Like the Domotex show held in Hanover earlier in the month, the IMM Furniture Fair in Cologne between 16 and 22 January highlighted the challenges facing tropical suppliers looking to increase their share of the European market, as pressure continues to mount from domestic manufacturers and non-wood materials. Demand for wooden exterior furniture, traditionally an important niche market for tropical wood products, is coming under pressure from other modern weather-resistant materials.

However, the Fair also emphasised that wood, alongside other natural materials and organic finishes, is very fashionable for interior furniture, that there is strong interest in furniture with a strong back story, and that small, well-designed products have an important role in the European furniture sector. All these trends offer new avenues to market for suppliers of tropical wooden furniture.

As if to emphasise these opportunities, the headline of the leading article on the IMM show by Decoist, a leading on-line magazine focused on architecture and modern design was “Wood is beyond good – it’s sensational!”. Decoist observes that “one of the big furniture design trends of 2017 is undoubtedly the way in which top manufacturers and designers have so whole heartedly embraced wood. In a world where organic finishes and natural materials are making a rapid comeback, wood is definitely the absolute king of 2017 and this trend is likely to continue to last beyond the year as well!”

Decoist’s comment that “Indonesia made a big impact at this year’s show with their unique creations” is particularly encouraging for the tropical wood sector and an early sign of the potential of Indonesia’s market development strategy in Europe. Indonesia had a significant presence at the show having booked just under 600 square metres for a national pavilion displaying products from a wide range of Indonesian companies, a timely investment in marketing for a national furniture industry that is the first, and only capable of delivering 100% FLEGT-licensed product.

Indonesia did well to target IMM Cologne which is now one of world’s leading furniture shows following a marketing drive to internationalise the event. The show achieved a record number of visitors this year, exceeding 150,000 for the first time. Of the 104,000 trade visitors, around 56,000 came from Germany and 48,000 from abroad (an increase of 4%). There were particularly large increases in visitor numbers from Spain, Russia, Italy, the UK, Netherlands, Poland, China, South Korea, India and the United Arab Emirates.

The show boasted around 1,200 exhibitors from 50 countries displaying more than 100,000 pieces of furniture and furnishing items, a third of which were shown to the international market for the first time in Cologne.

Non-wood materials taking greater share in exteriors market

While wood is in the ascendance in the interiors sector, the IMM show highlighted that alternative materials are making more ground in the exteriors sector. Exterior furniture continues to become more and more flexible and decorative and adapts to growing demand for pieces that can be used both inside and outside. This demand is driven both by new materials and lifestyle changes in which more people spend time on balconies, decks, patios and similar spaces which combine features of gardens and rooms.

Solid tropical wood garden furniture is increasingly substituted by outdoor sofas and chairs comprising modern, weather-resistant materials, with water resistant cushions and frames created using steel or plastics woven using traditional wicker techniques. Teak is still popular, but mainly to accent and soften furniture made primarily in other materials.

A star attraction of the show was the Caribe collection of outdoor furniture designed for Ames by Sebastian Herkner, a leading designer who was Guest of Honour at the IMM Cologne show in 2016, in collaboration with Colombian craftsmen. The pieces were made of woven plastic string and steel using the “Momposino” weave which is taught in school as a craft in the Santa Marta region of Colombia.

While not made of wood, the message conveyed about the Caribe collection in the IMM show publicity is relevant and should give encouragement to manufacturers of tropical wood furniture.

The IMM organisers observe that “the Caribe series stands for a trend in the interiors industry which is exemplary of the growing need for meaningfulness among manufacturers and consumers. And contrary to some expectations, this trend is evidently being carried by the market. It is not always the case that one succeeds in combining sustainable production with an aesthetic concept in a pilot project while at the same time also accommodating the increasing interest of people for authentic products. However the number of products that tell their own special story is constantly growing.”

Another trend at the IMM show that could be exploited by the tropical timber sector is to extend the use of solid wood into the climatically difficult environment of the bathroom. Together with the bathroom furniture manufacturer, Keuco, the company Team 7 from Austria was displaying the Lignatur edition at IMM Cologne which utilises natural wood to provide a high quality and unique finish to bathrooms. Again, the material used in this instance was not tropical timber, the traditional European favourites of walnut and oak being preferred. However, use of tropical wood would offer manufacturers both technical and aesthetic advantages in high-end bathroom furniture.

