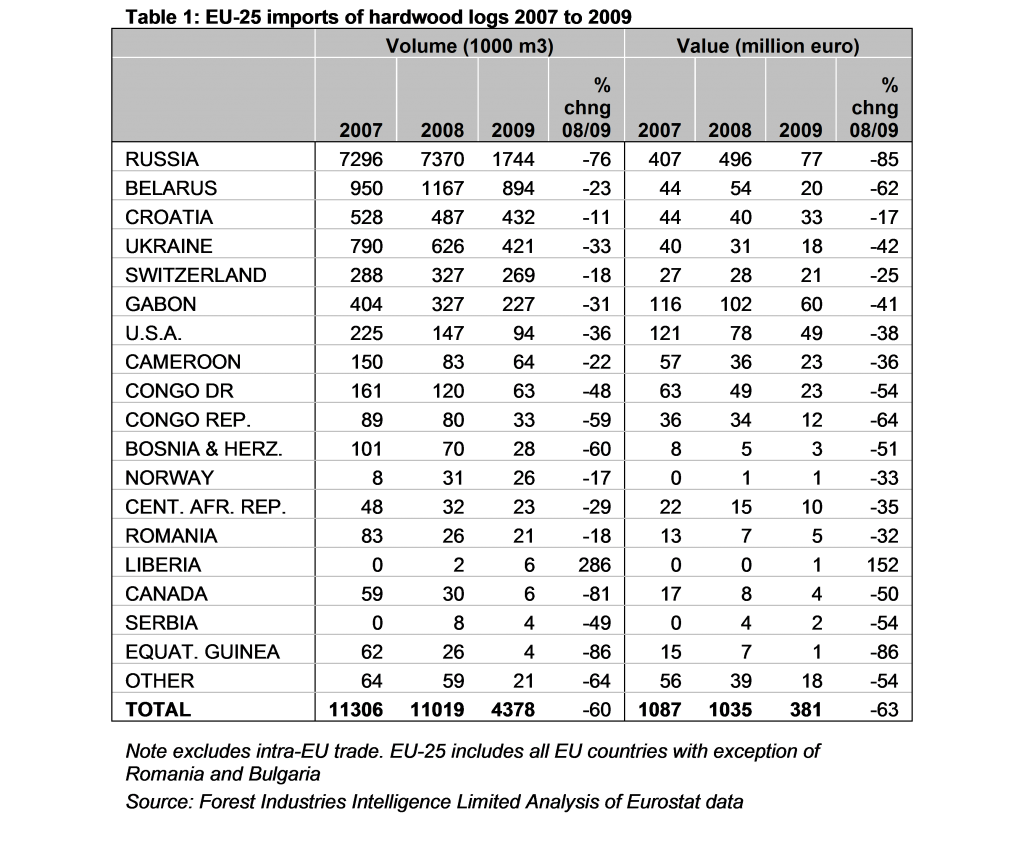

During 2009 EU imports of hardwood logs reached only 4.38 million m3, down a massive 60% on the previous year (Table 1). In addition to recessionary pressures and a lengthy period of destocking by European importers, the figures are strongly influenced by Russia’s phased introduction of log export taxes. This contributed to a 76% fall in the volume of EU imports from Russia during the year. However log imports were also well down from key tropical hardwood supplying countries including Gabon (-31%), Cameroon (-22%), the Congo Democratic Republic (-48%), and the Congo Republic (-59%).

