besides single-family homes, several tall wooden buildings are under construction all over the world.

As a main reason for the increased use of wood – besides aesthetics – he noted the growing awareness of climate change and other environmental issues, for example reflected in Green Building initiatives at national level in a several EU countries and the EU Directive for energy performance of buildings that requires new buildings to be nearly zero energy after 2020. .

Zero energy buildings can be made from different materials, according to Mr Kuittinen, but wooden buildings always seem to have lower carbon footprint than others. He concluded that “wood construction has been and will always be a vital part of our bioeconomy”.

This view was shared by Peter Wilson, Director of the Institute for Sustainable Construction at Napier University in Edinburgh, UK. He emphasised the number and importance of European architects as potential clients for the wood industry and stated that the timber industry still fails to reach out to enough architects. Architects are of special importance to the hardwood industry since they are often the key decision makers in high-value building projects.

Mr Wilson felt there is particular value in working with European universities – which train some of the world’s leading architects – to increase coverage of timber in the architectural syllabus. He also stressed that the development of engineered wood products has changed the perception of timber among designers and architects. China, in particular, should be encouraged to build its fast growing cities in wood rather than concrete or steel.

AHEC’s European Director David Venables echoed this call. He named architects, designers and specifiers as potential clients and key to future growth in the hardwood market.

In addition to more promotion and more education, he emphasised the need to develop innovative tools to deliver credible technical and performance data on hardwood materials. It is necessary to scientifically prove the advantageous performance of hardwoods compared with other building materials. Moreover, wood promotion should support the use of wood through simple and understandable messages. AHEC is showing how it’s possible to influence fashion trends to favour of a wider range of hardwood timbers by working with high-profile architects and designers.

Besides structural applications and a focus on environmental advantages, Mr Venables identified exterior applications and a wider use of species and grades as new opportunities for the hardwood sector. As an example, he presented AHEC’s “Endless Stair” project, made from cross-laminated Tulipwood produced from No 2 Common grade material.

Eyes opened for new market opportunities

Both organisers and participants seemed broadly satisfied with this year’s IHC, which for the first time was jointly organised by the European Timber Trade Federation (ETTF) and the European Organisation of the Sawmill Industry (EOS), with the Danish Sawmill Association and Timber Trade Federation as national co-hosts. Martin Nyrop-Larsen from the Danish Sawmill Association said that both traders and sawmillers benefitted from “useful information about markets and the future”. He noted that “eyes were opened for new market opportunities, for example in India”. The conference attracted around 100 delegates from 19 countries.

PDF of this article:

Copyright ITTO 2020 – All rights reserved