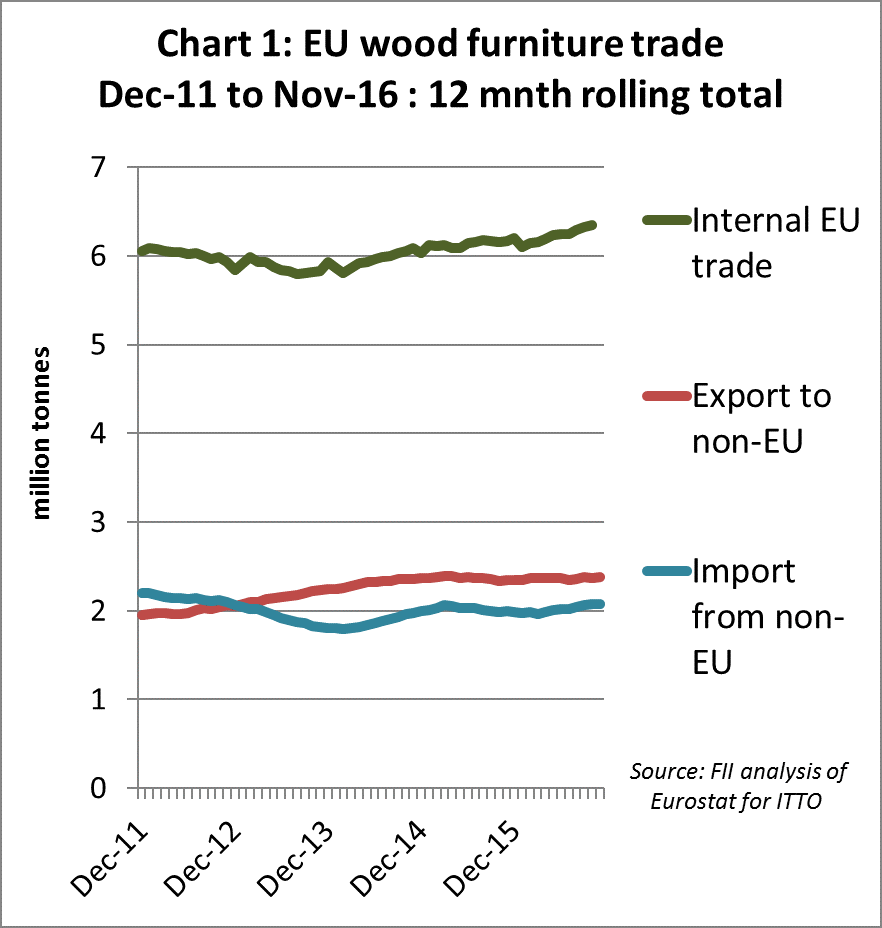

Furniture trade in Europe growing slowly

The trade background to the IMM fair is shown in Chart 1 which indicates that internal EU trade in wood furniture has been rising slowly since December 2013. This is due partly to improving consumption of wood furniture products manufactured in the EU, and to the increasing role of manufacturing facilities in lower cost Eastern European countries such as Poland and Lithuania to supply wood furniture to other parts of the EU.

The EU continues to maintain a small trade deficit in wood furniture with the rest of the world. Total EU exports to non-EU countries remained level at around 2.4 million tonnes in both 2015 and 2016, while imports were also stable at around 2 million tonnes. EU imports of wood furniture from China, which is by far the largest external supplier accounting for 50% to 55% of the total, were sliding in 2015 and the first half of 2016, but recovered slightly towards the end of last year.

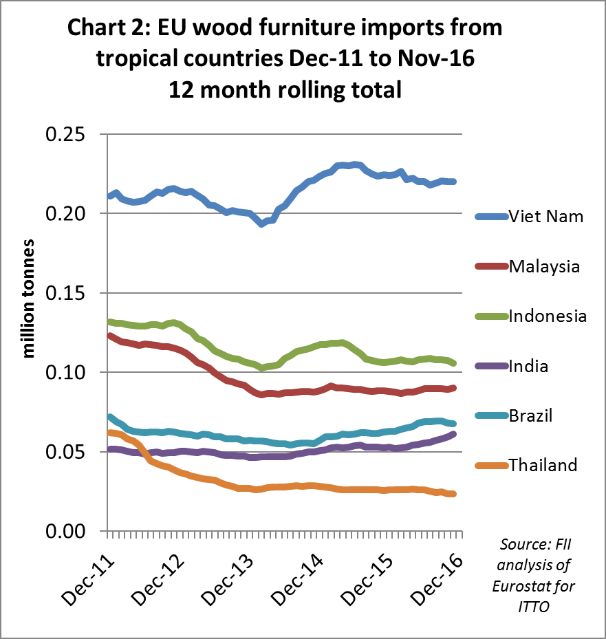

The performance of tropical countries in supply of wood furniture to European markets has been mixed in recent years (Chart 2). EU imports from Vietnam increased sharply between April 2014 and April 2015, taking share from China at that time. However, EU imports from Vietnam were sliding slowly between mid-2015 and the end of 2016.