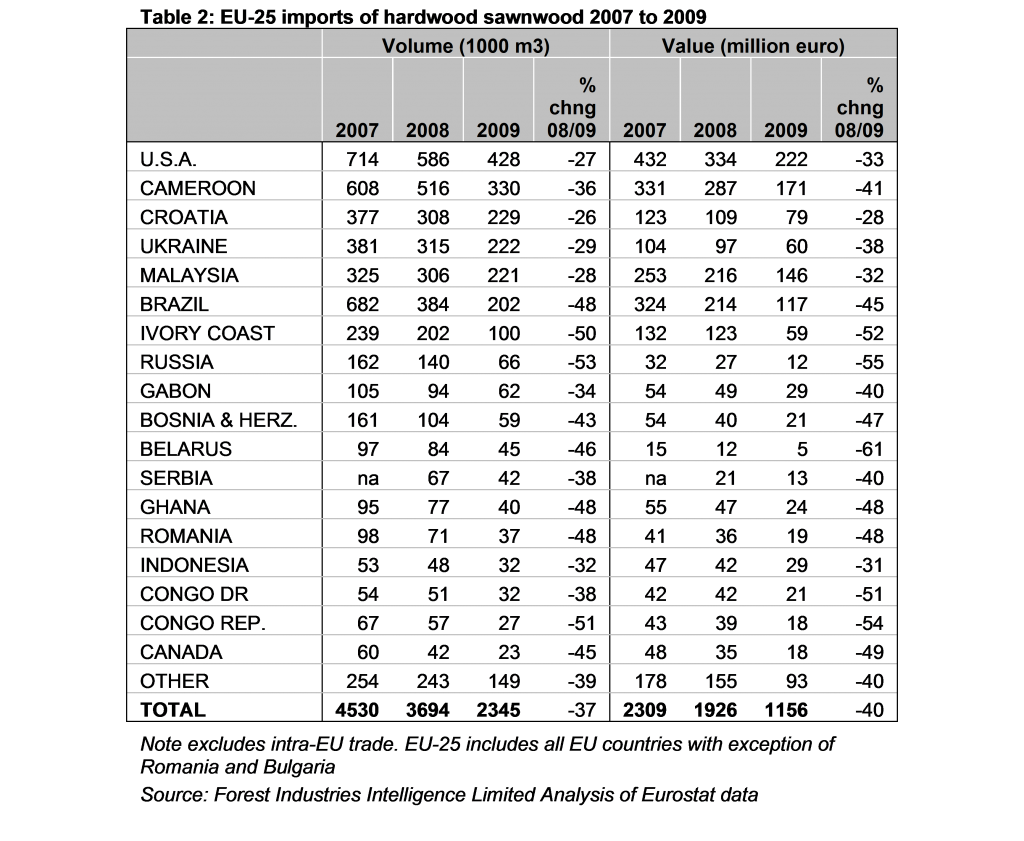

EU hardwood sawn imports down across the board in 2009

The decline in EU imports of hardwood sawn lumber, at around 37% in volume terms, was only slightly less dramatic than that experienced in the log sector (Table 2). All supply countries fared badly in the European market last year. The USA, the leading supplier, did better than most – the 27% decline in EU imports from the USA was relatively modest compared to the downturn in imports from other countries. The relative weakness of the dollar against the euro was one factor boosting U.S. hardwood competitiveness in Europe during 2009.

During 2009, Cameroon retained its position as the leading supplier of tropical hardwood sawnwood to the EU despite a 36% decline in shipments compared to the previous year. A number of factors contributed to this decline including: very slow European consumption of the leading Cameroon redwood species sapele and sipo; continuing efforts by European importers to destock during the first half of 2009; and mounting supply problems in the second half of the year.

EU imports of sawnwood from Malaysia held up marginally better than those from Cameroon, benefiting partly from the weaker dollar (Malaysian hardwoods unlike African hardwoods tend to be invoiced in dollars) and also from better availability and faster turnaround times. This latter factor has become particularly important in the recession as distributors throughout the European supply chain have been much less reluctant to carry stock.

Continuing supply problems and better market prospects at home contributed to a dramatic 48% fall in EU imports of hardwood sawn lumber from Brazil.