EU imports of wood furniture from Indonesia surged briefly and temporarily in 2015, but fell back again in 2016. It will be interesting to see whether Indonesia’s delivery of FLEGT licensed furniture and support for marketing in Europe will now be translated into an increase in sales.

Meanwhile EU imports of wood furniture from Malaysia and Thailand have been broadly flat over the last 3 years after losing ground in 2011 and 2012. In contrast EU imports from Brazil and India have been making ground in the last two years, although both are still relatively minor suppliers of wood furniture to the EU.

EU importers stock up on FLEGT licensed Indonesian plywood

The Global Timber Forum has published an interview with the CEOs of two European importing companies, Alexander de Groot of Fepco and Koen de Witte of Altripan, that were among the first to receive FLEGT licensed wood from Indonesia. The interview highlights both the market opportunities and remaining challenges of FLEGT licensing from the perspective of two of Europe’s largest plywood importing companies.

According to Alexander de Groot, FLEGT licensing offers a significant market opportunity for Indonesian plywood in Europe as due diligence is no longer required and buyers can be absolutely certain that all Indonesian wood comes from legal sources. Koen de Witte said that a large group of customers in Europe have been afraid of buying tropical wood because of possible EUTR problems and related negative publicity but that FLEGT licensing means importers can now start promoting tropical wood to these companies again.

Koen de Witte noted that products from Indonesia are rather expensive compared to competing materials from China or Malaysia and that logistics can be a challenge, however FLEGT licensing offers an opportunity to promote Indonesian plywood as a legal and high quality, sustainable product. He said that Indonesia will also have an increasing advantage over time as EU Competent Authorities are getting stricter and there are more checks on operators.

Koen de Witte said that there has yet to be any perceptible increase in demand from their own customers for FLEGT licensed timber, but “arrivals of wood from Indonesia have increased over the last few weeks as importers and traders are stocking up on FLEGT licensed material”. He also emphasised that it is early days and companies like Fepco and Altripan will now push to increase sales with active promotion and by making the more product available in the market.

Koen de Witte reckoned that Indonesian wood products are competitive in Europe and their market share will increase – although this will be partly dependent on developments in competing products which, for Indonesian plywood, are mainly from Russia and China. He suggested that “the great variety of products from China – in very different qualities and not always correctly declared – is making life difficult. But there are initiatives now to increase transparency and show customers how the plywood is made and what the differences are. This will improve Indonesia’s position”.

Alexander de Groot emphasized that European governments also have a responsibility now to help promote FLEGT licensed wood. He suggested that FLEGT should, for example, immediately be incorporated in public procurement rules and given the same status as FSC or PEFC. He noted that “one of our customers just had a case in Luxembourg, where authorities would not accept FLEGT licensed wood on a bid for a public building project – they only wanted FSC. This situation cannot continue. If European governments are not behind FLEGT this will sabotage the process”.

Both CEOs confirmed that of their own customers, the larger distribution groups and merchants in Europe are already familiar with the FLEGT process, but as large corporations their decision-making processes are fairly slow so it might take some time before they start purchasing more FLEGT licensed wood. Smaller merchants are generally less aware of FLEGT. At present importers are still more inclined to prefer FSC and PEFC, particularly in the UK and the Netherlands, but here merchants are quickly becoming aware of the importance of FLEGT licenses. France, Belgium and Germany are more difficult as companies there use less certified wood in general and interest in FLEGT is perceptibly lower.

While recognizing that their Indonesian suppliers had to work extremely hard to achieve FLEGT licensing, both CEOs said that from the perspective of European importers the process has been very simple. The importers only had to register to obtain a FLEGT license number and the rest was pretty much what they always had to do when importing wood. For them it basically comes down to uploading some information on a website and is much simpler than having to conform to EUTR due diligence requirements.

PDF of this article:

Copyright ITTO 2020 – All rights reserved