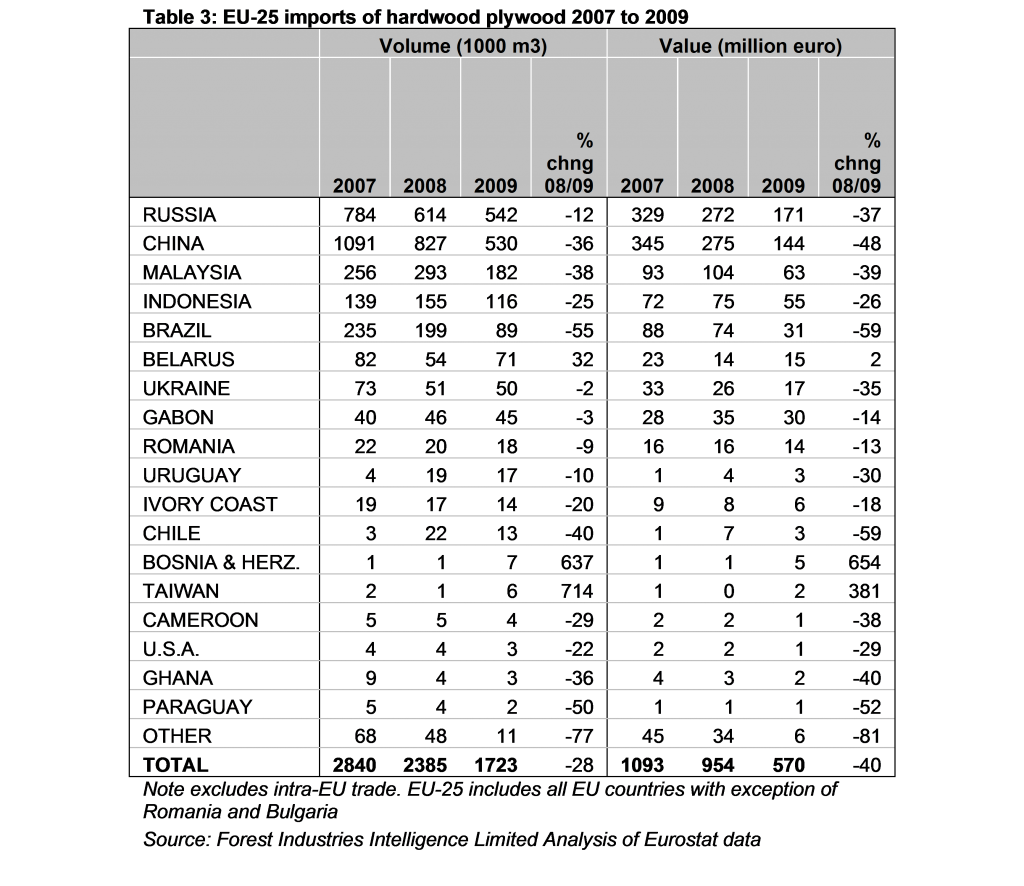

EU hardwood plywood imports down 28% in 2009

EU imports of hardwood plywood were down 28% in volume terms during 2009 (Table 3). Imports from Russia, the leading supplier of hardwood (mainly birch) plywood to the EU, experienced only a relatively modest decline of 12%. Russian plywood producers stepped in to fill some of the gap in Finnish supply with the phased introduction of Russia’s log export taxes. There are also reports that more European plywood buyers are switching away from tropical hardwood in favour of Russian birch product.

During 2009, China retained its dominant position as the leading developing world supplier of hardwood plywood to the EU, although at 530,000 m3 the volume is only half of that attained in 2007.

After significantly expanding share in the European hardwood plywood market in 2008, Malaysia lost ground in 2009. Recent trade reports suggest that declining availability due to tightening log supply in Malaysia is now encouraging more European importers to look to alternatives, including Russian birch plywood, alternative panels and non-wood products.

The pace of the long-term decline in European imports of Indonesian plywood slowed in 2009. However imports of Indonesian plywood – which reached only 116,000 m3 in 2009 – are a shadow of levels of around 600,000 m3 only 7 years ago. Meanwhile the decline in European imports of Brazilian hardwood plywood steepened last year, falling 55% to only 89,000 m3.

Major structural changes underway in EU veneer sector

Europe’s hardwood veneer import figures for 2009 (Table 4) bear the imprint of differing trends affecting the rotary and sliced veneer sectors. Both sectors have been profoundly influenced by the global economic downturn.

The rotary veneer sector is being influenced both by falling European consumption of tropical hardwood plywood and by the continuing shift in tropical hardwood plywood manufacturing away from Europe (notably France). These trends are particularly apparent in the significant decline over the last two years in European veneer imports from Gabon, the leading supplier of rotary veneer (mainly okoume), to the European market.

Meanwhile, the European sliced veneer sector experienced a major crises during 2009. There was a huge fall-off in demand, particularly in the door sector in Spain which had previously been one of the largest consumers of sliced veneer in Europe. A major reduction in hardwood harvesting in all the leading supply regions greatly reduced access to veneer quality logs. Severe cash flow problems also limited the ability of veneer mills to procure those logs that were available. This all occurred at a time when competitive pressure from the laminate and non-wood surface materials sector – also suffering from excess capacity – was on the rise and as product manufacturers were looking for ways to cut costs.

As a result of these trends, all the leading suppliers of sliced veneer lost a lot of ground in the European market during 2009. The volume of European hardwood veneer imports from Ivory Coast, the U.S.A. and Cameroon was down 44%, 38% and 46% respectively. For these suppliers, some cold comfort may be found in the fact that market conditions were just as bad for European veneer manufacturers. The Germany-based trade journal EUWID reports that large European veneer mills were operating at no more than 50% to 70% of capacity throughout 2009.

Early signs of recovery in EU imports during last quarter of 2009

While the 2009 annual import data makes for very gloomy reading, closer analysis of the quarterly data provides grounds for optimism. Chart 1 indicates that EU imports of hardwood logs, sawn and veneer from developing countries all turned upwards in the last quarter of 2009. In the case of logs and sawn, this was the first upward movement in import data following seven consecutive quarters of decline. For veneers, the upturn followed on from six consecutive quarters of decline. Meanwhile, the upturn in EU imports of plywood which began in the third quarter of 2009 was maintained into the last quarter of the year.

The signs are more promising but there is still considerably uncertainty over the likely strength of recovery in European tropical wood imports during 2010. Trade reports suggest that the recent rebound in imports has less to do with any significant change in underlying consumption than in a move by importers to fill gaps in stocks which have become extremely thin on the ground after such a long period low imports.

European imports of tropical hardwood logs from Gabon also received a significant short-term boost in the final quarter of 2009 as European plywood manufacturers sought to build stocks in advance of Gabon’s log export ban scheduled to be introduced from 1 January 2010.

At the end of 2009, European importers of all hardwood products were also responding to widespread reports of tightening availability in major supply regions which was widely reflected in rising prices. Lack of availability combined with patchy consumption may well put a brake on further significant increases in European imports of tropical hardwoods during 2010.

PDF of this article:

Copyright ITTO 2020 – All rights reserved